Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

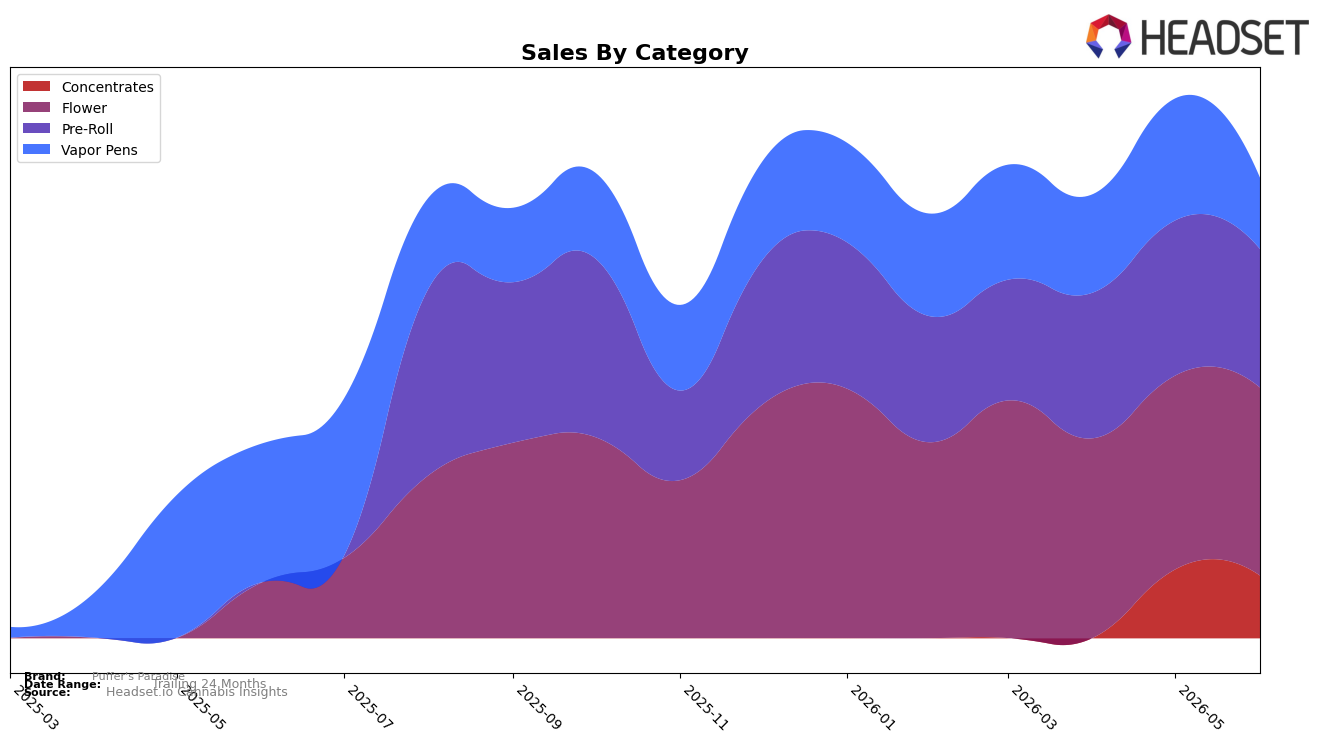

In June 2026, Puffer's Paradise concentrated 40.85% of sales in Flower with 239.31% year-over-year growth but a 3.00% month-over-month decline, while Pre-Roll held 30.08% share with a 10.74% month-over-month drop and no year-over-year read, indicating a recent pullback in a large base. Vapor Pens accounted for 15.45% share with a 48.69% year-over-year contraction and a 41.65% month-over-month fall, as Concentrates captured 13.62% share with an 8.93% month-over-month decline and no year-over-year benchmark. With total brand sales up 137.19% year over year and average price down 47.71%, the mix shift toward Flower at higher average price of $34.74 and away from Vapor Pens at 34.37 suggests growth is leaning on a premiumized Flower engine even as short-term category headwinds trim momentum.

These shifts imply Puffer's Paradise is pivoting its competitive posture toward Flower-led differentiation while absorbing volatility in Vapor Pens, with a 239.31% Flower year-over-year surge offsetting a 48.69% decline in Vapor Pens and a 10.74% month-over-month step-down in Pre-Roll. The June 2026 rank of 56 in Alberta Pre-Roll, alongside a 30.08% share of brand sales in that category and a 3.00% Flower month-over-month ebb, implies the path to broader defensibility runs through sustaining Flower gains while stabilizing Pre-Roll positioning in Alberta, using the lower average price strategy to maintain accessibility even as the mix tilts toward higher-priced formats.

Competitive Landscape

Puffer's Paradise sits at rank #56 in AB Pre-Roll for June 2026, improving 3 positions from #59 in March 2026 but still 6 spots below its peak of #50 from October 2025; this combination of a 3-rank quarter-on-quarter lift and a 6-rank gap to peak indicates incremental recovery without full reversion. In contrast, General Admission holds #1 with a 1-position year-over-year improvement despite a 21.97% sales decline, while Back Forty / Back 40 Cannabis is #2 after a 6-rank year-over-year climb alongside 64.01% sales growth, suggesting top-tier reshuffling that Puffer's Paradise has not matched. The pattern implies Puffer's Paradise is stabilizing below the leadership pack, with modest rank momentum insufficient to bridge the mid-table gap unless quarter-on-quarter gains compound faster than competitor rank ascents.

Notable Products

Dragon's Breath Live Rosin (1g) posted the steepest decline at -45.8% month over month to rank 8, while Magik Dragon Pre-Roll 3-Pack (1.5g) slid -13.7% yet held rank 1, indicating volatility at the bottom alongside stickiness at the top. Across the top ten, four SKUs are Pre-Roll products occupying ranks 1, 2, 4, and 9, with movements spanning +16.3% for Honah Lee Haze Pre-Roll 3-Pack (1.5g) at rank 6 to -29.6% for Heavenly Haze Infused Pre-Roll 3-Pack (1.5g) at rank 9, which implies the format is saturated and price- or promo-sensitive. On Flower, Magik Dragon (7g) rose +11.3% at rank 5 as Honah Lee Haze (7g) fell -10.5% at rank 3, suggesting share is rotating within the portfolio rather than expanding category reach. The mix points to a pivot opportunity: stabilize Pre-Roll price architecture while leaning into Magik Dragon (7g) momentum to offset concentrate volatility and rebalance reliance on a single top Pre-Roll.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.