Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Cloud Cover (C3) is stocked at 148 licensed dispensaries across Missouri, Massachusetts, and Michigan, 102 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Kansas City, St Peters, and Columbia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

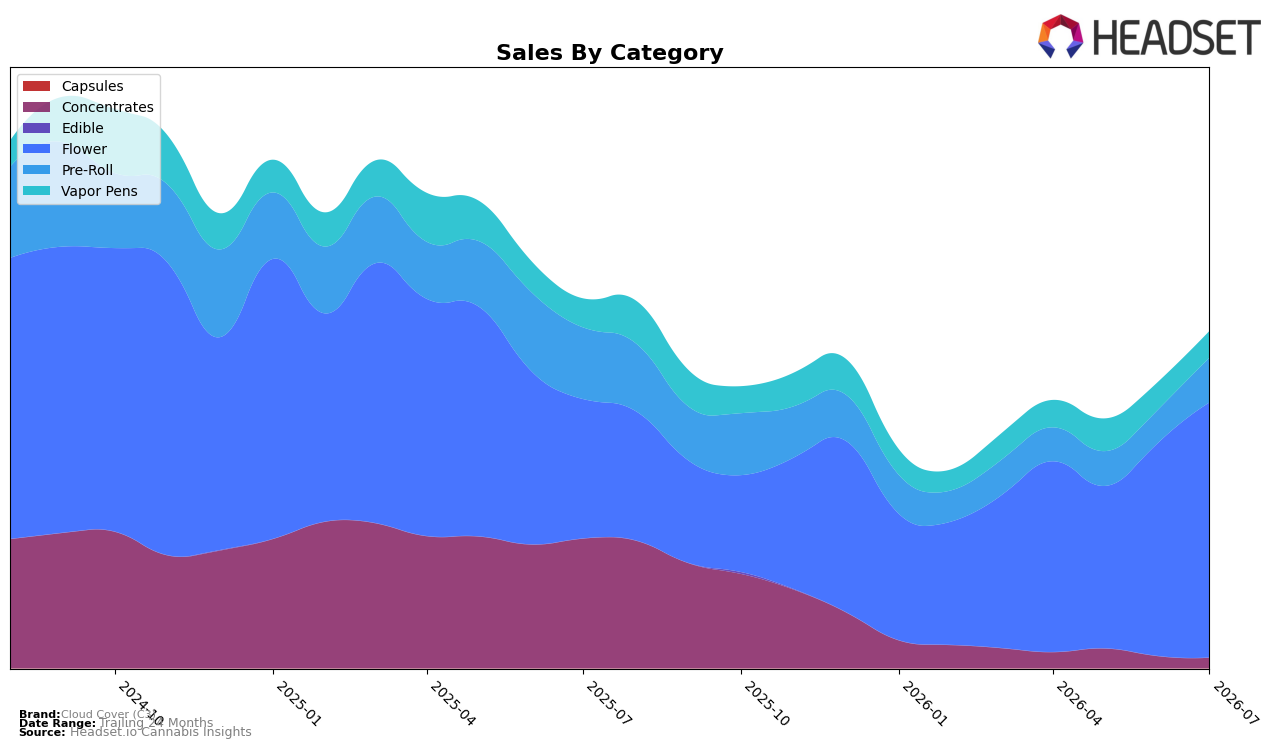

Cloud Cover (C3) concentrated 75.82% of July 2026 sales in Flower, with category sales up 83.25% year over year and 19.77% month over month, while Vapor Pens slipped 8.05% YoY and 4.05% MoM at a 7.87% share. Pre-Roll carried 13.23% share with a 34.90% MoM lift but a 37.71% YoY decline, and Concentrates fell 92.02% YoY and 12.90% MoM to 3.08% share; against a brand-level sales decline of 8.84% YoY and a 15.21% YoY rise in average price to $21.54, this mix implies Flower gains are offsetting deeper erosion in smaller categories. The overall pattern is a pivot toward higher-priced Flower (average $26.67) while legacy Concentrates contraction and Vapor Pens softness limit total recovery.

With Flower now the anchor, Cloud Cover (C3) is competing as a mid-shelf Flower-led brand rather than a multi-format portfolio, evidenced by a 21st rank in Flower in Missouri and a 19.77% MoM Flower uptick outpacing the 4.05% MoM decline in Vapor Pens. The 34.90% MoM rebound in Pre-Roll alongside a 37.71% YoY drop indicates promotional or assortment-driven volatility rather than durable scale, whereas the 92.02% YoY collapse in Concentrates suggests an exit or deprioritization that simplifies positioning but narrows cross-sell. The implication is that short-term share wins will come from defending and trading up within Flower while selectively stabilizing Pre-Roll mix, since reliance on Flower at 75.82% share concentrates risk and caps category reach.

Competitive Landscape

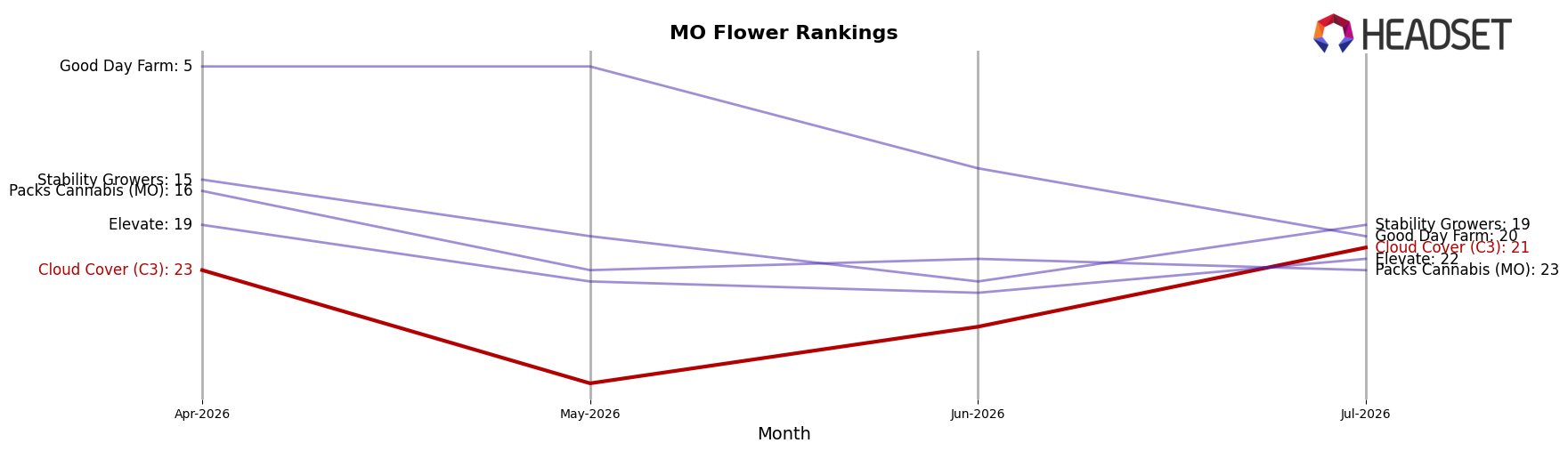

Cloud Cover (C3) sits at rank #21 in MO Flower in July 2026, improving 18 positions from #39 year over year, while edging up 2 spots from #23 in April 2026; this climb coincides with a peak rank of #21 in July 2026 and places the brand well behind Flora Farms at #1 and Sinse Cannabis at #2, with Sinse advancing from #4 to #2 and Local Cannabis Co. rising from #10 to #5. Relative momentum suggests Cloud Cover (C3)’s rank gains are outpacing the flat-to-declining leader at #1 (Flora Farms down 1.25% YoY sales) but may lag faster risers like Local Cannabis Co. whose sales grew 41.83% YoY, implying the current trajectory points to mid-tier consolidation unless conversion accelerates against top-5 climbers.

Notable Products

Detroit Runtz (3.5g) posted the steepest move in July 2026 with a -33.1% month-over-month drop to rank 10, while Apple Tartz (3.5g) surged +119.9% to rank 2, signaling volatility concentrated at both the bottom and near the top of the list. Frozen Dessert (3.5g) also advanced with an +81.8% MoM increase at rank 8, whereas LA Purp (3.5g) slipped -27.1% to rank 3, and seven of the top ten are Flower SKUs, indicating category concentration despite divergent trajectories within eighths and bulk. The single largest dollar contributor among top positions came from MAC Truck (Bulk) at $139,752 alongside stable bulk peers inside the top 10, contrasting with sharper swings in 3.5g eighths. The pattern implies Cloud Cover (C3) is leaning into bulk Flower for volume stability while using select 3.5g launches like Apple Tartz (3.5g) to create episodic spikes that can reorder the ranking mix.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.