Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

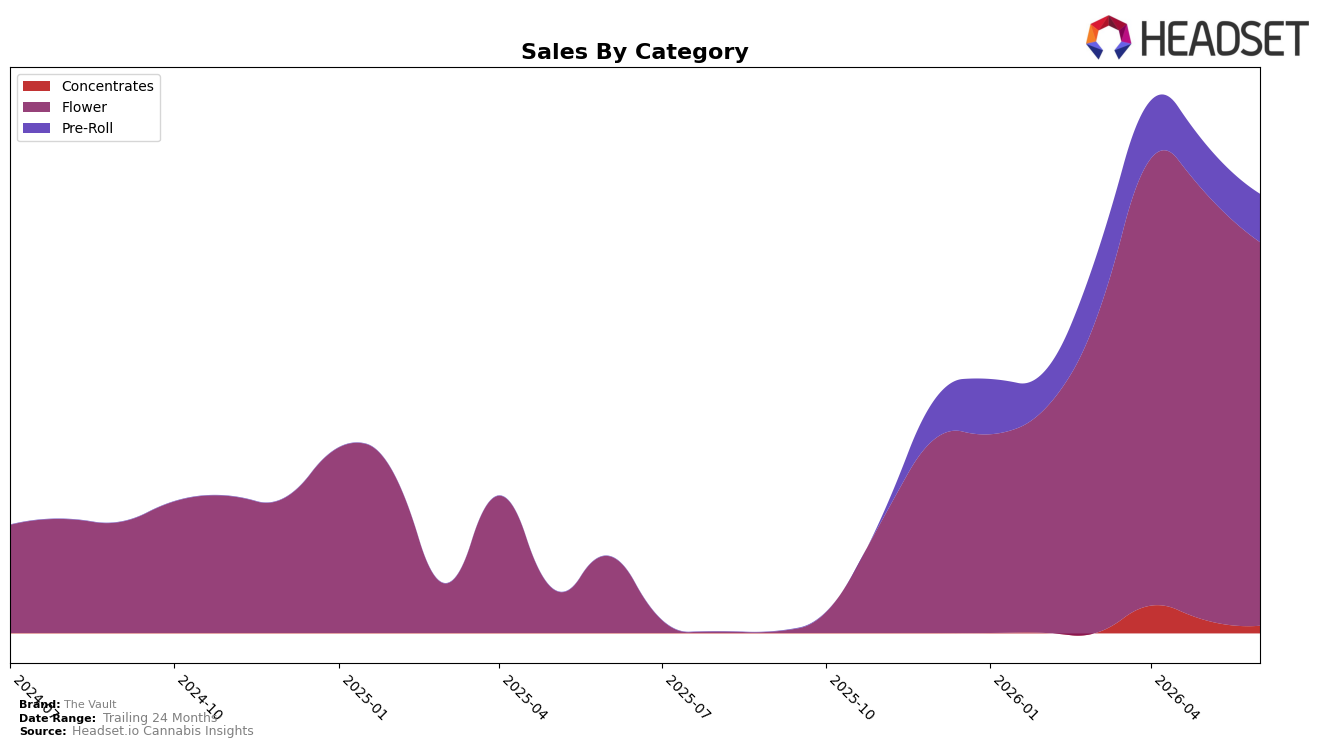

In June 2026, The Vault concentrated 87.40% of sales in Flower with a 400.65% year-over-year surge while posting a 10.37% month-over-month decline, and held 10.94% in Pre-Roll with a 1.77% month-over-month dip; Concentrates accounted for 1.65% share but fell 44.36% month-over-month. Despite a 26.14% year-over-year drop in overall average price to $26.61, Flower’s average price sat higher at $35.02, indicating price compression at the portfolio level alongside premium-weighted mix in the core category; combined, these shifts suggest The Vault is trading volume into Flower at lower unit pricing while trimming peripheral categories, a pattern that concentrates risk and constrains diversification.

With Flower dominance at 87.40% and a category rank of 30 in New Jersey Flower, the brand’s month-over-month pullback of 10.37% in its primary category alongside a 44.36% slide in Concentrates signals sensitivity to category cycles and a reliance on a single demand engine. The juxtaposition of a 400.65% Flower year-over-year lift against a 1.77% Pre-Roll month-over-month contraction implies that gains are skewed to one lane, so positioning skews toward volume capture over breadth; this mix tilts the brand toward price-driven Flower share battles rather than a hedge across adjacent inhalables.

Competitive Landscape

The Vault is ranked #30 in New Jersey Flower in June 2026, up 7 positions from #37 in March 2026, and it briefly peaked at #29 in May 2026 before slipping 1 spot month over month; with no year-over-year rank available, the immediate signal is a quarter-on-quarter climb paired with a short-term pullback. Meanwhile, Find. moved to #1 with a 12-position YoY rise and 225.99% YoY sales growth, and Ozone holds #2 despite a 2-position YoY improvement alongside a -10.61% YoY sales change, indicating that The Vault’s ascent from #37 to #30 places it behind competitors advancing faster or defending top tiers even with mixed growth. The pattern implies The Vault’s trajectory is upward but tentative, requiring sustained month-over-month gains to convert a Q2 rank lift into enduring top-25 presence.

Notable Products

Gorilla Glue #4 Pre-Roll (1g) posted the standout move with an 85.9% month-over-month surge to rank 2, while Gorilla Glue #4 (3.5g) fell 16.8% but still held rank 1. Kashmir Kush (3.5g) dropped 44.8% to rank 4, and Super Boof (3.5g) eased 8.3% at rank 5, indicating mixed traction across core Flower SKUs.

Flower concentrated the leaderboard with eight of the top ten, yet the only MoM gain above 30% came from a Pre-Roll, suggesting wallet shift into ready-to-smoke formats. Gelato Cream Cake (3.5g) rose 38.4% at rank 6 while Gorilla Glue #4 Smalls (7g) declined 15.3% at rank 7, and total category weighting is tilting from premium eighths toward value and convenience at roughly the $57k scale for the top SKU. The pattern implies The Vault’s commercial direction is pivoting toward form-factor diversification where Pre-Rolls capture incremental velocity while legacy Flower leaders defend rank through breadth rather than growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.