Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Resinate is stocked at 106 licensed dispensaries across Massachusetts, with the deepest coverage in Brockton, Easthampton, Great Barrington, Springfield, and Boston. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

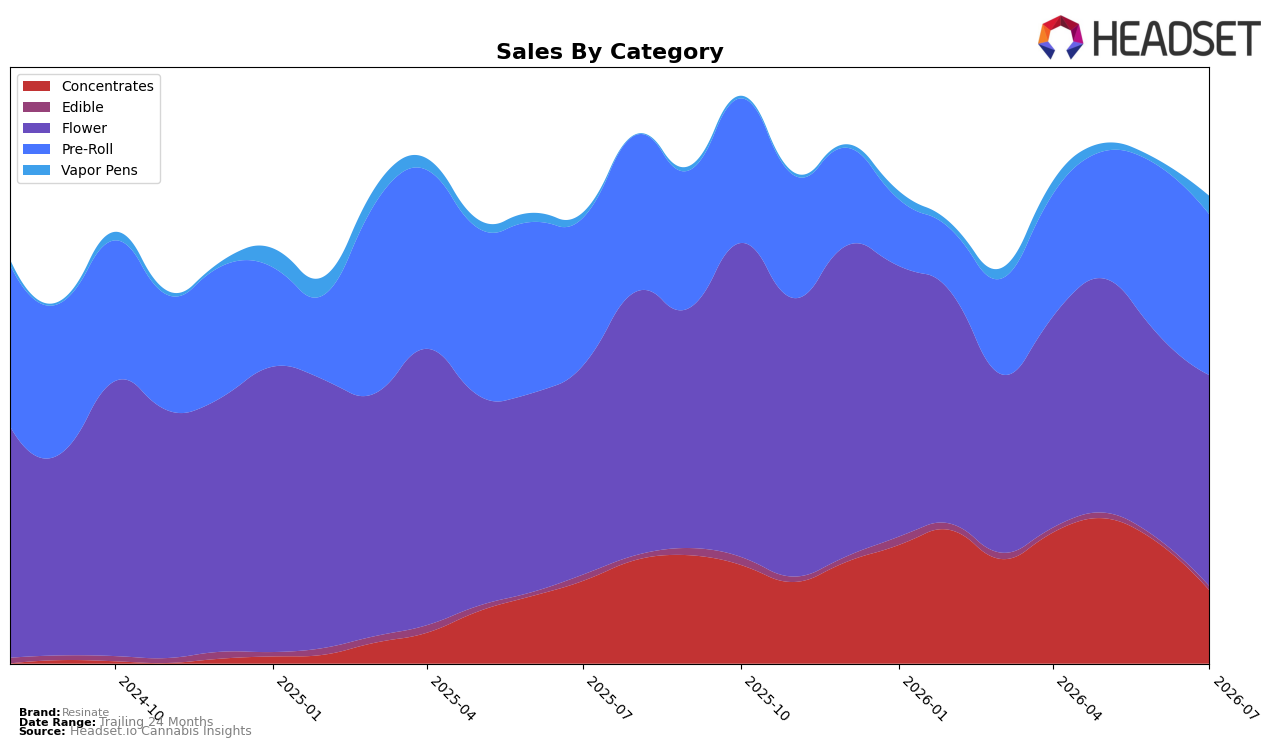

In July 2026, Resinate’s mix tilted toward Flower at 44.83% share with 0.87% year-over-year growth and 3.19% month-over-month, while Pre-Roll held 34.20% share with 8.73% YoY but fell 4.77% MoM; together these two categories accounted for 79.03% of sales, indicating concentration in inhalables. Concentrates dropped 11.42% YoY and 39.03% MoM to 15.72% share, as Vapor Pens surged 200.60% YoY and 185.96% MoM to 4.13% share, signaling rapid re-entry from a small base; Edible remained niche at 1.12% share with -28.32% YoY and +4.32% MoM. The brand’s average price declined 14.79% YoY alongside modest total sales growth of 3.55% YoY, and rank in Flower was 45 in Massachusetts, which implies volume-driven recovery in inhalables offsetting margin pressure and a deliberate pivot away from Concentrates.

The shift shows Resinate leaning into accessible inhalables: Vapor Pens’ triple-digit growth paired with a 14.79% YoY average price reduction points to price-enabled trial that complements Flower’s 3.19% MoM lift and Pre-Roll’s 8.73% YoY expansion. With Concentrates contracting 39.03% MoM and 11.42% YoY while Vapor Pens scaled from a low base to 4.13% share, the portfolio appears to be reallocating demand toward lower-friction formats, which can raise household penetration but may cap near-term price realization. Given the Flower rank of 45 in Massachusetts and a combined 79.03% share in Flower and Pre-Roll, sustaining growth likely depends on defending Flower velocity while using Vapor Pens’ 185.96% MoM momentum to diversify away from the 15.72% Concentrates exposure.

Competitive Landscape

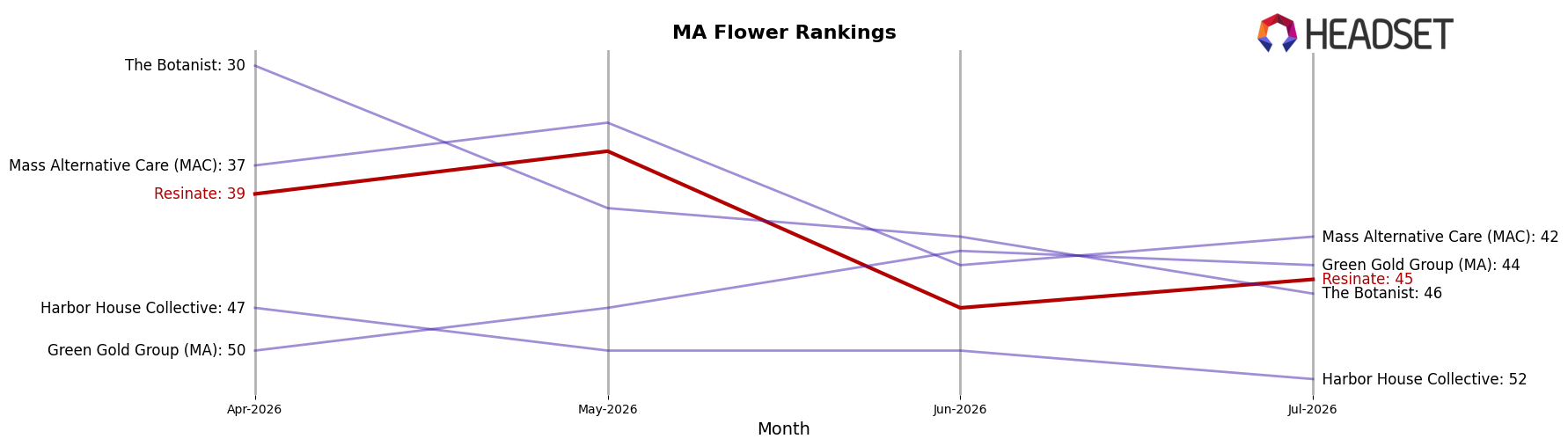

Resinate sits at rank #45 in Massachusetts Flower in July 2026, down 6 positions year over year from #39, and also 6 positions below its April 2026 three-month reference point at #39; against that slippage, the brand is 20 ranks below its December 2025 peak at #25, signaling a multi-quarter retreat rather than a one-month wobble. Meanwhile, Farmer's Cut climbed from #4 to #1 with a 56.7% year-over-year sales increase, and Root & Bloom advanced from #10 to #5 alongside 118.9% sales growth, indicating that leaderboard mobility is flowing upward for competitors while Resinate is drifting downward; the pattern implies Resinate’s rank trajectory is losing share of attention to faster-advancing peers and will require either mix shifts or pricing actions to stabilize ranks before further erosion from #45.

Notable Products

Strawberry Banana Lemon Pre-Roll (1g) posted the steepest decline in July 2026 at -29.8% MoM while sliding to rank 6, and Socrates Sour Pre-Roll (1g) also fell -14.5% to rank 3, indicating demand is tilting away from mid-pack pre-rolls even as the category still holds seven of the top ten slots. Socrates Sour (3.5g) surged +44.9% MoM to rank 4 while Blue Dream (3.5g) dropped -14.2% to rank 8, a split that points to selective Flower momentum concentrated in a single SKU rather than a category-wide lift. Blue Dream Pre-Roll (1g) retained rank 1 with a +6.4% MoM gain and an estimated $54,725 in July 2026 sales, but the second-ranked Gelato Pre-Roll (1g) lacks a comparable growth signal, implying leadership is narrow at the top. Together these movements imply Resinate’s mix is consolidating around a few winners in Pre-Rolls and a standout in Flower, signaling a need to reinforce hero SKUs while pruning underperforming variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.