Market Insights Snapshot

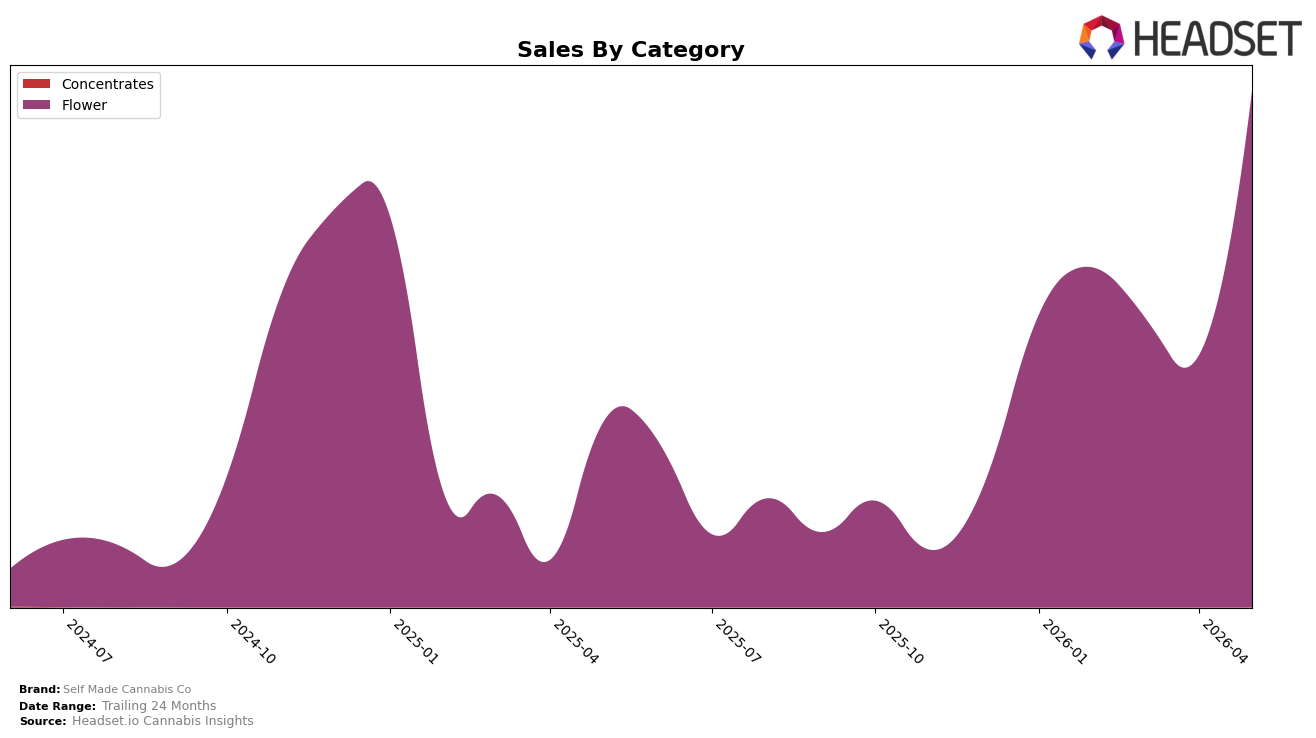

In May 2026, Self Made Cannabis Co operated as a single-category brand with Flower accounting for 100.0% of sales, rising 178.98% year over year and 105.48% month over month, while the average item price increased 4.03% YoY to $25.92. Within Oregon Flower, the brand stood at rank 24, indicating mid-pack placement despite triple-digit growth rates in both YoY and MoM terms; this concentration in one category suggests a volume-led surge within Flower rather than diversification across formats.

The combination of a 100.0% Flower mix and a 4.03% YoY price lift alongside 105.48% MoM sales growth points to demand elasticity favoring volume at a slightly higher price point, implying headroom to trade up without immediate share loss. Holding rank 24 in Oregon Flower while posting 178.98% YoY expansion indicates that growth is more about catching up in a broad category tide than about premium-tier displacement, meaning the brand’s near-term positioning is as a scale-oriented Flower player with pricing power constrained to incremental moves.

Competitive Landscape

Self Made Cannabis Co is ranked #24 in OR Flower in May 2026, improving 53 positions from #77 year over year, and climbing 11 spots from #35 three months ago; this new peak rank of #24 in May 2026 contrasts with PRUF Cultivar / PRŪF Cultivar holding steady at #1 year over year while posting a 23.9% YoY sales gain, and Grown Rogue moving up from #7 to #2 alongside a 51.1% YoY sales increase. Against this top-tier movement, Bald Peak slid from #2 to #3 with a 12.6% YoY sales decline, and Otis Garden advanced from #20 to #5 with 101.4% YoY sales growth, indicating Self Made Cannabis Co’s rise from #77 to #24 is outpacing some incumbents on rank momentum but still trails the velocity of leading climbers; the trajectory implies the brand is transitioning from lower-tier presence toward mid-shelf relevance, with continued share capture likely if the recent 11-rank lift over three months persists.

Notable Products

Cherry Dosi (28g) posted the standout movement in May 2026 with a 103% month-over-month increase, climbing into rank 7, while Ultra Sour (3.5g) rose 33.9% yet remained lower at rank 4; this split suggests momentum is coming from larger-format genetics rather than small-pack entries. Tiramisu (28g) held rank 2 with an estimated $54,031 in sales as Blue Zushi (28g) in rank 5 advanced only 7.0%, and Cindy 99 (28g) at rank 10 moved 6.4%, pointing to slower velocity at the bottom of the top 10 despite one outlier surge. With eight of the top ten anchored in 28g Flower, the concentration in large formats signals a pivot toward value-driven ounces where a single breakout like Cherry Dosi can quickly reconfigure the middle ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.