Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Incredibulk is stocked at 109 licensed dispensaries across Washington, with the deepest coverage in Seattle, Spokane, Tacoma, Vancouver, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

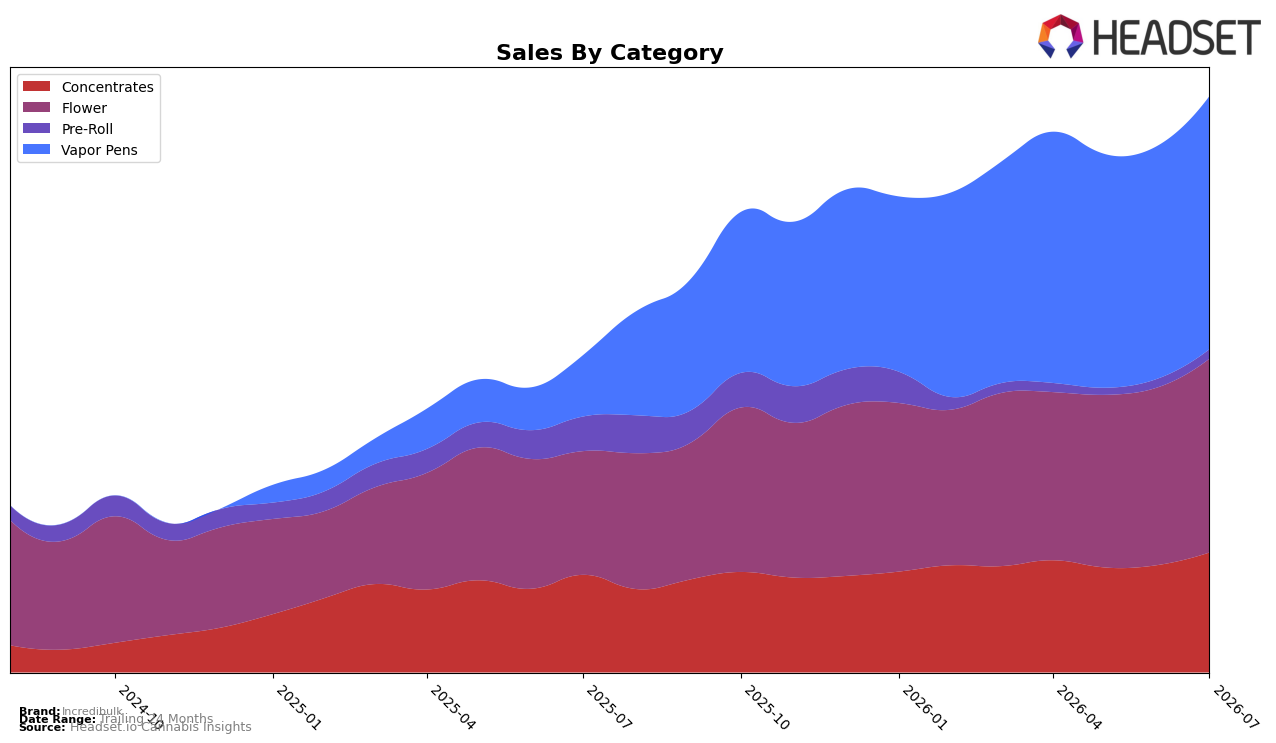

In July 2026, Vapor Pens held 43.94% share with 313.20% year-over-year growth and 8.63% month-over-month growth, while Flower accounted for 33.64% share with 56.75% year-over-year and 9.06% month-over-month gains; together these two categories made up 77.58% of mix and pulled overall brand sales up 81.83% year-over-year. Concentrates contributed 20.82% share with 22.95% year-over-year and 11.68% month-over-month growth, whereas Pre-Roll fell to 1.60% share with a -73.19% year-over-year decline but an 8.44% month-over-month uptick; the category skew toward Vapor Pens and Flower, alongside a 2.84% year-over-year average price increase to $6.53, implies Incredibulk is concentrating volume in faster-growing inhalable formats while letting Pre-Roll contract.

Within Vapor Pens, an 8.63% month-over-month lift paired with a 313.20% year-over-year surge, and a Washington Vapor Pens rank of 26, signals momentum in a scale category, while Flower’s 56.75% year-over-year and 9.06% month-over-month gains provide a stabilizing second pillar. The juxtaposition of Concentrates growing 11.68% month-over-month but only 22.95% year-over-year, versus Pre-Roll’s -73.19% year-over-year collapse and 1.60% share, indicates portfolio prioritization toward higher-velocity cartridges and core Flower; this mix positions Incredibulk to trade penetration for rank advancement in Washington by leaning into Vapor Pens while using Flower to buffer volatility.

Competitive Landscape

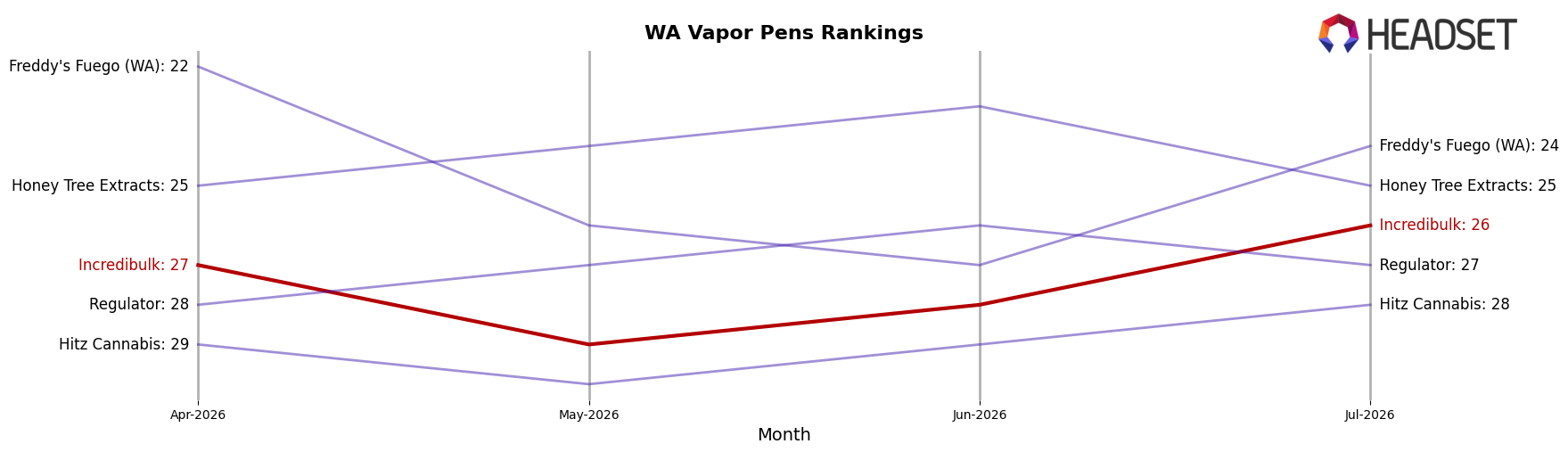

Incredibulk ranks #26 in Washington Vapor Pens in July 2026, improving 48 positions year over year from #74, and nudging up 1 spot since April 2026 from #27 to #26; this climb coincides with the brand hitting its peak rank of #26 in July 2026 while the category’s top tier reshuffled, as Mfused slipped from #1 to #2 with a -26.1% YoY sales change and Crystal Clear moved from #2 to #1 with a +12.6% YoY sales change. The juxtaposition of a 48-rank upward move for Incredibulk alongside a leadership handoff at the top implies share is opening in the mid-tier, positioning Incredibulk to convert recent rank momentum into sustained placement if it capitalizes on volatility above it.

Notable Products

Sour Blueberry Distillate Cartridge (1g) posted the steepest movement in July 2026 with a -11.4% month-over-month decline to rank 7, while Amnesia Haze Distillate Cartridge (1g) rose 13.7% to hold rank 1 and Zkittlez Distillate Cartridge (1g) gained 4.3% at rank 3. Dolato Distillate Cartridge (1g) advanced 27.5% to rank 4 and Trophy Wife Distillate Cartridge (1g) climbed 22.7% at rank 5, indicating middle-tier SKUs are compressing the gap with the top spot despite Dirty Girl Distillate Cartridge (1g) inching up just 1.7% at rank 2. Nine of the top ten are Vapor Pens, and that category concentration alongside Blueberry Pancake Wax (1g) at rank 10 with $9,291 suggests limited diversification outside inhalables. The pattern implies Incredibulk is leaning into breadth within Vapor Pens while pruning or repositioning underperforming terpene profiles like Sour Blueberry rather than expanding across form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.