Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

SugarTop Buddery is stocked at 83 licensed dispensaries across Oregon, with the deepest coverage in Eugene, Bend, Portland, Springfield, and Ashland. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

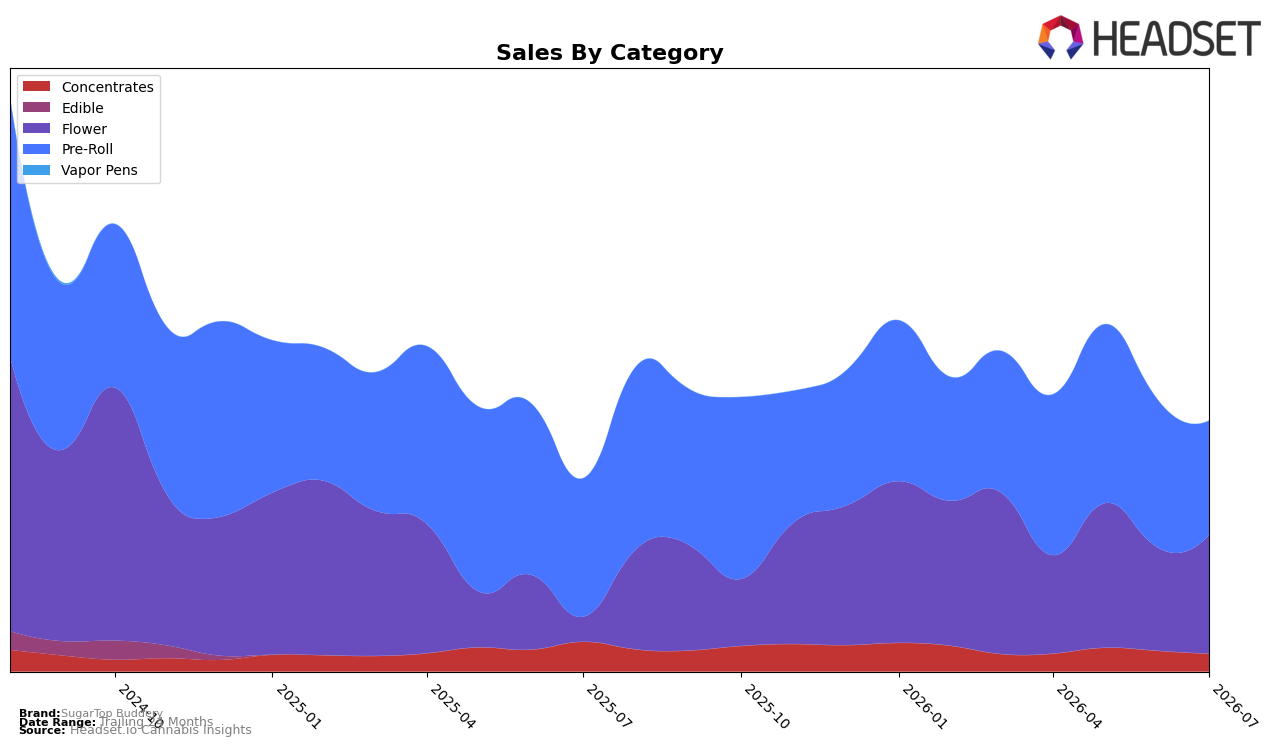

SugarTop Buddery shifted decisively toward Flower in July 2026, with Flower rising to a 47.33% mix share alongside a 379.64% year-over-year sales gain and a 14.88% month-over-month lift, while Pre-Roll contracted to 45.65% share with a -17.44% YoY and -22.70% MoM decline. Concentrates compressed further to 7.02% share with -40.31% YoY and -14.06% MoM, and the brand’s average price fell -12.50% YoY even as total brand sales increased 29.99% YoY, indicating volume-led growth concentrated in categories with lower price points than Flower’s $29.48 average. The pattern implies SugarTop Buddery is reallocating demand toward higher-value Flower while allowing Pre-Roll and Concentrates to shrink, using price elasticity to convert traffic into volume without sacrificing the mix pivot.

With Flower now the plurality at 47.33% and Pre-Roll sliding 22.70% MoM, SugarTop Buddery’s category posture favors premium-perceived formats despite a -12.50% YoY price cut at the brand level, positioning the brand to climb from its Flower rank of 71 in Oregon if the 14.88% MoM Flower momentum persists. The simultaneous 379.64% YoY Flower surge and -40.31% YoY Concentrates drop concentrate revenue risk into a single growth pillar, which implies near-term share wins will depend on sustaining Flower replenishment and guarding against cannibalization from discounted Pre-Rolls that still hold 45.65% share.

Competitive Landscape

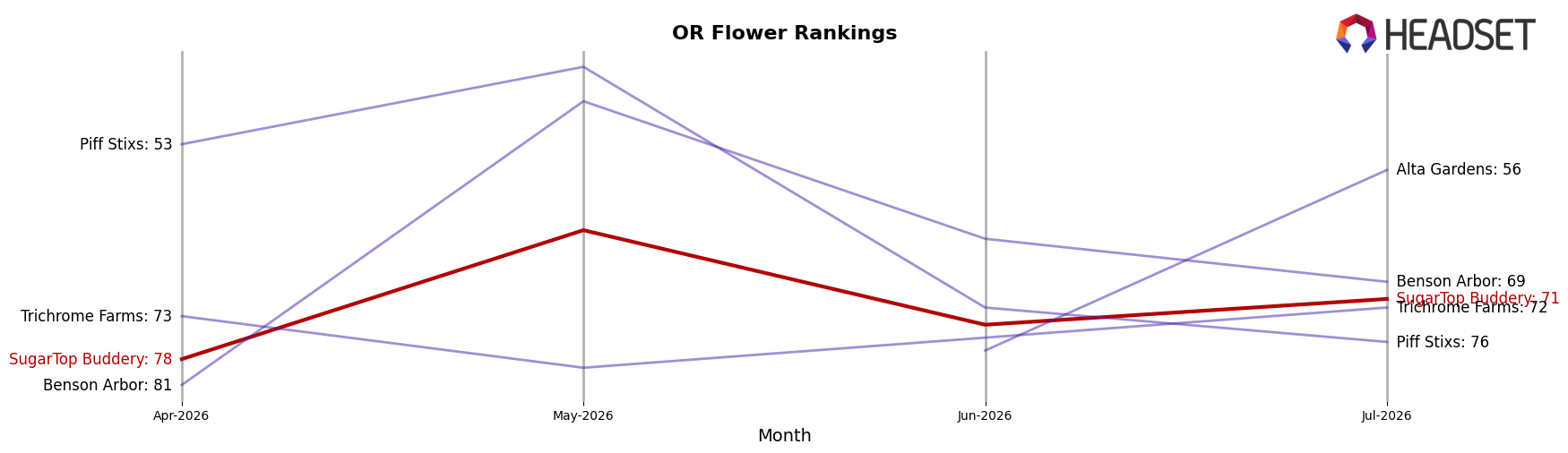

SugarTop Buddery sits at rank #71 in OR Flower for July 2026 after improving 119 positions from #190 year over year, and it has edged up 7 spots from #78 in April 2026 while still far from its peak at #14 in July 2024; meanwhile, PRUF Cultivar / PRŪF Cultivar held at #1 year over year and Grown Rogue advanced from #3 to #2 as Otis Garden climbed from #12 to #4, indicating SugarTop Buddery’s upward movement is happening in a tier where top spots are consolidating among faster risers with 53%–86% sales growth. The pattern implies SugarTop Buddery’s rebound is real but capped unless it accelerates beyond single-digit rank gains amid competitors posting double-digit rank and sales momentum.

Notable Products

Mondo Bat - Purple Water Ice Pre-Roll (1g) posted the steepest decline in July 2026 at -14.8% and slipped to rank 2, while Stubby Bat - Acapulco Gold Pre-Roll (0.5g) rose 26.0% to rank 1, signaling a swap in flagship momentum. Mondo Bat - Pure Michigan Pre-Roll (1g) advanced 38.3% to rank 4, and eight of the top ten are Pre-Roll SKUs, concentrating share at the expense of Flower despite Cake Bomb (1g) holding rank 8 with $19,854 in sales. The pattern implies SugarTop Buddery is consolidating consumer demand around single-gram and half-gram Pre-Rolls, nudging mix away from Flower and forcing portfolio decisions around underperforming flavor lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.