Market Insights Snapshot

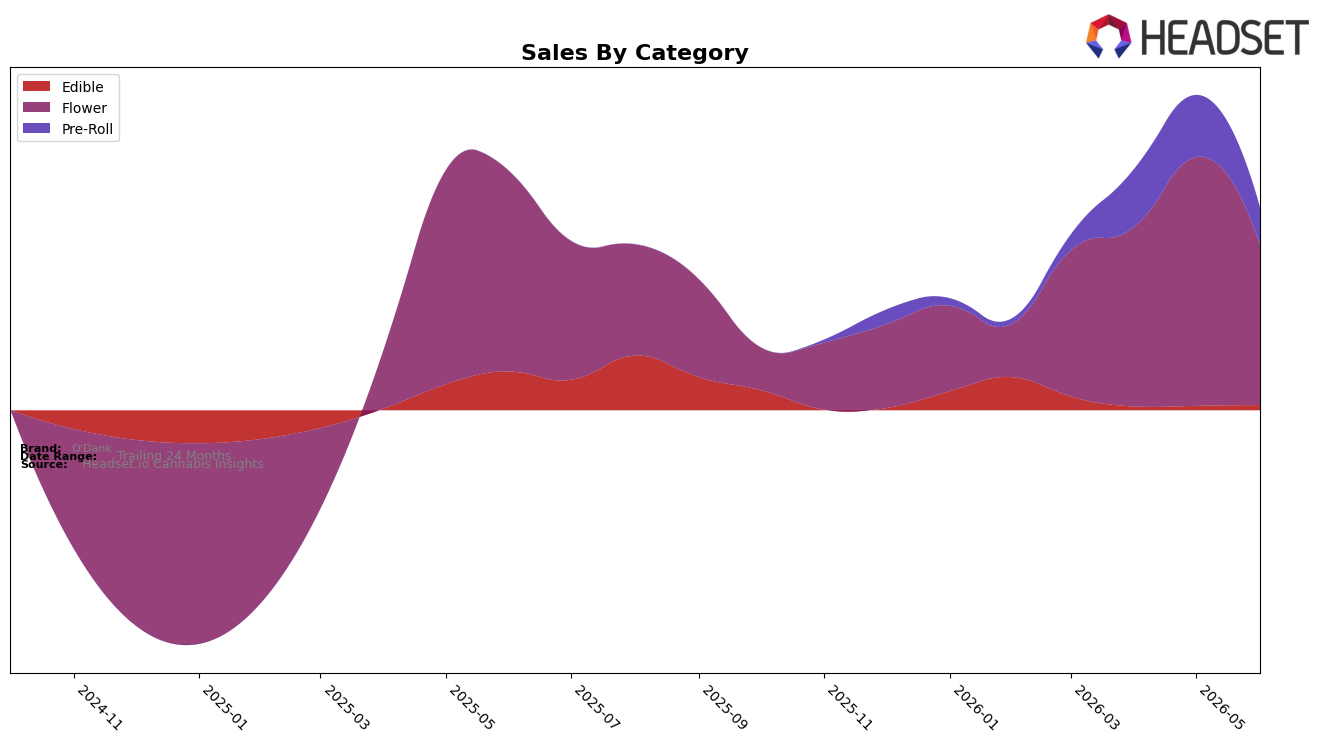

O'Dank concentrated 79.07% of sales in Flower in June 2026, with Flower down 19.84% year over year and 35.56% month over month, while Pre-Roll held 18.49% share with a 39.61% month-over-month drop and Edible maintained 2.44% share with an 87.17% year-over-year decline but an 18.07% month-over-month gain. The average price fell 41.29% year over year to $20.89, yet Flower’s category-level average price sat at $35.12, indicating mix and pricing are moving in opposite directions; combined with a 15.02% brand sales decline year over year and a Flower rank of 39 in Ohio, the pattern implies a heavy reliance on a contracting anchor category and a price architecture that risks eroding perceived value even as volume chases lower tickets.

With Flower still commanding 79.07% share but falling faster month over month than the brand overall (-35.56% vs. -39.61% in Pre-Roll and +18.07% in Edible), the brand’s positioning is skewed toward a price-sensitive Flower play that sacrifices margin headroom; the 41.29% year-over-year average price compression alongside a 19.84% Flower decline suggests discount-driven share defense that isn’t translating to rank lift, as evidenced by the 39th position in Flower in Ohio. The Edible uptick of 18.07% month over month from a 2.44% base and an 87.17% year-over-year hole implies limited diversification power today, so defending Flower while selectively scaling Edible where elasticity is favorable becomes the practical path to reduce exposure to single-category volatility.

Competitive Landscape

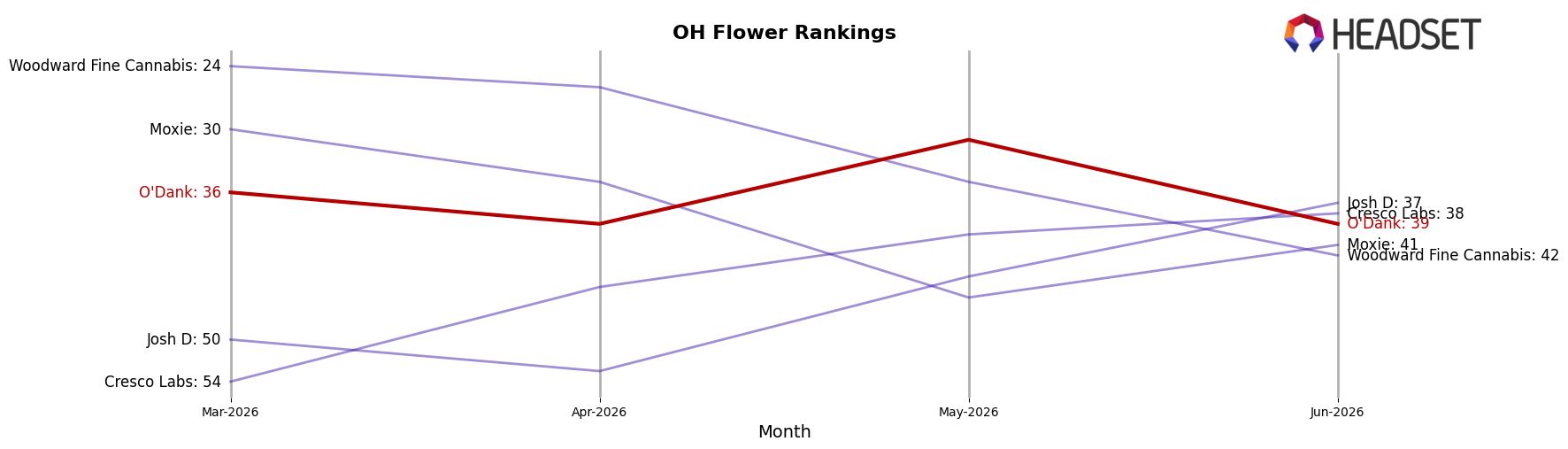

O'Dank sits at rank #39 in OH Flower for June 2026, down 5 positions year over year from #34 and slipping 3 spots since March 2026 from #36, after peaking at #31 in May 2026; by contrast, Klutch Cannabis climbed from #20 to #1 with 304.8% YoY sales growth while Riviera Creek moved from #1 to #2 alongside a 22.7% YoY sales decline, indicating O'Dank’s mid-pack drift is driven less by absolute contraction and more by faster-moving leaders reshuffling the top 10, a trajectory that implies share erosion unless rank recovers toward its May 2026 peak.

Notable Products

Lemon Cherry Sorbet Pre-Roll 2-Pack (1g) posted the steepest movement in June 2026 with a -51.7% month-over-month drop to rank 4, while H.F.C.S. (3.5g) fell -39.0% to rank 8. Sticky Pie (3.5g) declined -46.7% at rank 9, and Lemon OG Pre-Roll 2-Pack (1g) was the lone riser at +9.9% sitting at rank 5. Four of the top ten are Flower SKUs, but the two largest declines sit within Flower ranks 8 and 9, implying product mix risk is accumulating in mid-tier Flower even as Pre-Roll holds share through stable positions at ranks 1 and 2.

Despite LCS Pre-Roll 2-Pack (1g) holding rank 1 and LOG Pre-Roll 2-Pack (1g) at rank 2, the category split shows pressure where Pre-Roll strength is concentrated at the top while mid-pack Flower weakens by -39.0% and -46.7%. Frosted Cookies (14.15g) at rank 3 anchors premium Flower with $83,422, yet D Coast (3.5g) at rank 4 and Lemon OG (3.5g) at rank 6 lack month-over-month momentum signals. The pattern implies O'Dank is leaning on a narrow Pre-Roll leadership while Flower volatility may require SKU pruning or pricing calibration to prevent share erosion below the top tier.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.