Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Redemption is stocked at 384 licensed dispensaries across Michigan, Pennsylvania, and 4 other states, 192 of them in Michigan, with the deepest coverage in New Buffalo, Grand Rapids, Lansing, Detroit, and Adrian. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

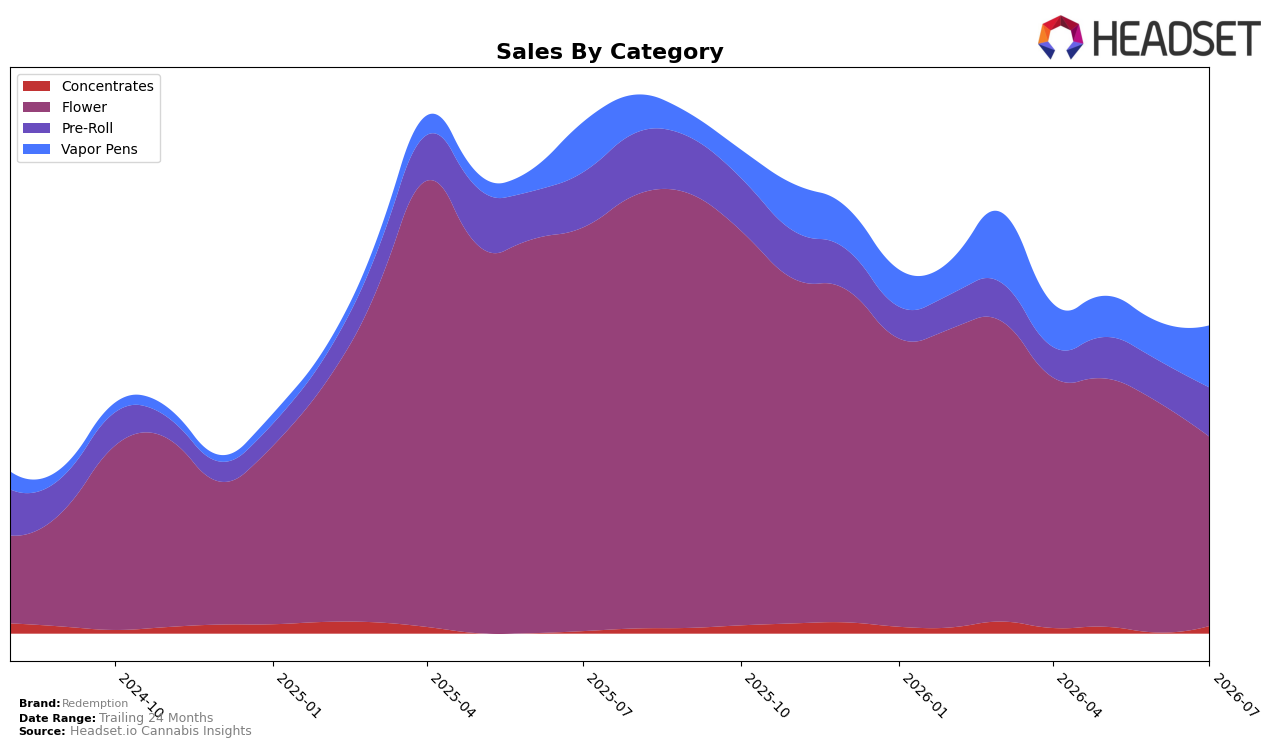

In July 2026, Redemption’s category mix tilted away from Flower as Flower’s share sat at 55.43% with sales down 51.21% year over year and 16.75% month over month, while Vapor Pens rose to 20.95% share with sales up 18.27% year over year and 43.81% month over month. Pre-Roll held 17.45% share with sales down 8.49% year over year but up 12.67% month over month, and Concentrates reached 6.17% share with sales up 28.98% year over year and 40.06% month over month. Despite an overall brand sales decline of 35.56% year over year alongside a modest 1.89% increase in average price, the mix shift toward Vapor Pens and Concentrates indicates volume is consolidating in format types with faster recent momentum.

The pivot away from Flower’s double-digit month-over-month contraction of 16.75% and steep 51.21% year-over-year decline, toward categories growing 40.06% month over month in Concentrates and 43.81% month over month in Vapor Pens, implies Redemption is repositioning toward inhalable formats where price points (average price $14.43 in Vapor Pens vs. $26.54 in Flower) support quicker trial and basket flexibility. With Pre-Roll’s 12.67% month-over-month lift but 8.49% year-over-year dip, the brand’s near-term upside likely comes from sustaining the two fastest-moving segments while treating Flower as a defensive anchor; the pattern suggests reallocating merchandising and promotional focus to Vapor Pens and Concentrates can counterbalance Flower contraction and stabilize share.

Competitive Landscape

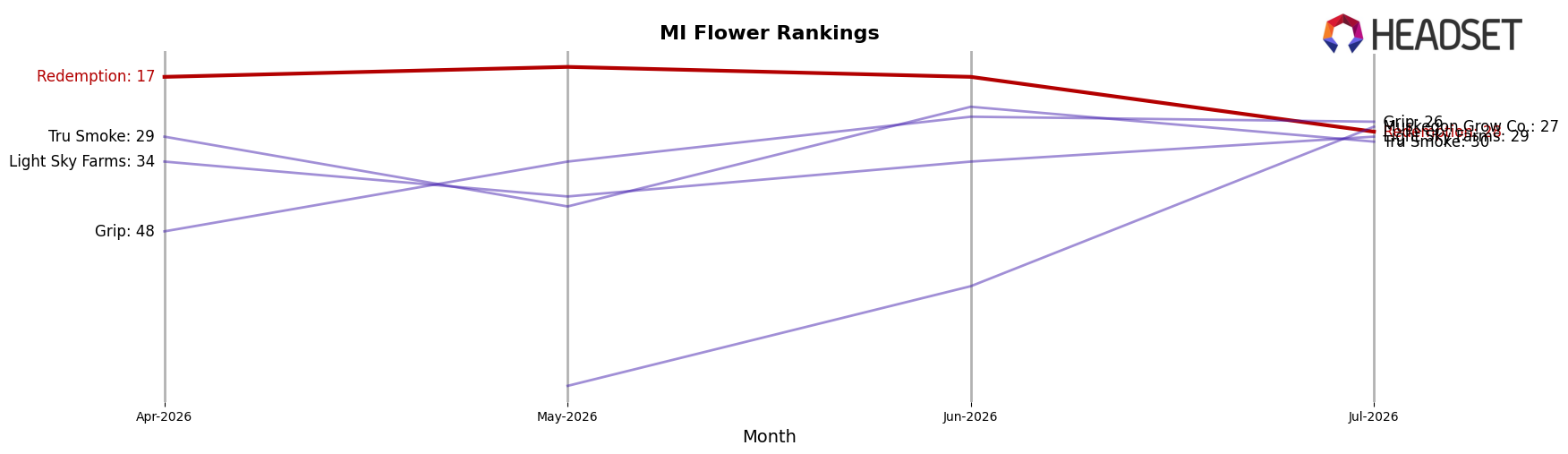

Redemption sits at rank #28 in MI Flower for July 2026, down 21 positions year over year from #7, and 11 spots below its April 2026 standing at #17; the brand is also 24 ranks off its historical peak of #4 from April 2025. In contrast, High Minded holds #1 despite a 12.46% year-over-year sales decline, while Goodlyfe Farms advanced to #3 with 36.83% year-over-year growth; Mischief moved to #4 with 59.39% year-over-year growth, tightening pressure at the top. The spread between Redemption’s current #28 and competitors at #1–#4, combined with a 21-rank YoY slide and an 11-rank drop since April 2026, implies the brand’s trajectory is downward and that recapturing share will require reversing multi-quarter rank erosion rather than expecting near-term reversion to its April 2025 peak.

Notable Products

Sweet N' Gassy (3.5g) posted the steepest movement in July 2026 with a -34.2% month-over-month decline while slipping to rank 6, contrasting with Lemon Cherry Diesel (3.5g) up +34.9% at rank 1. Stanky Leg (3.5g) also rose +36.7% at rank 5, and together these shifts put three Flower SKUs inside the top six while Pre-Rolls occupy ranks 4, 8, and 10. With Flower accounting for seven of the top ten ranks and the lead SKU generating $233,791, the mix implies a tilt toward high-velocity 3.5g strains where volatility can be used to trade up share in laddered price tiers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.