Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

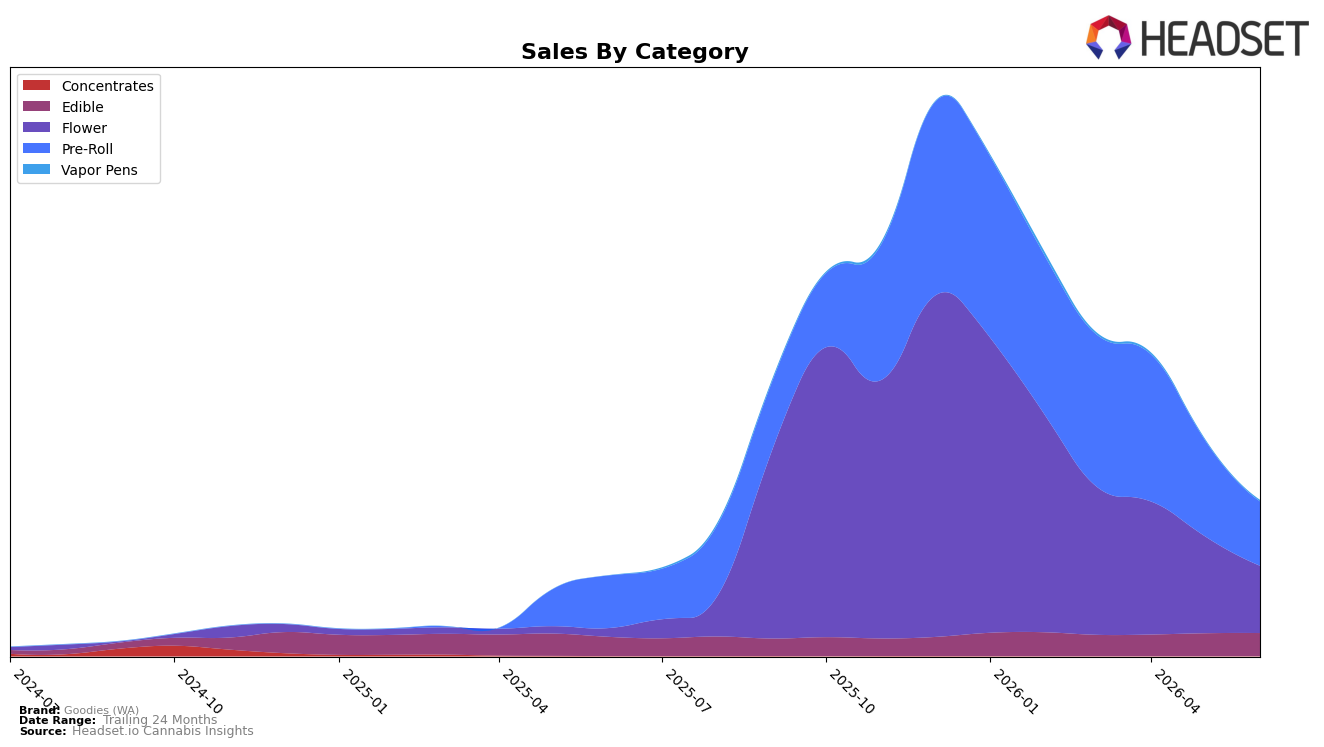

Goodies (WA) concentrated 43.18% of June 2026 sales in Flower and 41.31% in Pre-Roll, with Edible at 14.71% and Vapor Pens at 0.80%. Flower expanded year over year by 698.03% while Pre-Roll rose 22.50%, yet month over month both contracted, with Flower down 30.89% and Pre-Roll down 33.37%; Edible inched up 0.90% MoM and Vapor Pens rose 19.60% MoM. The mix shift indicates reliance on two large, simultaneously cooling inhalable segments, while smaller Edible and nascent Vapor Pens provided the only MoM stability; combined with a brand-level 94.48% YoY sales lift and a 90.21% YoY increase in average price to $17.27, the pattern implies recent price-led gains are vulnerable if June’s double-digit MoM pullbacks in core categories persist.

Within the Flower category, a rank of 63 in New Jersey despite a 698.03% YoY surge suggests scale is still limited relative to the field, and the 30.89% MoM decline signals share capture may be episodic rather than durable. With Pre-Roll also down 33.37% MoM while Edible grew 0.90% MoM and Vapor Pens climbed 19.60% MoM off a 0.80% share base, the portfolio tilts toward volatility-prone inhalables; the implication is that Goodies (WA)’s positioning would benefit from converting Edible’s steadier month-level trajectory into a larger share and using Vapor Pens’ momentum to diversify away from the twin MoM contractions in Flower and Pre-Roll.

Competitive Landscape

Goodies (WA) sits at rank #63 in June 2026, down 21 places from rank #42 in March 2026 and 34 places below its peak rank of #29 in January 2026; over the same June 2026 snapshot, Find. climbed YoY from #12 to #1 while Ozone held near the top moving from #2 YoY to #2 despite a -10.6% sales change. With competitors like Good Green advancing from #14 to #3 alongside +88.6% sales growth and Simply Herb rising from #13 to #4 with +57.9%, Goodies (WA)’s slide from #42 to #63 in the last three months implies a share reallocation toward faster-moving value propositions and that reversing trajectory will require recapturing rank density lost since January 2026.

Notable Products

Mango Sorbet Infused Pre-Roll (1g) posted a -61.2% month-over-month drop while sliding to rank 3, whereas Huckleberry Pie Infused Pre-Roll (1g) surged +109.8% to rank 1, indicating sharp intra-portfolio rotation within the same format. With five of the top ten as Pre-Roll SKUs, the category is concentrated yet volatile, as Candy Pre-Roll 7-Pack (3.5g) fell -40.2% at rank 7 while Gas Pre-Roll 7-Pack (3.5g) in rank 4 inched up +6.5%, pointing to shifting mix between infused singles and multi-pack options. Edibles such as CBN:THC 2:1 Sour Berry Punch Gummies 10-Pack (100mg THC, 50mg CBN) at rank 2 grew +3.5% while CBD/THC 1:2 Blue Raspberry Gummies 10-Pack (100mg THC, 50mg CBD) at rank 6 added +3.1%, and Flower entries rounded out ranks 9–10 with Animal Tsunami (7g) and Gas Tax (7g), suggesting stability outside Pre-Roll volatility. The pattern implies Goodies (WA) is leaning into Pre-Roll-led shopper acquisition while maintaining steady Edible and Flower anchors, a mix that trades higher traffic for higher variance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.