Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Local Roots is stocked at 56 licensed dispensaries across Massachusetts, with the deepest coverage in Boston, Quincy, Worcester, Bridgewater, and Brookline. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

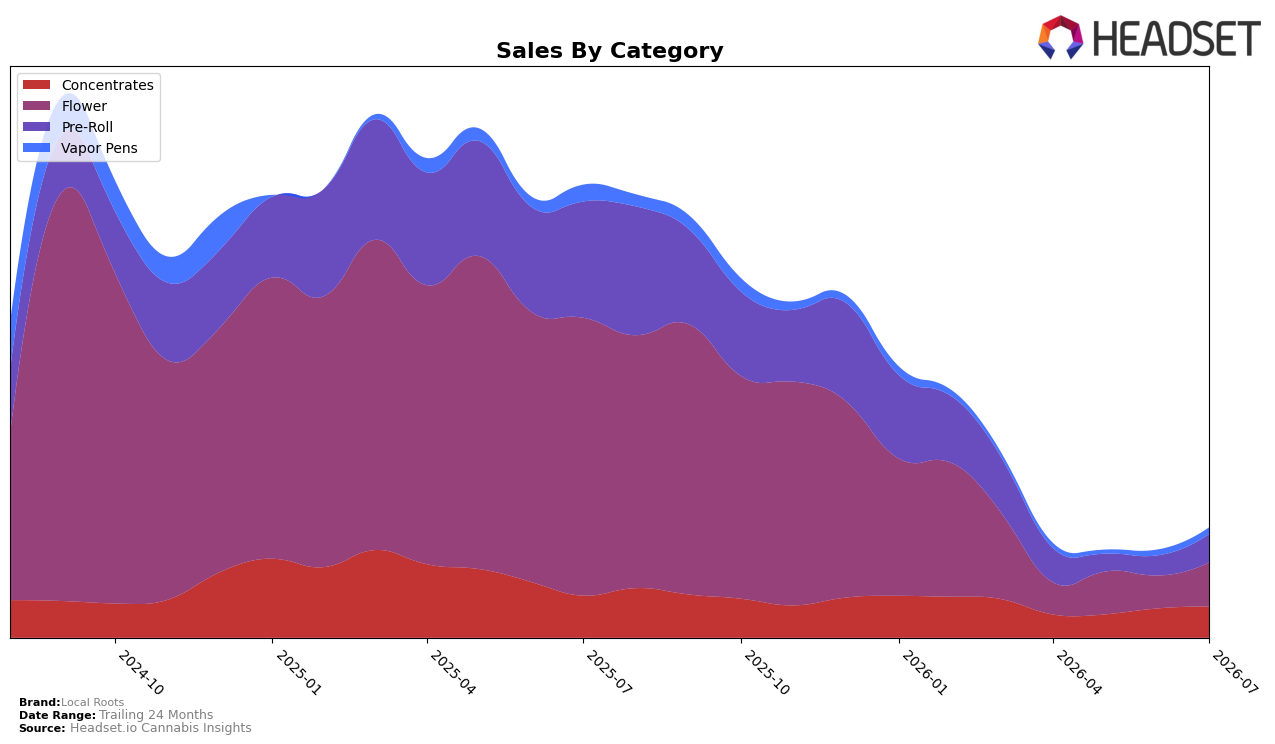

Local Roots concentrated its July 2026 revenue in Flower at 40.08% share and Pre-Roll at 25.66%, while Concentrates held 28.20% and Vapor Pens 6.05%; within this mix, Flower fell year over year by 84.08% and Pre-Roll by 75.61%, even as month over month both rebounded 34.42% and 40.99%, respectively. Concentrates contracted 26.20% year over year but rose 5.95% month over month, and Vapor Pens declined 60.41% year over year with a 14.32% monthly lift; in parallel, the average price increased 4.15% year over year and the Flower rank in Massachusetts sat at position 98, indicating a portfolio leaning on categories with steep annual declines but short-term recovery pulses.

The category shifts point to a tactical pivot: the outsized month over month gains in Pre-Roll at 40.99% and Flower at 34.42% within a portfolio where these two categories represent 65.74% share suggest demand elasticity to promotional or assortment moves, while the smaller 5.95% lift in Concentrates and 14.32% in Vapor Pens imply narrower momentum. Given a 98 rank in Massachusetts Flower alongside an 84.08% year over year Flower decline and a 4.15% average price increase, the near-term opening is to prioritize velocity over ticket by deepening Pre-Roll breadth and selectively defending Flower SKUs, because the mix now rewards quick-turn formats even as legacy Flower equity lags on an annual basis.

Competitive Landscape

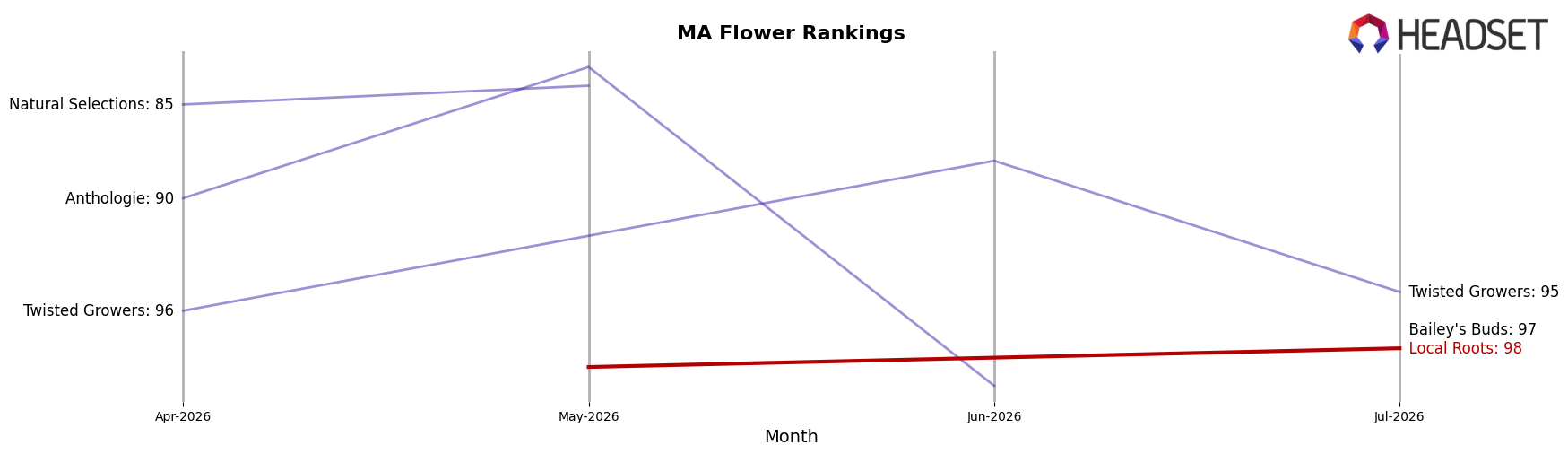

Local Roots sits at rank #98 in MA Flower for July 2026, down 70 positions year over year from #28, while improving 16 spots versus April 2026 when it was #114; the brand’s historical ceiling of #22 in September 2024 contrasts with a market where Farmer's Cut advanced from #4 to #1 and Root & Bloom climbed from #10 to #5. With competitors like Perpetual Harvest holding #3 and High Supply / Supply at #4, Local Roots’ recent quarter-on-quarter rank gain of 14% alongside a 250% year-over-year rank decline rate by position count implies the brand has stabilized off a low but must reverse longer-term share loss to re-enter the top 50.

Notable Products

Peyote Cookies Pre-Roll (1g) delivered the headline move in July 2026 with a 205% month-over-month jump that pushed it to rank 1, while Jack Skunk Pre-Roll (1g) fell 27% and slid to rank 5. Pura Vida Pre-Roll (1g) also surged 177% to rank 3, and together with two other pre-rolls in the top six signals a concentration of pre-rolls across the top ten. In concentrates, GG4 Live Hash Rosin (1g) rose 52% to rank 7 and Ice Cream Cake Brick Hash (1g) climbed 58% to rank 10, indicating parallel momentum outside pre-rolls. The pattern implies Local Roots is tilting its mix toward faster-cycling inhalables where sharp MoM gains can convert into share at the very top of the ranking, using breakout pre-rolls to anchor visibility while concentrates provide a secondary growth lane.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.