Market Insights Snapshot

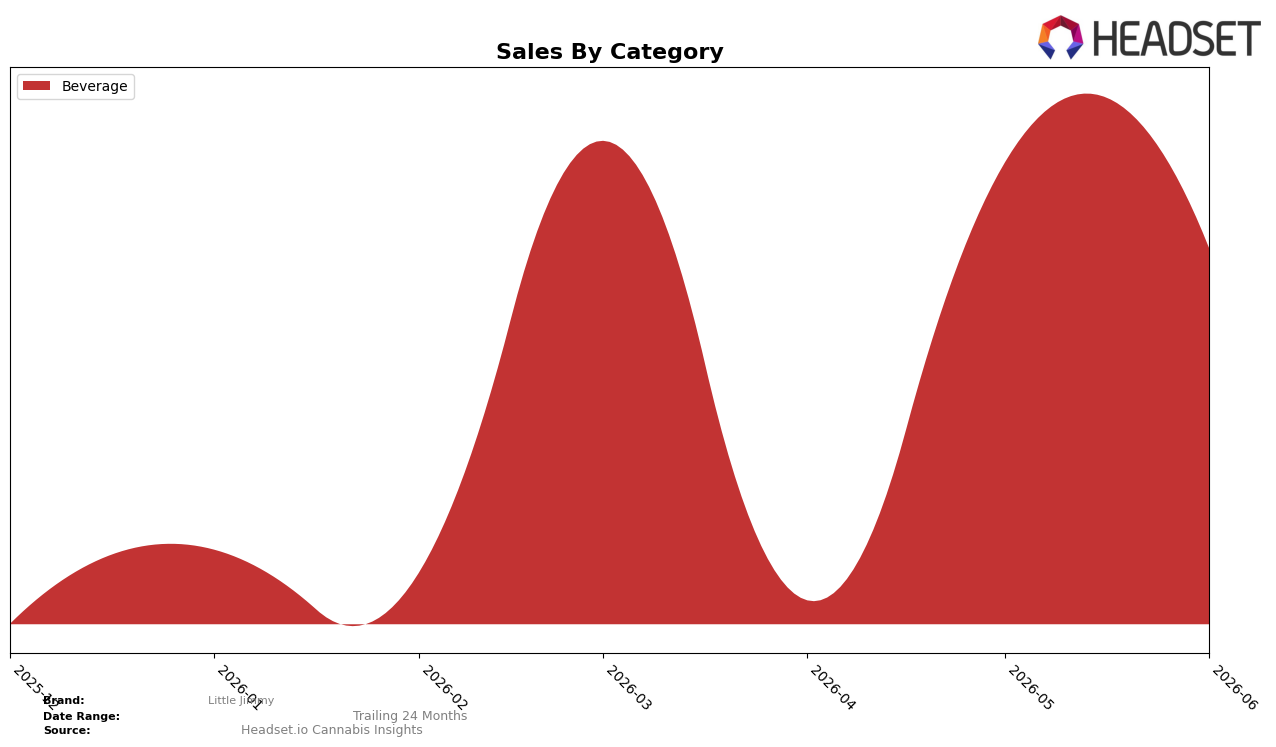

In June 2026, Little Jimmy operated as a single-category brand with Beverage holding 100.0% share, and a month-over-month decline of 17.46% coinciding with an average price of $4.02 and no reported year-over-year figure. With no intra-brand category offsets and no rank provided in Maryland Beverage, the 100.0% concentration amplifies exposure to category volatility while the 17.46% MoM downswing indicates demand or distribution softness rather than mix dilution. The pattern implies that single-category concentration is translating into higher short-term variability, where any 10–20% swing in the core category directly transmits to total brand performance without buffer.

The 100.0% Beverage dependency paired with a 17.46% month-over-month contraction suggests positioning risk: Little Jimmy is effectively indexed to Beverage seasonality and retailer shelf decisions, and a lack of adjacent-category presence removes cross-purchase lift. In Maryland, the absence of a rank alongside a full-category share and a double-digit monthly decline implies limited visibility gains from the current SKU strategy, pushing the brand toward a defensive stance where improving velocity per facing or selective flavor/format expansion within Beverage would matter more than breadth. The implication is that maintaining price discipline around the $4.02 average while engineering even a 5–10% MoM recovery within Beverage would disproportionately lift total brand results given the 100.0% mix.

Competitive Landscape

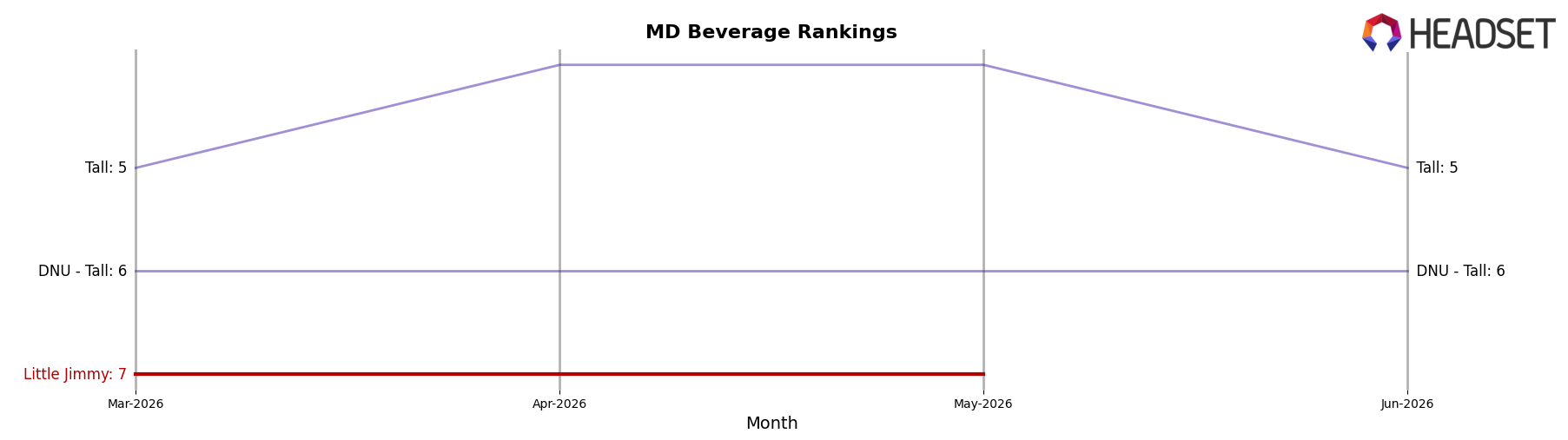

Little Jimmy sits at #7 in MD Beverage in June 2026, unchanged from #7 three months prior, marking a flat rank trajectory even as peers reshuffle; meanwhile, Keef Cola held #1 year over year with 16.35% sales growth and Vibations climbed from #4 to #3 on 116.95% growth, while Dixie Elixirs slipped from #3 to #4 despite 2.07% growth. Against this backdrop, Little Jimmy’s peak rank of #7 in June 2026 coincides with competitors maintaining or improving positions—Sunnies by SunMed stayed #2 with 44.74% growth and Tall held #5 with 96.84% growth—implying that holding #7 signals stable placement but also mounting pressure to convert share as faster-rising brands compress headroom above.

Notable Products

CBN/THC 1:1 Sereni Tea Shot (10mg CBN, 10mg THC, 12oz, 355ml) led June 2026 despite a -16.2% month-over-month drop and holding rank 1, while Paradise Tea Shot (10mg THC, 12oz, 355ml) fell -20.3% and sat at rank 3. CBD/THC/CBG/CBC Tranquili Tea Shot (20mg CBD, 10mg THC, 10mg CBG, 5mg CBC) posted the steepest slide at -26.4% and rank 4, contrasting with Immuni Tea Shot (10mg) at rank 2 with a smaller -6.5% decline. With all top-4 SKUs concentrated in Beverage and total leader sales at $2,594, the pattern implies reliance on a single format where share is shifting toward daily-wellness profiles over heavier multi-cannabinoid mixes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.