Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Hillview Farms is stocked at 20 licensed dispensaries across New Jersey, with the deepest coverage in Hoboken, Atlantic City, Bordentown, Butler, and Elmwood Park. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

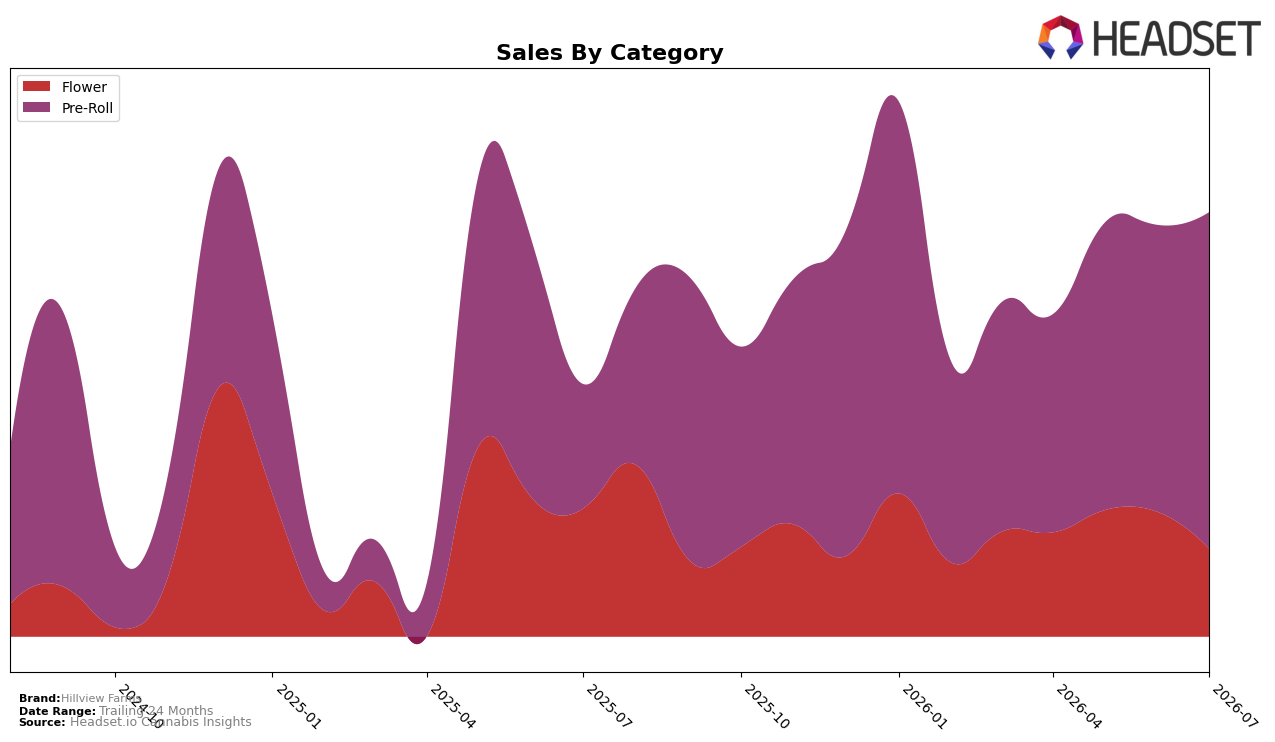

In July 2026, Hillview Farms concentrated 71.31% of sales in Pre-Roll, up 103.93% year over year and 13.49% month over month, while Flower fell to 28.69% share with a 19.31% YoY decline and a 17.99% MoM drop. The average price decreased 5.31% YoY to $23.26, alongside a lower Pre-Roll average price of 19.61 and a higher Flower average price of 43.31, signaling mix-driven price compression as volume migrates to the lower-priced format. With Pre-Roll ranked 21 in New Jersey and serving as the growth engine, the pattern implies the brand is trading customers into value-forward Pre-Rolls while ceding premium Flower velocity.

The sharp Pre-Roll expansion alongside a 13.49% MoM gain and a concurrent 17.99% MoM Flower contraction indicates Hillview Farms is anchoring on accessible price points to widen reach, even as the brand’s 41.80% YoY sales lift is disproportionately tied to a single category at 71.31% share. Given the 103.93% YoY surge in Pre-Roll versus a 19.31% YoY decline in Flower, and a rank position of 21 in New Jersey Pre-Roll, the implication is a positioning skewed toward scale over premium breadth; sustaining growth will likely require defending Pre-Roll rank while stabilizing Flower to reduce category concentration risk.

Competitive Landscape

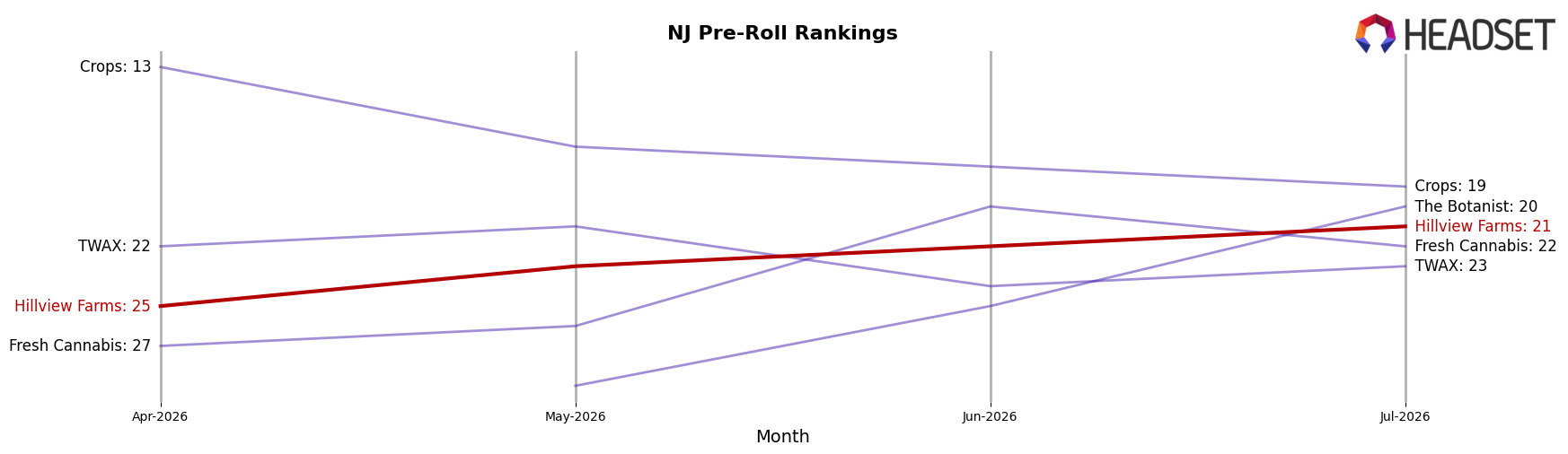

Hillview Farms sits at rank #21 in NJ Pre-Roll in July 2026, improving 12 positions from #33 year over year, while slipping 4 spots from #25 in April 2026; the brand’s historical ceiling was rank #14 in May 2025, indicating a recovery path but below its prior peak. In contrast, RYTHM moved up from #3 to #1 and Ozone advanced from #8 to #2, whereas Garden Greens eased from #1 to #3 and Full Tilt Labs surged from #22 to #4; this mix of upward and downward competitor shifts, combined with Hillview Farms’ 12-rank YoY climb and 4-rank QoQ dip, implies a mid-pack rebound that relies on stabilizing recent slippage to convert momentum into sustained top-20 presence.

Notable Products

Purple Jellato Pre-Roll 2-Pack (1g) led July 2026 with a 93% month-over-month surge and held rank 1, outpacing the next-best MoM mover Purple Diesel Pre-Roll 2-Pack (1g) at 46% and rank 7, which signals acceleration concentrated at the top and tail of the chart. Orange Sunshine Pre-Roll 2-Pack (1g) sat at rank 2 with a 12% MoM gain while Lemon OG Haze Pre-Roll 2-Pack (1g) at rank 3 moved just 4%, creating a widening spread where the category leader is compounding advantage against mid-tier growth. Eight of the top ten are Pre-Roll SKUs, and the only notable larger pack in the set, Cereal Milk Pre-Roll 5-Pack (2.5g), posted $15,844 at rank 8 while the related Cereal Milk Pre-Roll 2-Pack (1g) rose 21% at rank 5, implying format breadth is supporting the halo without displacing the 2-Pack focus. The pattern points to Hillview Farms leaning into Pre-Roll variety anchored by a breakout flagship, suggesting a strategy that prioritizes high-velocity 2-Packs while testing larger-pack participation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.