Where to Buy

Just Flower is stocked at 128 licensed dispensaries across Maryland and Arizona, 99 of them in Maryland, with the deepest coverage in Baltimore, Silver Spring, Annapolis, Columbia, and Frederick. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

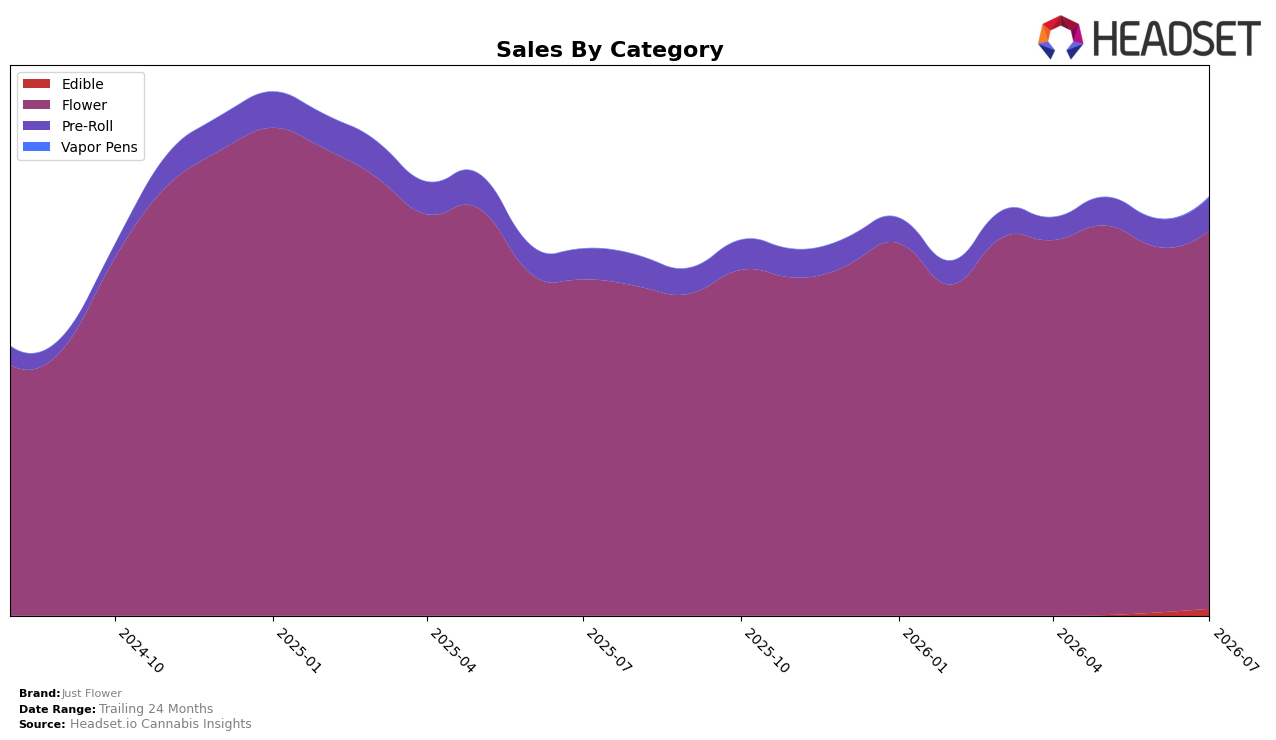

Market Insights Snapshot

In July 2026, Just Flower concentrated 90.30% share in Flower with 12.54% year-over-year growth and 3.55% month-over-month growth, while Pre-Roll held 7.83% share with 7.81% YoY and 17.63% MoM gains; Edible rose to 1.67% share on a 111.22% MoM jump, and Vapor Pens reached 0.20% share with a 698.50% MoM spike. The brand’s average price increased 5.32% YoY to $21.46 as Flower pricing sat higher at an average of 29.79, implying that mix shift toward higher-priced Flower supported revenue while rapid MoM expansions in smaller formats signal test-and-learn extensions rather than a structural pivot.

Being ranked 1 in Flower in Arizona alongside a 12.54% YoY category gain and a 3.55% MoM uptick indicates defensible leadership anchored in core Flower, while Pre-Roll’s 17.63% MoM growth and Edible’s 111.22% MoM surge point to incremental reach without diluting the 90.30% Flower share. The pattern suggests positioning as a Flower-first brand using small but fast-growing satellites—Pre-Roll at 7.83% share and Vapor Pens at 0.20% share with 698.50% MoM—to hedge against price compression and broaden entry points, keeping premium perception intact via higher average Flower pricing.

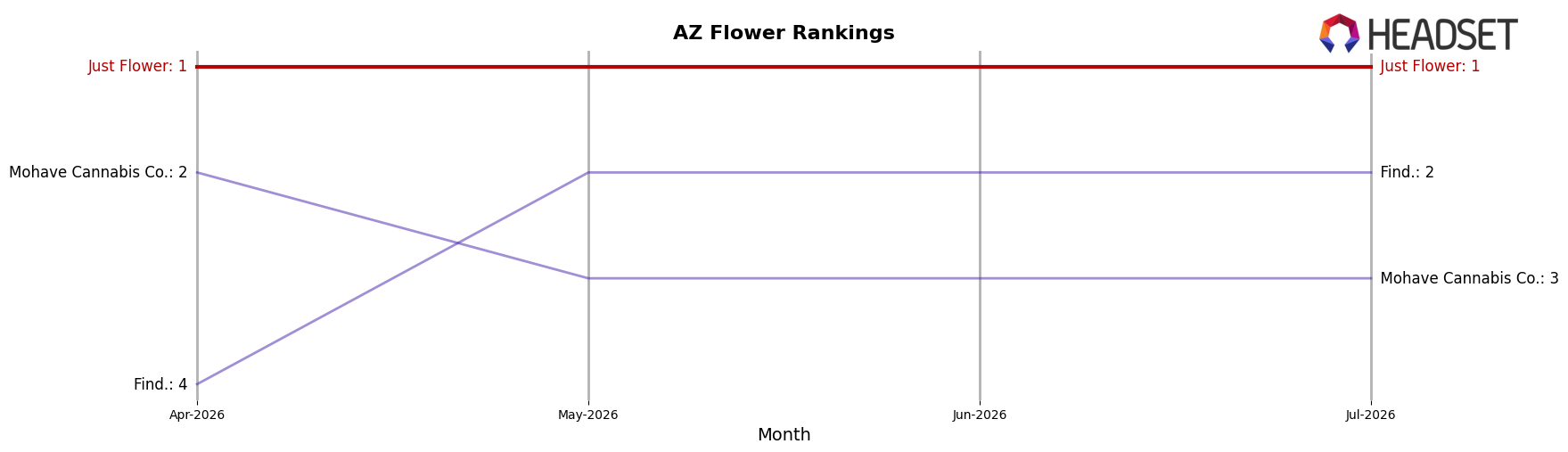

Competitive Landscape

Just Flower holds #1 in AZ Flower in July 2026, unchanged YoY from #1, while Find. sits at #2 with a 74.35% YoY sales increase and Fenix slid from #4 to #5 with a -6.90% YoY sales change; additionally, Brown Bag moved up from #5 to #4 alongside a 79.04% YoY sales jump and Mohave Cannabis Co. maintained #3 with an 8.93% YoY sales lift, indicating that holding #1 amid upward pressure from #2 and #4 implies Just Flower’s rank stability is being tested by faster climbers even as its top position persists.

Notable Products

Cherry Stout Pre-Roll 2-Pack (1g) posted the steepest movement in July 2026 with a -14.0% month-over-month drop, sliding to rank 8, while GMOzk (14g) surged +174% MoM to rank 2 with $228,307, indicating volatility concentrated at the edges of the lineup. Queen's Delight Pre-Roll 2-Pack (1g) rose +23.7% MoM at rank 6 as Pre-Rolls tallied four of the top ten positions, yet Flower SKUs held the higher ranks at 2, 3, 4, 5, 9, and 10. GMOzk (14g) at rank 2 and the Pre-Roll declines at rank 8 together imply a tilt toward larger-pack Flower driving visibility while value-oriented Pre-Rolls require SKU-level pruning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.