Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

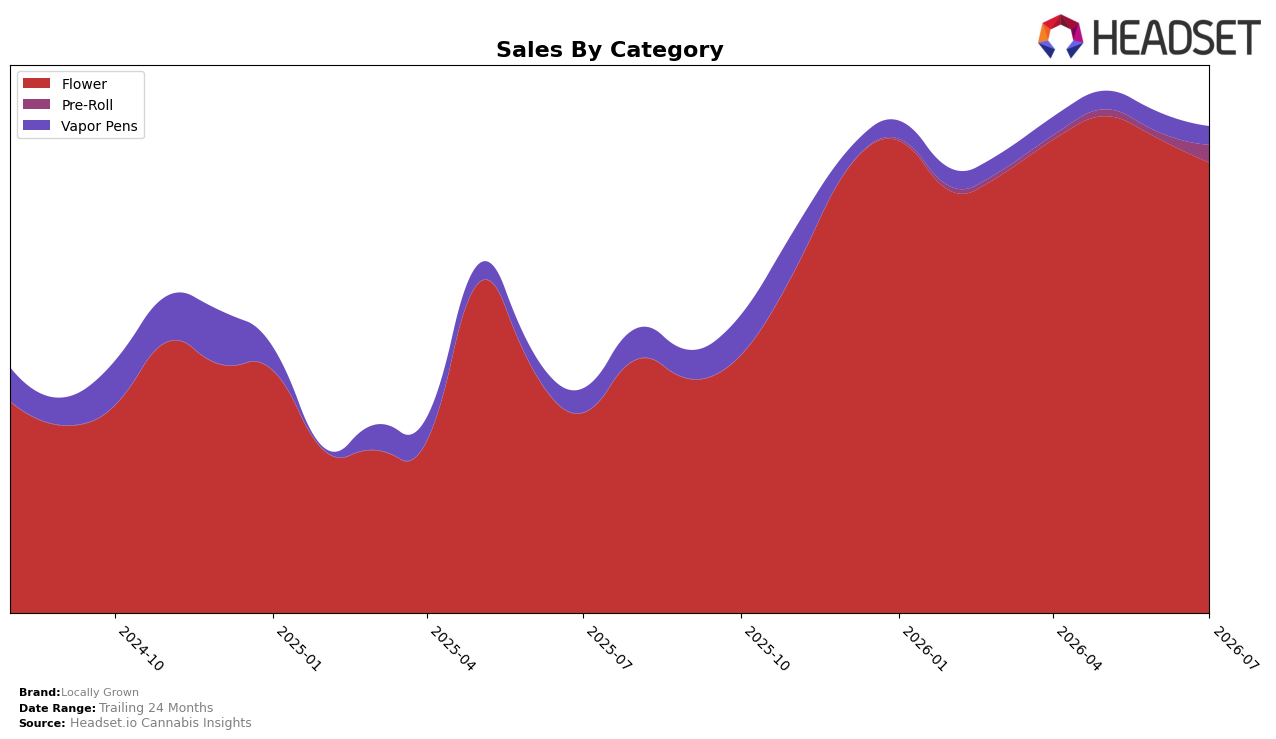

Locally Grown’s category mix in July 2026 was dominated by Flower at 92.64% share, with Flower sales up 125.29% year over year but down 5.12% month over month, signaling reliance on a single engine even as monthly velocity cooled. Vapor Pens held 3.76% share with a 23.06% YoY decline and a 6.65% MoM drop, while Pre-Roll reached 3.59% share after a 182.63% MoM surge despite lacking a YoY baseline, indicating a rapid near-term pivot. With average price up 22.80% YoY to $13.97 alongside a Flower average price of $14.99, the mix shift pairs price expansion with unit concentration, implying margin headroom is tied primarily to Flower while Pre-Roll adds volume ballast.

The shifts imply a positioning concentrated in value-forward Flower with selective expansion bets: a rank of 11 in Flower in Ohio sets a clear battleground, while the 5.12% MoM Flower dip and 182.63% MoM Pre-Roll spike point to diversification as the practical hedge. The 23.06% YoY contraction in Vapor Pens against a 125.29% YoY Flower rise suggests de-emphasis of hardware-dependent formats in favor of combustion-led demand, and the 22.80% YoY price lift with a 3.59% Pre-Roll share indicates pricing power remains centered in Flower as Pre-Roll builds trial. The pattern implies Locally Grown should treat Pre-Roll as the gateway for incremental share capture while defending Flower in Ohio to convert rank 11 into durable distribution and pricing leverage.

Competitive Landscape

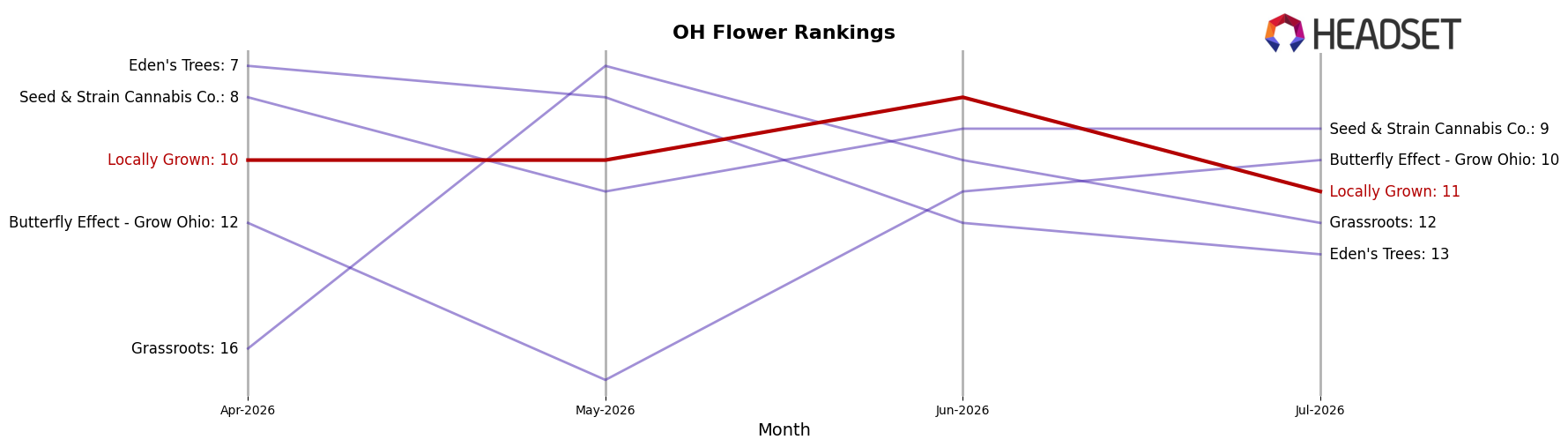

Locally Grown sits at rank #11 in OH Flower in July 2026, improving 8 positions from #19 year over year, while slipping 1 spot from #10 in April 2026 and down from its #8 peak in June 2026; in the same window, RYTHM advanced from #6 to #1 with 74.99% YoY sales growth and Klutch Cannabis jumped from #21 to #3 on 403.04% YoY growth, indicating that Locally Grown’s middle-tier rise is outpaced by leaders gaining share faster. With Riviera Creek moving from #1 to #2 alongside a -15.97% YoY sales decline and Certified (Certified Cultivators) climbing from #14 to #5 on 92.83% growth, Locally Grown’s modest YoY rank gain paired with a post-peak pullback implies a consolidation phase where maintaining top-10 access will require pacing against faster-rising rivals rather than incremental improvement alone.

Notable Products

#72 (2.83g) posted the standout move in July 2026 with +135.0% MoM, vaulting to rank 1, while Jack Le'Pew (2.83g) plunged -55.7% MoM to rank 9; this split points to sharp polarization within the same size tier. Flex Fuel (2.83g) also contracted -26.9% MoM at rank 8 as Caveman (2.83g) slipped -6.5% to rank 6, and Flower accounted for all top-10 SKUs, concentrating assortment risk in a single category. With Mad River Kush (2.83g) and Tahoe Jack (2.83g) holding ranks 2 and 3 alongside the #1 surge, the power is consolidating at the top while mid-pack volatility rises, implying Locally Grown is skewing toward a few hero Flower SKUs and away from breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.