Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Mojo (Edibles) is stocked at 91 licensed dispensaries across Michigan and Maine, 74 of them in Michigan, with the deepest coverage in Detroit, New Buffalo, Battle Creek, Coldwater, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

In July 2026, Mojo (Edibles) concentrated 82.63% of sales in Edible with year-over-year down 13.29% and month-over-month essentially flat at -0.07%, while Vapor Pens expanded to 16.39% share with year-over-year up 6.44% and month-over-month up 24.23%. Smaller lines were volatile: Concentrates held 0.76% share with year-over-year down 80.82% but month-over-month up 130.12%, and Pre-Roll sat at 0.22% share with year-over-year up 99.66% but month-over-month down 84.40%. With average price up 7.55% year-over-year to one price point ($10.05) alongside a brand-level sales decline of 12.88% year-over-year, the pattern implies the core Edible base is shrinking while secondary categories are absorbing incremental, more price-tolerant demand.

The category mix shifts suggest a repositioning opportunity: Edible softness at -13.29% year-over-year against a 24.23% month-over-month uplift in Vapor Pens indicates portfolio elasticity away from the core toward inhalables, and a 130.12% month-over-month rebound in Concentrates despite an 80.82% year-over-year drop points to episodic activation rather than sustained pull. Holding rank 19 in Edible in Michigan while Vapor Pens gain share to 16.39% implies the current pricing stance (+7.55% year-over-year) is better aligned with faster-moving non-edible formats, so maintaining Edible relevance likely requires mix-led innovation or price architecture changes rather than relying on transient spikes like the 99.66% year-over-year surge in Pre-Roll.

Competitive Landscape

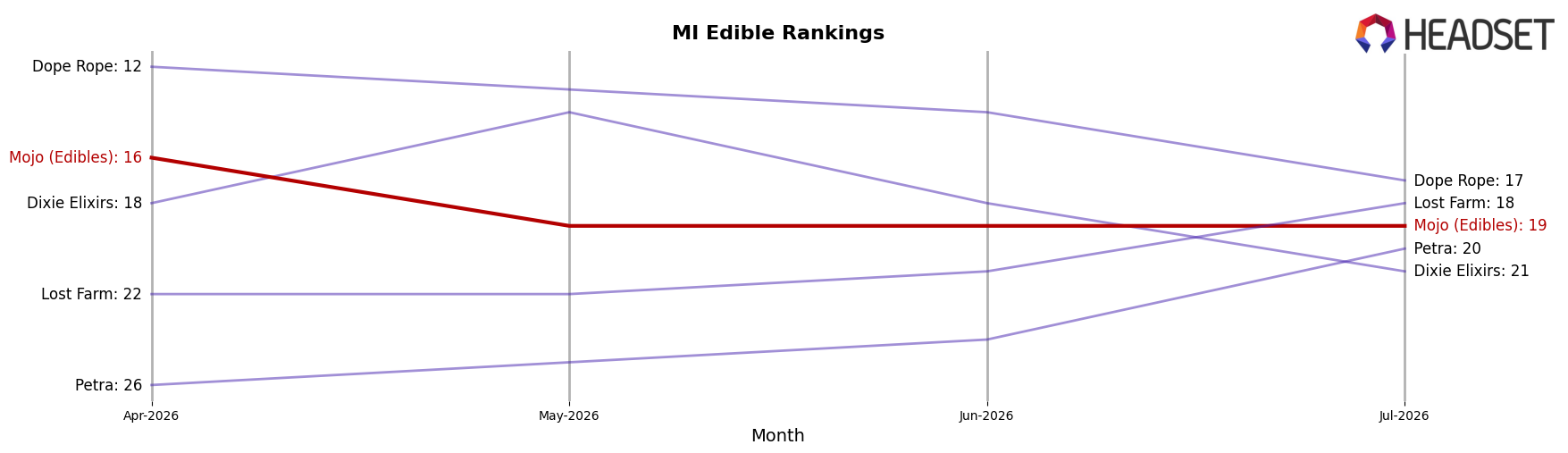

Mojo (Edibles) sits at rank #19 in MI Edible for July 2026, down 2 positions from #17 year over year and 3 spots from #16 in April 2026, after peaking at #13 in March 2026; meanwhile, category leader Wyld remains #1 with a -23.3% YoY sales change and Camino climbed from #4 to #3 with +12.9% YoY sales, indicating Mojo’s relative slippage is occurring while the top tier is bifurcating between contraction and selective gains. The combination of a 2-rank YoY decline and a 3-rank drop since April 2026, alongside MKX Oil Company drifting from #3 to #4 with +4.6% YoY sales and Choice holding #2 with a -0.4% YoY change, implies Mojo’s rank trajectory is being pressured by competitors that are either stabilizing at the top or gaining share despite broader softness, pointing to a need for share defense rather than short-term rebound expectations.

Notable Products

Nuggy Caramel Peanut Bites Chocolates 10-Pack (200mg) delivered the largest month-over-month surge at +54.8% to rank 1, while Cookies & Cream Chocolate Bites (200mg) fell -12.7% at rank 4, signaling a widening gap between a breakout leader and a sliding mid-tier SKU. The steepest decline came from Caramel Filled Milk Chocolate Bites 10-Pack (200mg) at -30.8% in rank 5 alongside a -46.3% drop for Peanut Butter Chocolate Mini Bites 10-Pack (200mg) in rank 7, whereas Cookie Bars Chocolate Bites (200mg) rose +39.3% to rank 2, concentrating momentum at the very top. With eight of the top ten as chocolate bite formats and only modest movement from Choco Gummies - Blueberry Dark Chocolate Gummies 10-Pack (200mg) at +0.8% in rank 6, July 2026 performance points to a portfolio tilt toward high-velocity chocolate bites anchored by a single flagship, implying near-term gains will depend on sustaining Nuggy Caramel Peanut Bites and one to two follower SKUs rather than broad-line growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.