May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

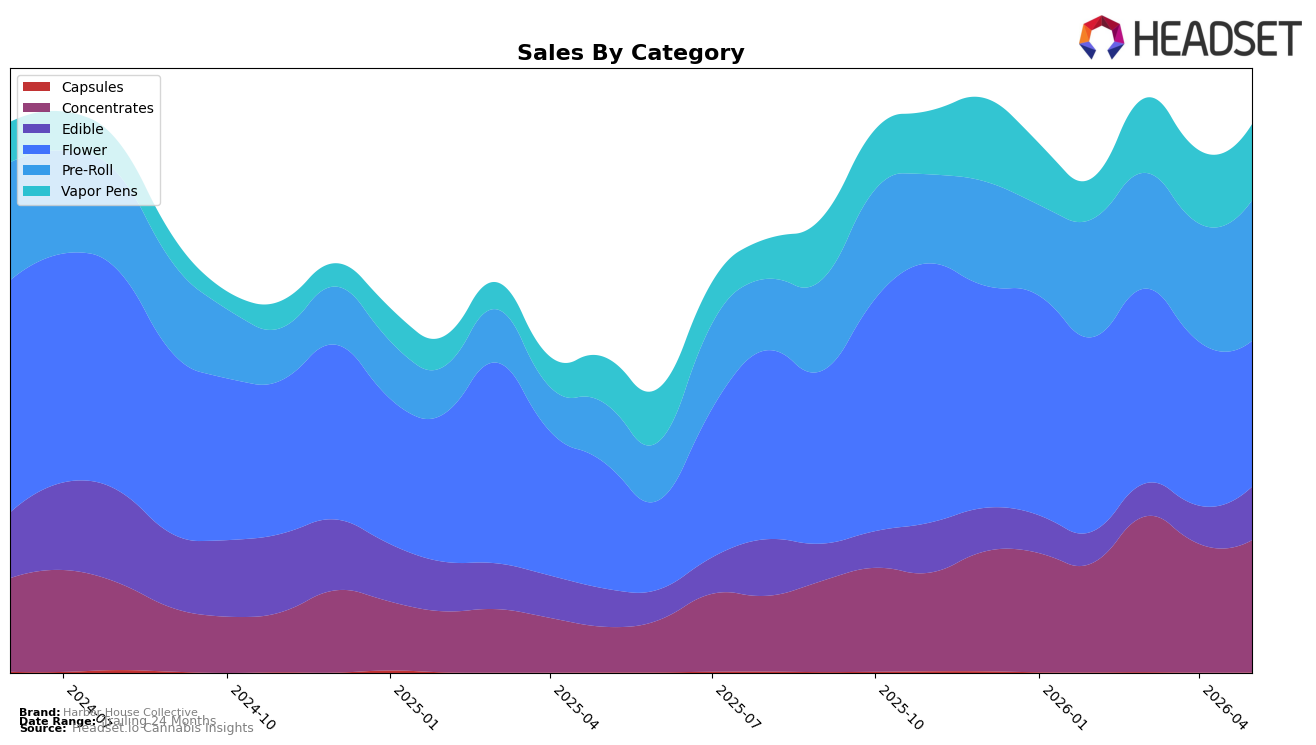

In May 2026, Harbor House Collective’s mix tilted toward Pre-Roll at 25.60% share and Flower at 26.55% share, while Concentrates held 24.10%, signaling a three-pillar portfolio where Flower remains the largest but is retreating month over month. Flower grew 15.45% year over year yet fell 11.11% month over month, whereas Pre-Roll surged 136.29% year over year and 18.99% month over month, and Concentrates advanced 189.31% year over year with a 2.70% month-over-month gain; this split implies demand is shifting from higher-priced Flower toward faster-turn, lower-price-per-unit form factors. Despite brand-level sales up 73.41% year over year and an average price down 15.27% year over year, the category momentum centers on Pre-Roll and Concentrates, indicating that volume expansion is being carried by accessible price points and inhalable formats rather than premium Flower positioning in Massachusetts.

The mix shift has positioning implications: a heavier Pre-Roll contribution alongside steady Vapor Pens (+66.10% year over year, +3.91% month over month) and fast-growing Edible (+39.01% year over year, +39.82% month over month) broadens Harbor House Collective’s entry pathways while Flower softness month over month risks diluting its anchor category credibility. With Flower ranked 51 in Massachusetts and its month-over-month decline of 11.11% against Pre-Roll’s 18.99% increase, Harbor House Collective’s near-term advantage lies in leaning into scale-friendly inhalables and replenishment categories, using Concentrates’ 189.31% year-over-year growth and Pre-Roll’s 25.60% share to offset Flower volatility and reposition the brand around value-accessible inhalable leadership.

Competitive Landscape

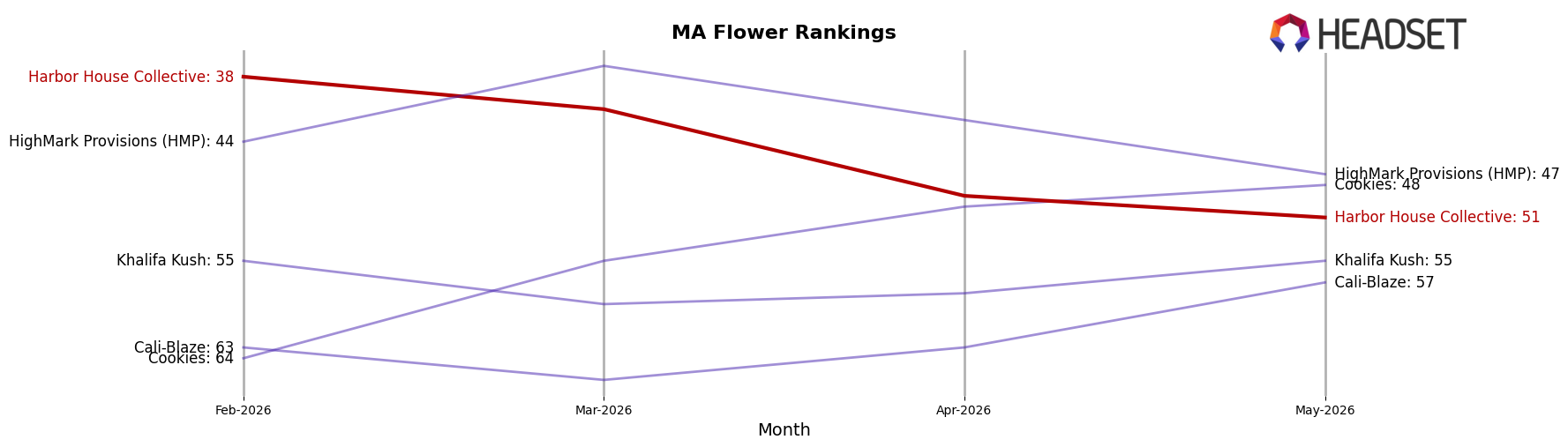

Harbor House Collective sits at rank #51 in Massachusetts Flower for May 2026, improving 10 positions from #61 year over year, but sliding 13 spots from #38 in February 2026 and down 23 from its #28 peak in November 2025; this mixed trajectory contrasts with Farmer's Cut rising from #3 to #1 alongside a 25.30% YoY sales increase and Root & Bloom jumping from #21 to #5 with 237.35% YoY growth, while Simply Herb slipped from #1 to #2 with a -17.50% YoY decline. The combination of a 10-rank YoY gain and a 13-rank three-month drop implies Harbor House Collective is gaining long-term ground but losing near-term shelf position to faster-accelerating competitors, signaling the need to counter momentum shifts rather than chase absolute peak rank recovery.

Notable Products

Sour Tangie Pre-Roll (1g) delivered the headline move in May 2026 with a 71.8% month-over-month increase and the number 1 rank, while Albariño Pre-Roll (1g) fell 36.0% and slid to rank 6. Orange 43 Pre-Roll (1g) in rank 2 inched up 1.5% MoM, and Aspen OG Pre-Roll (1g) at rank 4 rose 9.0% MoM, signaling mixed momentum within the same format. Eight of the top ten are Pre-Roll SKUs, concentrating the portfolio around a single format even as Albariño (3.5g) held rank 9 in Flower with a 4.6% MoM gain and $31,704 in sales. The pattern implies Harbor House Collective is leaning into Pre-Rolls for volume while Flower serves as a stabilizer, so assortment bets are clustering around high-velocity joints with selective strain-level pruning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.