Apr-2026

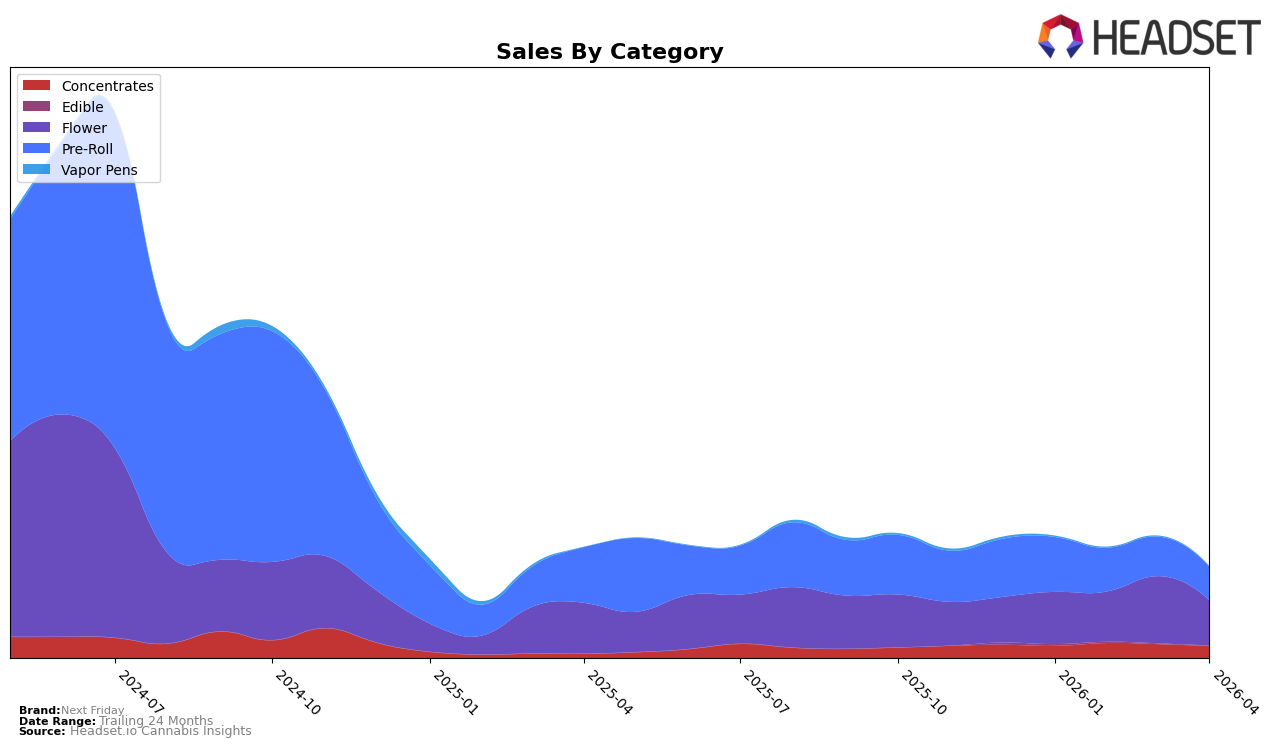

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

Next Friday's performance across various categories and regions shows a mix of both challenges and opportunities. In Alberta, the brand's presence in the Flower category has seen a decline, dropping from 61st in January 2026 to 83rd by April 2026. This trend indicates that Next Friday is struggling to maintain its position among the top competitors in this category within the region. Similarly, the Pre-Roll category in Alberta also reflects a downward trend, where the brand did not make it into the top 30 rankings by April 2026, suggesting a need for strategic adjustments. On a more positive note, Saskatchewan shows upward momentum in the Flower category, moving from outside the top 30 in January to securing the 41st spot by April. This suggests a growing acceptance and potential for market share expansion in this province.

In Ontario, Next Friday's performance in the Concentrates category has remained relatively stable, maintaining a consistent rank around the 50s, although there was a slight drop to 58th in April 2026. This stability might indicate a loyal customer base or consistent demand, although the drop in ranking could be a signal to enhance competitive strategies. The Flower category in Ontario, however, presents a different picture, with the brand entering the top 100 at the 85th position in March 2026. Despite not being in the top 30, this entry could be seen as a foothold in a competitive market, offering room for growth. Overall, while challenges are evident in certain regions and categories, there are also indications of potential growth and areas where Next Friday could capitalize on emerging opportunities.

Competitive Landscape

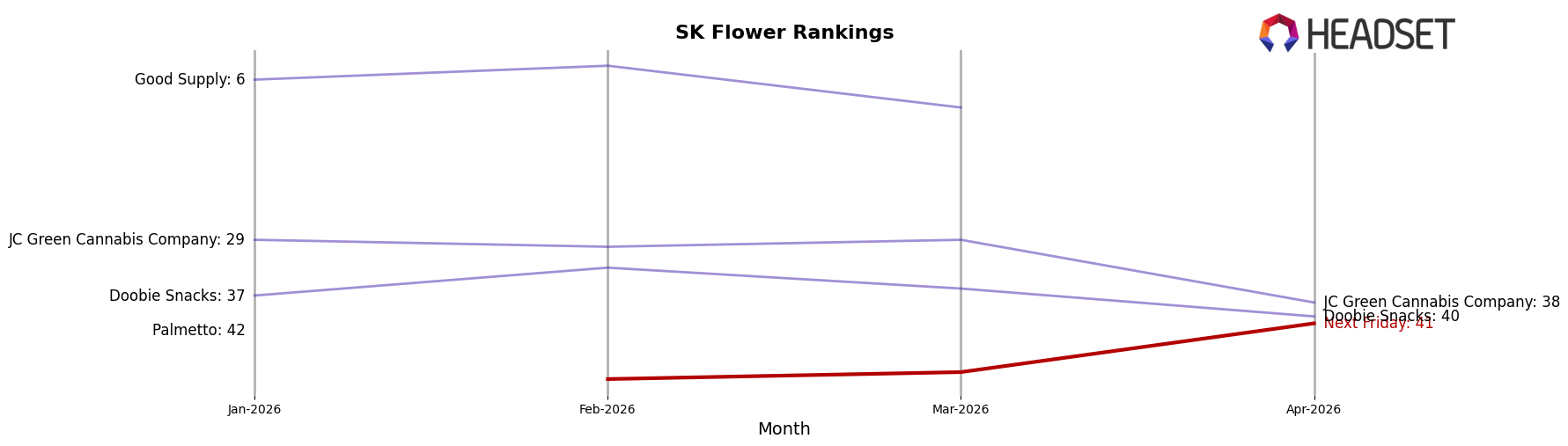

In the competitive landscape of the Flower category in Saskatchewan, Next Friday has shown a notable upward trajectory in its rankings, moving from not being in the top 20 in January 2026 to securing the 41st position by April 2026. This positive trend in rank is accompanied by a significant increase in sales, indicating a growing consumer preference for Next Friday's offerings. In contrast, Good Supply, which started strong in January 2026 at 6th place, experienced a decline, dropping out of the top 20 by April 2026. Meanwhile, JC Green Cannabis Company and Doobie Snacks have shown relatively stable performances, with JC Green Cannabis Company ending at 38th and Doobie Snacks at 40th in April 2026. The data suggests that while Next Friday is gaining momentum, established brands like Good Supply are facing challenges in maintaining their market position, potentially opening up opportunities for Next Friday to capture more market share.

Notable Products

In April 2026, the top-performing product for Next Friday was the Burner Phone Special Pre-Roll (0.5g) in the Pre-Roll category, maintaining its leading position from March 2026. The Mutant Tire Fire Pre-Roll (0.5g) held steady in second place, consistent with its ranking in March. Notably, the Next Friday Pre-Roll (0.5g) emerged in third place, achieving sales of 1089 units, marking its first appearance in the rankings. The Chameleon Connoisseurs Pre-Roll 5-Pack (2.5g) experienced a slight drop, moving from third to fourth place compared to the previous month. Lastly, the Blueberry Fuego Pre-Roll 3-Pack (1.5g) entered the rankings in fifth place for the first time in April 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.