Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

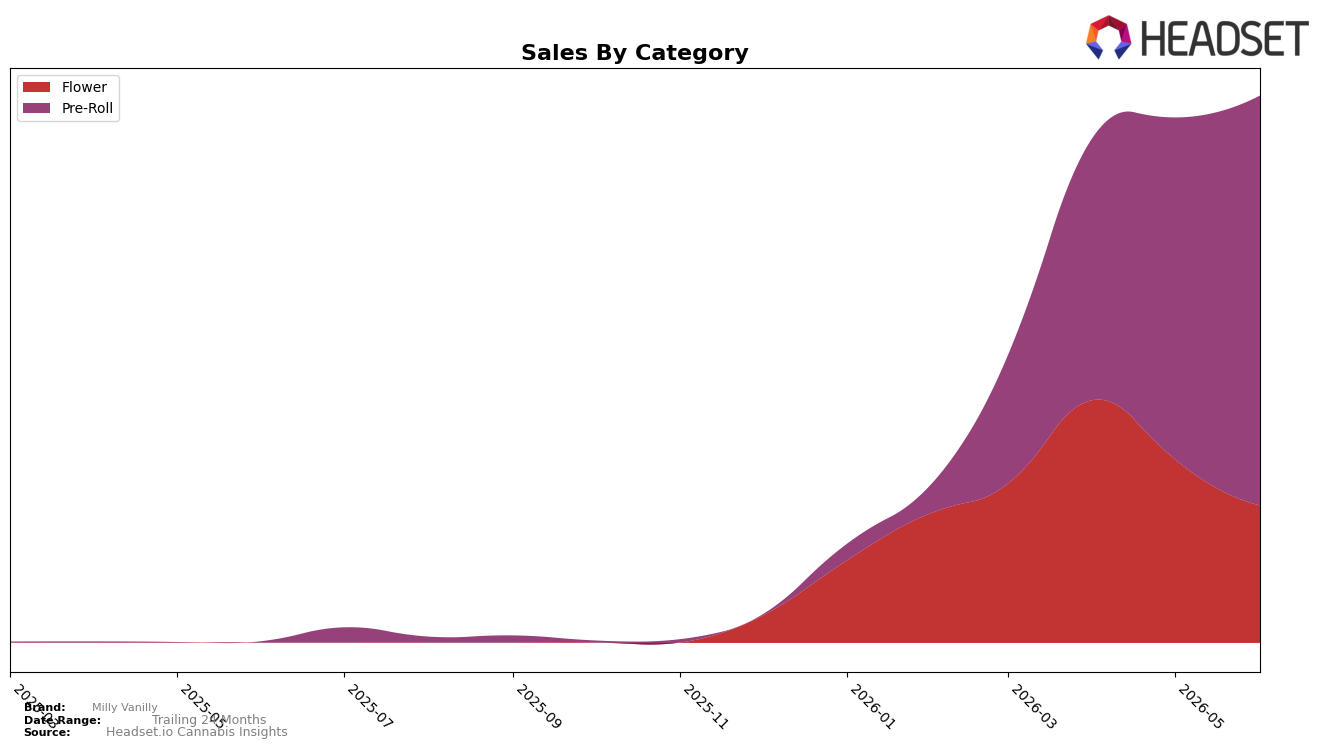

In June 2026, Milly Vanilly concentrated 74.93% of sales in Pre-Roll while Flower accounted for 25.07%, a mix that shifted month over month as Pre-Roll grew 19.87% and Flower fell 25.14%. Year over year, Pre-Roll expanded 41,814.53% alongside a brand-level average price decline of 39.75%, anchoring a volume-led expansion that elevated Pre-Roll’s role despite a higher average price in Flower at $38.72 versus $11.36 in Pre-Roll. The pattern implies the brand is actively trading into lower-priced, higher-velocity Pre-Roll to gain scale, accepting mix pressure away from higher-ticket Flower to drive reach and basket incidence.

That tilt toward Pre-Roll places Milly Vanilly as a value-access player within the format, with category share consolidation aligning to rank 15 in Pre-Roll in Saskatchewan and a 19.87% month-on-month Pre-Roll lift outpacing the 25.14% decline in Flower. The 41,814.53% year-over-year Pre-Roll surge combined with a 39.75% brand-wide average price drop indicates the positioning leans on elastic price bands and pack/size architecture, implying future gains will depend on sustaining price ladders in Pre-Roll while selectively defending higher-margin Flower to avoid profitability drag from a 74.93% Pre-Roll-heavy mix.

Competitive Landscape

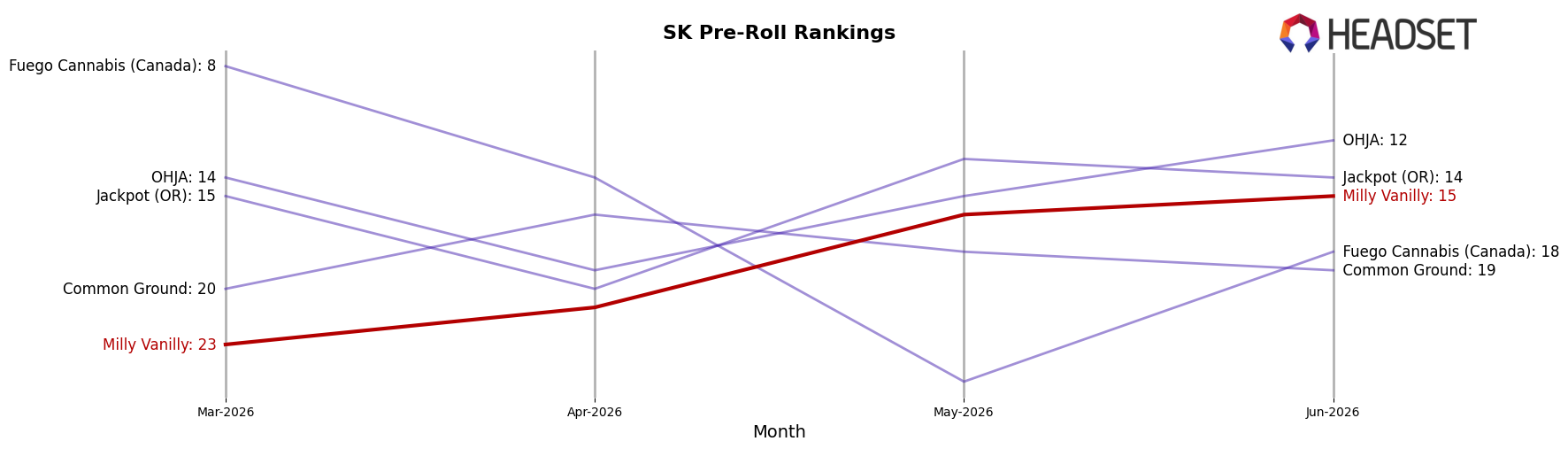

Milly Vanilly sits at rank #15 in SK Pre-Roll in June 2026, improving 8 positions from #23 in March 2026 while also marking a peak rank of #15 in June 2026; with no year-over-year rank available, the short-term climb stands out against competitors where Doobie Snacks jumped from #9 to #3 and Back Forty / Back 40 Cannabis held #1 with 134% YoY sales growth. Relative to Spinach at #4 and General Admission at #5, Milly Vanilly’s move from #23 to #15 over three months contrasts with Spinach’s steadier placement near #3–#4 and General Admission’s #4 to #5 slippage, implying Milly Vanilly is entering the competitive mid-tier from below rather than displacing entrenched leaders.

Notable Products

Inda Couch Pre-Roll 2-Pack (1g) posted the largest movement in June 2026 with a 177% month-over-month surge that vaulted it to rank 3, while Soft Serve Pre-Roll 2-Pack (1g) fell 34% to rank 4. The top two positions were held by Soft Serve Pre-Roll 5-Pack (2.5g) at rank 1 despite a 10% decline and Inda Couch Pre-Roll 5-Pack (2.5g) at rank 2 with a 7% dip, indicating a reshuffle within formats rather than a category exit. With eight of the top ten as Pre-Roll SKUs and the Inda Couch Pre-Roll 10-Pack (5g) up 30% to rank 5 versus Soft Serve Pre-Roll 10-Pack (5g) up 18% to rank 6, multi-pack momentum is tilting toward Inda Couch on velocity.

Outside Pre-Rolls, Indacouch Milled (10g) rose 45% to rank 7 while Soft Serve Milled (10g) declined 27% to rank 10, concentrating flower gains in one line and losses in the other. Two newly charting infused singles entered at ranks 8 and 9 without month-over-month baselines, and the category mix kept Pre-Rolls at 80% of the top ten even as the leading Soft Serve 5-Pack generated $30,843. The pattern implies Milly Vanilly is consolidating around Inda Couch value packs and milled formats while Soft Serve shifts toward fewer but higher-rank flagship pre-rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.