Market Insights Snapshot

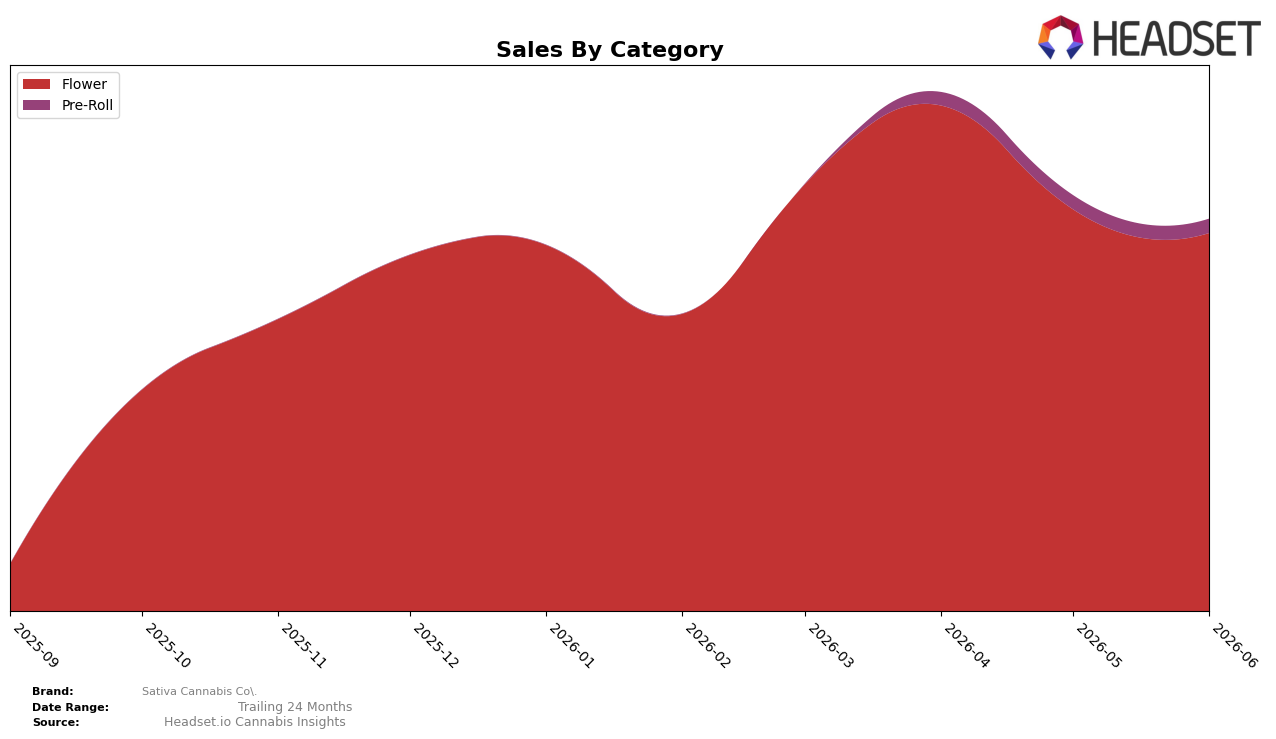

In June 2026, Sativa Cannabis Co.’s mix is overwhelmingly concentrated in Flower at 96.44% share while Pre-Roll holds 3.56% share, a split that tilts further toward single-SKU purchasing as Flower average price sits at $50.55 versus Pre-Roll at $8.77. Month over month, Flower contracted by 5.87% while Pre-Roll expanded by 1.15%, and in the Flower category the brand sits at rank 28 in Arizona. The pattern implies a narrowing reliance on Flower that is under short-term pressure, with a small but incrementally growing Pre-Roll presence offering limited diversification.

The combination of a 5.87% month-over-month decline in the 96.44% Flower base and a 1.15% month-over-month uptick in the 3.56% Pre-Roll slice suggests mix risk if category headwinds persist, because the falling contribution comes from the dominant line while the stabilizer is too small to offset volatility. Given the rank position of 28 in Arizona Flower and the large price gap between $50.55 Flower and $8.77 Pre-Roll, the current trajectory implies Sativa Cannabis Co. is positioned as a Flower-first brand that may need either share capture within Flower or deliberate Pre-Roll scaling to prevent further dilution of overall momentum.

Competitive Landscape

Sativa Cannabis Co. sits at rank #28 in AZ Flower in June 2026, a climb of 1 position from March 2026 (#29) and matching its peak rank of #28 in June 2026, while year-over-year rank is unavailable and therefore offers no direct comparison. Against the top tier, Just Flower holds #1 with a +1 YoY rank and +13.0% sales growth, and The Pharm moved from #5 to #4 with +44.1% sales growth, indicating that Sativa Cannabis Co.’s +1 rank shift over three months trails competitors’ upward momentum at the category’s summit. With Mohave Cannabis Co. at #3 despite a -13.9% sales change and Brown Bag rising to #5 alongside +72.8% sales growth, the pattern suggests that Sativa Cannabis Co.’s current foothold at #28 requires either rapid share capture or targeted differentiation to avoid being boxed out by faster-moving brands.

Notable Products

Premium Diesel (3.5g) posted the steepest decline at -66.4% month over month and slid to rank 5, signaling a sharp pullback in a core Flower SKU. Sour Haze (3.5g) counter-moved with a +76.6% surge to rank 3, while Raspberry Haze Pre-Roll (1g) climbed to rank 1 with +114.4% MoM and $9,728 in June 2026 sales. Four of the top ten are 14g Popcorn Flower SKUs sitting between ranks 6 and 9 despite MoM changes ranging from +1.8% to -1.3%, indicating stability in value-pack formats even as 3.5g performance bifurcates. Taken together, Sativa Cannabis Co.'s mix points to a pivot toward higher-velocity haze-led units and steady 14g value formats while legacy Diesel in 3.5g cedes share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.