Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

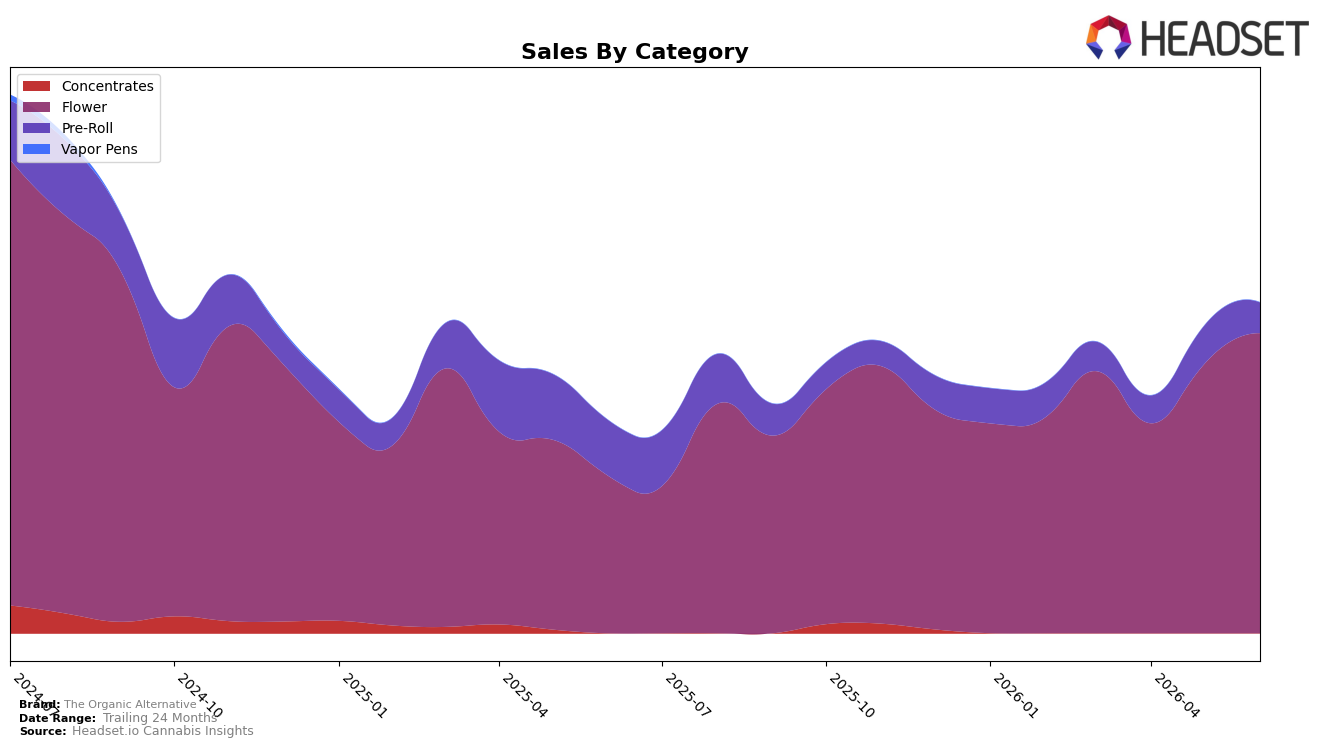

In June 2026, The Organic Alternative concentrated 90.81% of sales in Flower with year-over-year growth of 90.89% and month-over-month growth of 11.34%, while Pre-Roll held 9.19% share with a year-over-year decline of 45.20% and a month-over-month drop of 20.41%. Average price rose 56.95% year over year to $32.12 as Flower’s price point reached 36.73, coinciding with total brand sales growth of 55.41% year over year despite a 24-month contraction of 22.46%. This mix and pricing pattern implies the brand is leaning into higher-priced Flower to drive volume and margin, while allowing Pre-Roll’s shrinking share and negative momentum to release lower-value pressure from the portfolio.

With Flower anchoring rank 23 in Colorado and representing 90.81% of the mix, the 11.34% month-over-month Flower lift alongside a 20.41% month-over-month pullback in Pre-Roll implies a deliberate tilt toward a premiumized core rather than a breadth strategy. The combination of a 56.95% year-over-year average price increase and a 90.89% Flower growth rate indicates price elasticity remains favorable in the core segment, while the 45.20% year-over-year decline in Pre-Roll suggests de-prioritization of a lower-priced entry lane; together, these shifts imply positioning around depth in Flower where the brand can trade up and defend share at mid-pack category rank.

Competitive Landscape

The Organic Alternative sits at rank #23 in CO Flower in June 2026, improving 20 positions year over year from #43, while slipping 1 spot from March 2026’s #24 and remaining 7 places below its peak #16 from July 2024; by contrast, Seed & Strain Cannabis Co. climbed from #2 to #1 with 62.8% year-over-year sales growth and Natty Rems surged from #28 to #5 with 221.0% growth, indicating that The Organic Alternative’s rank rebound is outpaced by faster-moving leaders and suggesting its trajectory points to mid-tier consolidation rather than imminent top-10 entry unless velocity accelerates.

Notable Products

White Truffle (3.5g) posted the steepest move in June 2026 with a -65.6% month-over-month drop while sliding to rank 10, contrasting with Mishawaka Jazz Cabbage (3.5g) up 58.9% to rank 1 and Devil Driver (3.5g) up 50.9% at rank 3. Pre-Rolls were mixed as Golden Goat Pre-Roll 4-Pack (2g) fell -11.6% at rank 5 while the Mishawaka Jazz Cabbage Pre-Roll 4-Pack (2g) rose 16.3% at rank 6, and six of the top ten are Flower SKUs indicating concentration in inhalables. Despite Kush Mints (3.5g) slipping -8.2% at rank 2, the combined rise of Mishawaka Jazz Cabbage and Devil Driver across 3.5g and 14g formats suggests flagship strains are carrying share at the expense of weaker tail SKUs. The pattern implies The Organic Alternative is consolidating demand into a few lead strains and formats, signaling a tilt toward depth in core Flower over breadth across secondary offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.