Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Heirloom Collective is stocked at 71 licensed dispensaries across Massachusetts, with the deepest coverage in Fall River, Allston, Lowell, Quincy, and Springfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

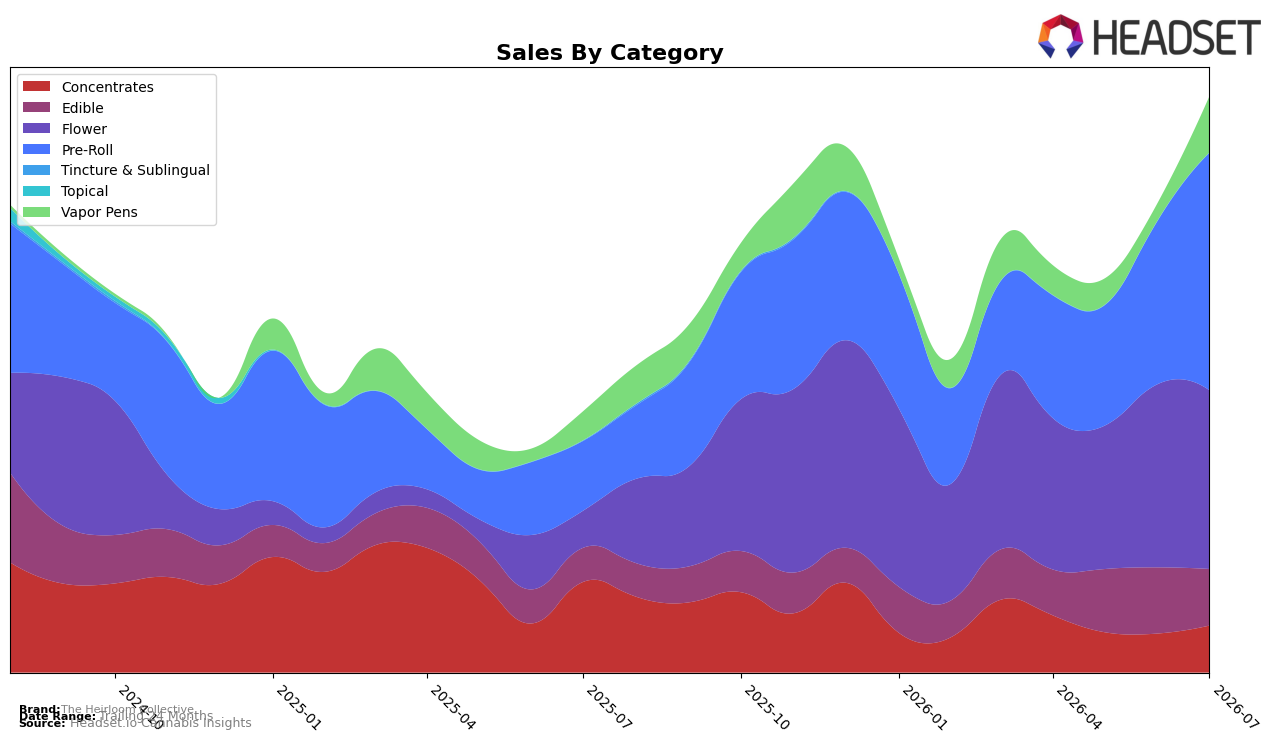

In July 2026, The Heirloom Collective’s mix pivoted toward Pre-Roll at 41.27% share with 241.07% year-over-year growth and 45.04% month-over-month growth, while Flower held 31.04% share with 383.91% YoY and a -2.56% MoM dip. Vapor Pens expanded to 9.74% share with 94.67% YoY and a 224.12% MoM surge, contrasting with Edible at 9.81% share and -14.49% MoM despite 66.30% YoY, and Concentrates at 8.15% share with -48.23% YoY but 20.41% MoM. With overall brand sales up 121.26% YoY and average price down 30.10% YoY, the pattern implies unit-led expansion driven by lower ticket sizes, with momentum concentrated in Pre-Roll and a rapid monthly rebound in Vapor Pens while Flower stabilizes as a high-growth but flattening monthly anchor.

Positioning in Massachusetts centers on value-forward formats: Pre-Roll scale plus a 30.10% YoY price decrease signals price elasticity capture, while the 224.12% MoM lift in Vapor Pens indicates tactical promotional or SKU refresh effects that can diversify reliance on the 41.27% Pre-Roll share. Given a Pre-Roll category rank of 32 and Flower’s 383.91% YoY growth paired with a -2.56% MoM contraction, the implication is a two-pronged strategy—defend mid-pack rank through consistent Pre-Roll availability and price architecture, and convert the Flower growth into sustainable share without cannibalizing pen gains—so the brand can trade shoppers across formats rather than over-indexing on a single entry point.

Competitive Landscape

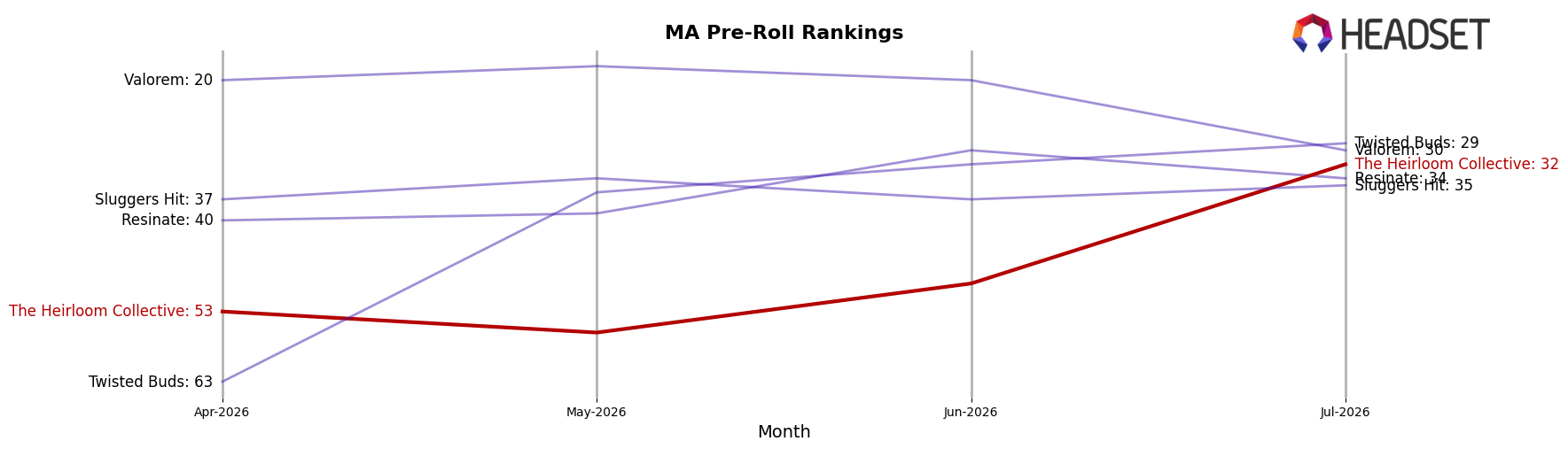

The Heirloom Collective sits at rank #32 in MA Pre-Roll in July 2026, improving 55 positions from #87 year over year, and gaining 21 slots from #53 in April 2026; this climb coincides with hitting a peak rank of #32 in July 2026 while the category leader Jeeter held #1 both year over year and in July 2026 with a 44% YoY sales increase, and Cali-Blaze moved from #16 to #2 alongside a 241% YoY sales rise, indicating that The Heirloom Collective’s acceleration is closing relative rank distance even as top competitors expand faster in absolute sales. The juxtaposition of a 55-rank YoY jump for The Heirloom Collective against Nature's Heritage advancing from #4 to #3 with a 42% YoY sales gain and Northern Grown rising from #10 to #4 with a 100% YoY lift implies that recent rank momentum is timing-driven and defensible only if conversion gains outpace the mid-tier cohort’s high-percentage growth.

Notable Products

Orange Crush Pre-Roll (0.75g) posted the headline move in July 2026 with a 111.6% month-over-month surge and climbed to rank 4, while Classic Cubes 20-Pack (100mg) fell 20.6% MoM and slid to rank 10; together these shifts indicate volatility concentrated at the edges of the top 10. Kitchen Sink Pre-Roll (1g) stayed at rank 1 with a 38.0% MoM increase and generated $66,934, and Peanut Butter Lady Pre-Roll (1g) rose 39.7% MoM to hold rank 3, pointing to consistent demand at the top. With eight of the top ten as Pre-Roll SKUs and Grape Pie Bx1 Pre-Roll (1g) down 5.4% at rank 9, the category shows breadth but uneven momentum across formats. The product mix implies The Heirloom Collective is concentrating on Pre-Rolls to drive share, using a few fast-advancing SKUs to offset softness in non-Pre-Roll offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.