May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In May 2026, Suncrafted concentrated its mix into Concentrates at 48.50% share with year-over-year growth of 75.35% and month-over-month acceleration of 154.33%, while Flower held 40.95% share with a -30.44% year-over-year decline but a 67.36% month-over-month lift. Vapor Pens expanded to 8.18% share on 59.24% year-over-year growth and 334.96% month-over-month growth, whereas Pre-Roll fell to 1.93% share with -90.47% year-over-year and -58.35% month-over-month. Edible remained marginal at 0.44% share despite a 57.87% month-over-month increase and a -63.95% year-over-year drop. With brand sales down 11.61% year-over-year but up 60.34% over 24 months and average price up 59.28% year-over-year to $27.25, the pattern implies Suncrafted is pivoting toward higher-priced Concentrates and recovering volume in Vapor Pens to offset prolonged Flower and Pre-Roll erosion.

The mix shift pushes Suncrafted toward a potency- and format-led positioning centered on Concentrates, evidenced by a 26th rank in Concentrates in Massachusetts alongside a 154.33% month-over-month surge and 75.35% year-over-year growth, while Vapor Pens’ 334.96% month-over-month spike suggests a secondary inhalables lane that can scale faster than Flower. The concurrent -30.44% year-over-year decline in Flower and -90.47% year-over-year in Pre-Roll concentrate demand into fewer, higher-value units, aligning with a 59.28% year-over-year rise in average price and a 48.50% category share concentration. This structure implies near-term share gains are likelier through continued Concentrates depth and selective Vapor Pen expansion rather than broad SKU revival in Flower or Pre-Roll.

Competitive Landscape

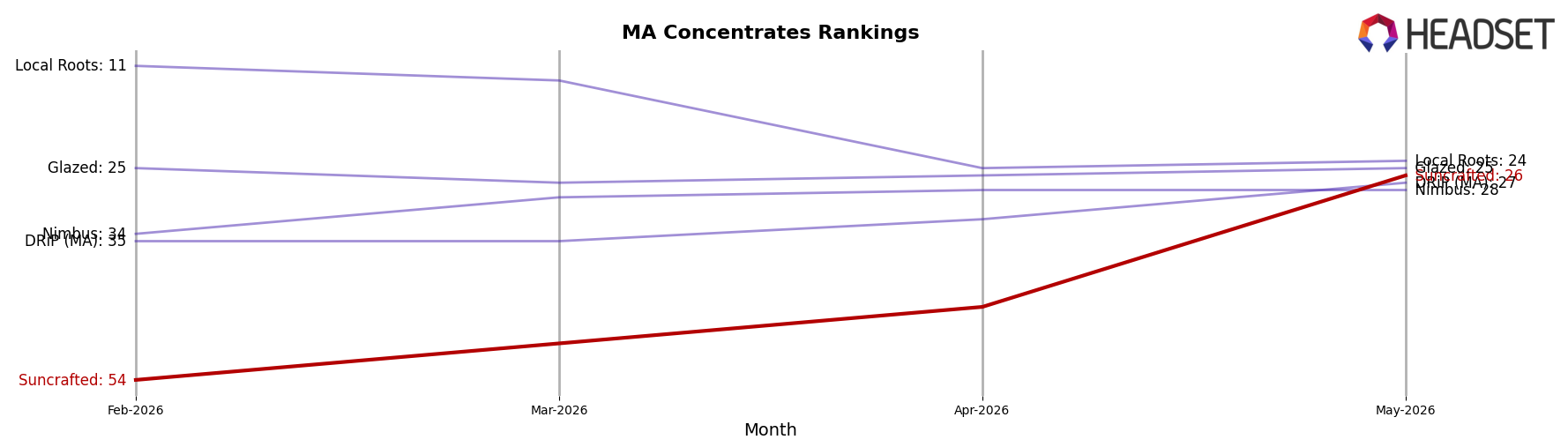

Suncrafted sits at rank #26 in MA Concentrates in May 2026, improving 14 positions from #40 year over year, and rising 28 ranks from #54 three months ago to match its peak at #26 in May 2026; meanwhile, top competitor Good Chemistry Nurseries held #1 year over year and in May 2026 while Harbor House Collective advanced from #17 to #5 alongside a 189.2% YoY sales change, indicating Suncrafted’s rank gains are occurring amid faster upward mobility among leaders. With Crispy Commission Concentrates steady at #2 despite a -14.9% YoY sales change and Nature's Heritage anchored at #3 with +20.1% YoY sales, Suncrafted’s climb of 14 ranks YoY and 28 ranks since February 2026 implies momentum from a lower base that still requires further share capture to penetrate the top 20.

Notable Products

Fruity Gum (3.5g) posted the standout move in May 2026 with a +717% month-over-month surge to the rank 2 position, while Superboof (3.5g) climbed +162% MoM to rank 1, indicating Flower is driving the leaderboard. Bananaconda Cold Cure Live Rosin (1g) also accelerated +115% MoM at rank 7, yet Concentrates occupy ranks 4, 6, 7, and 8 as a block, whereas Flower holds ranks 1, 2, 3, and 5, concentrating eight of the top ten in just two categories. With two Flower SKUs occupying the top two ranks and at least four Concentrates in the top ten, the mix tilts toward high-velocity Flower supported by premium-priced rosin for basket trade-up, implying Suncrafted is prioritizing breadth in Flower while using Live Rosin to anchor higher-ticket trips around $9,514.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.