Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

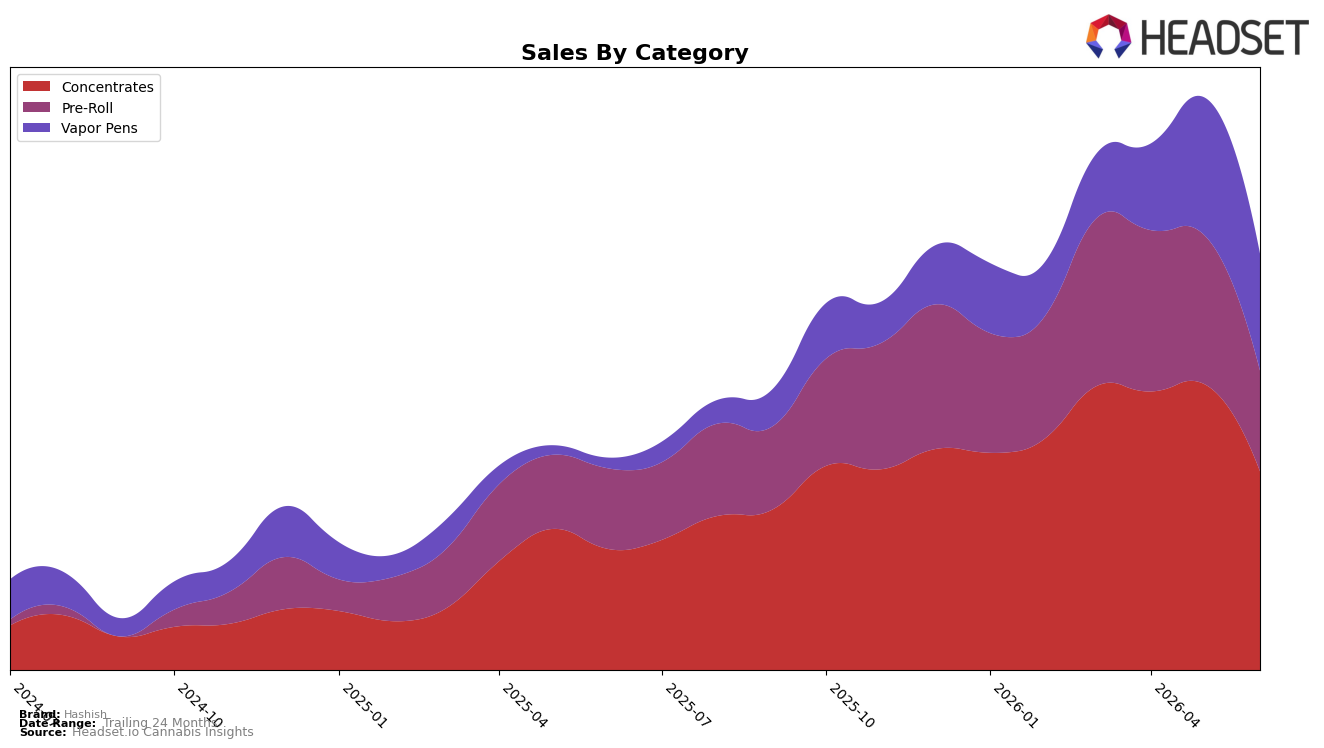

Hashish concentrated nearly half of June 2026 sales in Concentrates at 47.25% share with a 61.72% year-over-year gain, even as month-over-month declined 29.98%; Vapor Pens expanded to 28.27% share with a 689.45% year-over-year surge and a 14.62% month-over-month drop; Pre-Roll held 24.48% share with 23.62% year-over-year growth and a 31.34% month-over-month dip. Despite a 21.40% year-over-year rise in average price and a brand-level 90.11% year-over-year sales increase, the simultaneous month-over-month pullbacks across all three categories point to a mix that is levering multi-category expansion while absorbing short-term sequential volatility.

With Concentrates anchoring share at 47.25% and a California Concentrates rank of 8, the mix indicates a positioning that leans into a premium potency segment while using Vapor Pens’ 28.27% share and 689.45% year-over-year growth as a reach vehicle to diversify demand. The steeper month-over-month declines in Concentrates (-29.98%) and Pre-Roll (-31.34%) versus Vapor Pens (-14.62%) imply the brand’s resilience is currently tied more to inhalable convenience formats, suggesting pricing power from a 21.40% year-over-year average price lift is being sustained by breadth across form factors rather than single-category dependence.

Competitive Landscape

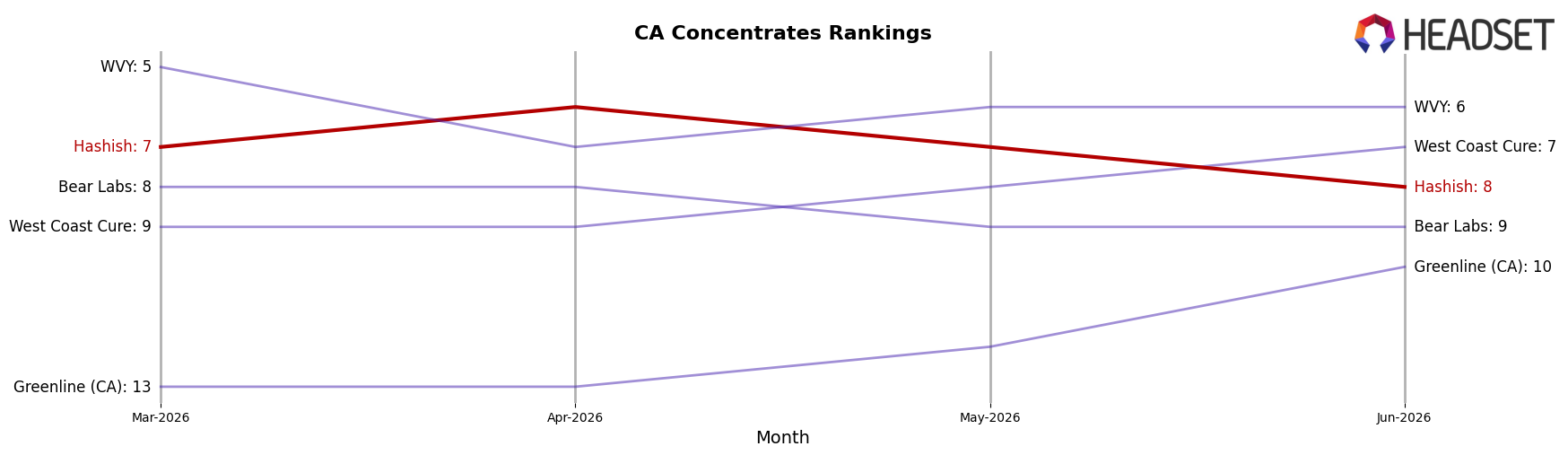

Hashish sits at rank #8 in CA Concentrates in June 2026, improving 3 positions from #11 year over year, but slipping 1 spot from #7 in March 2026 while remaining 2 places below its peak at #6 in April 2026; meanwhile, Raw Garden held at #1 year over year and 710 Labs moved up from #4 to #3 with a 24.7% YoY sales lift as Punch Extracts / Punch Edibles slid from #3 to #4 alongside a 29.1% YoY decline. The mix of a 3-rank YoY climb against leaders holding or gaining share and a 1-rank slip since March 2026 implies Hashish is advancing structurally but ceding near-term momentum to faster risers.

Notable Products

Blueberry Kush Rosin Infused Pre-Roll (1g) posted the standout move in June 2026 with a +385.8% month-over-month surge to rank 1, while Z Animal Rosin Infused Pre-Roll (1g) fell -69.2% to rank 2. Strawberry Guava Rosin Disposable (1g) slid -50.9% at rank 9, and Mars OG Rosin Infused Pre-Roll (1g) contracted -77.6% at rank 3. With three of the top four ranks held by Pre-Roll SKUs, the tilt toward infused pre-rolls implies Hashish is consolidating around a flagship format despite volatility within the lineup.

Baby Yoda Hash Hole Infused Pre-Roll (1.6g) debuted at rank 4 with $31,127, while Vapor Pens entries held mixed positions as Garlic Juice Live Rosin Disposable (1g) sat at rank 5 and Strawberry Guava Rosin Disposable (1g) dropped to rank 9. Concentrates clustered tightly with four SKUs between ranks 6 and 10, indicating a stable second pillar versus the sharper swings in Pre-Rolls and Vapor Pens. The pattern suggests a portfolio anchored by a breakout Pre-Roll leader and buffered by consistent Concentrates, positioning Hashish to prioritize infused pre-roll scale while using rosin-based Concentrates to smooth category risk.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.