May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

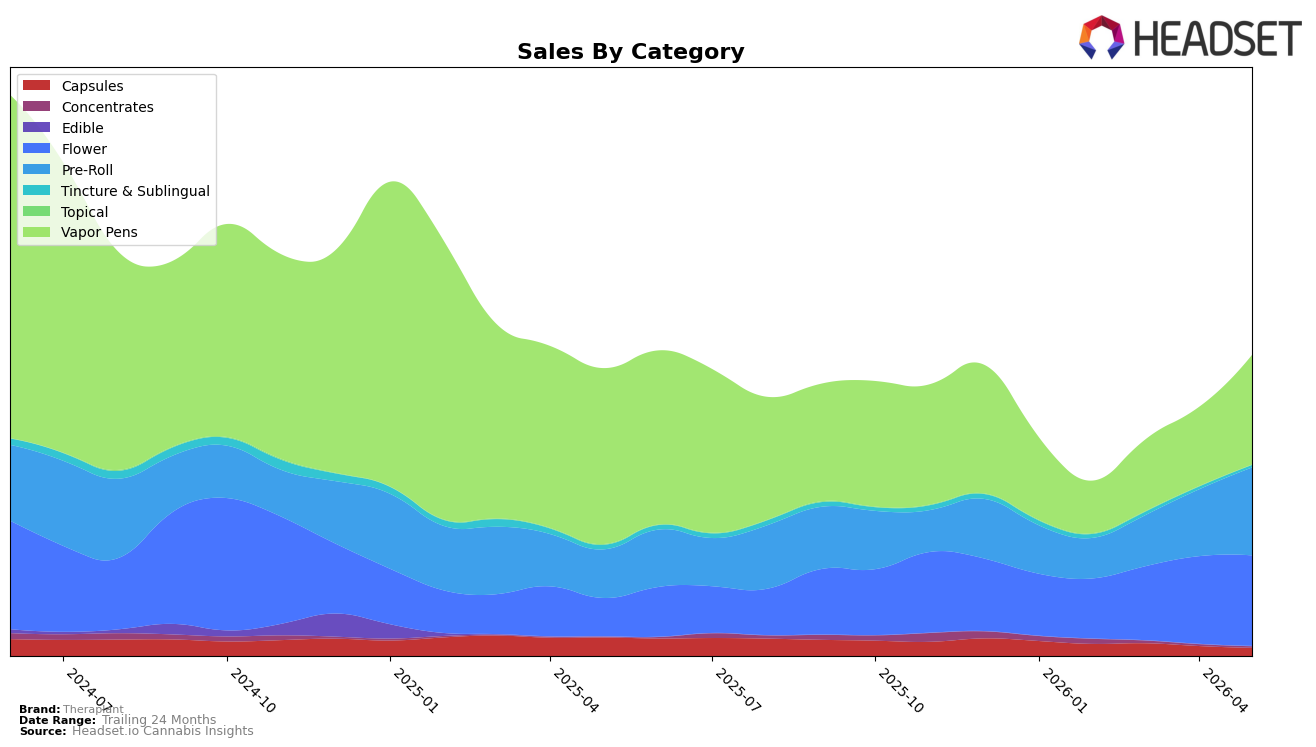

In May 2026, Theraplant’s mix tilted toward inhalables, with Vapor Pens at 36.64% share despite a -37.73% year-over-year decline and a 38.99% month-over-month rebound, while Flower expanded to 30.21% share on 137.25% year-over-year growth and a 3.37% month-over-month uptick. Pre-Roll reached 29.35% share with 81.56% year-over-year growth and a 31.99% month-over-month lift, whereas Capsules shrank to 2.65% share with -56.58% year-over-year and -18.52% month-over-month declines. Tincture & Sublingual fell to 0.72% share with -49.38% year-over-year and -13.87% month-over-month movement, and Concentrates held 0.41% share with 133.83% year-over-year growth but a -21.25% month-over-month dip. This pattern suggests Theraplant is consolidating around Flower and Pre-Roll momentum while using a short-term Vapor Pens bounce to stabilize overall mix, implying a pivot away from low-velocity wellness formats.

Positioning-wise, the rise in Flower and Pre-Roll share to a combined 59.56% alongside a -28.33% year-over-year drop in average price signals a trade-down or value-driven shift that can widen basket penetration while pressuring unit economics; the Vapor Pens rank of 3 in Connecticut creates a visibility anchor even as year-over-year category sales contracted. The simultaneous 38.99% month-over-month lift in Vapor Pens and 31.99% month-over-month lift in Pre-Roll indicates near-term elasticity to promotions or pricing, while Capsules’ -18.52% month-over-month decline and Tincture & Sublingual’s -13.87% month-over-month slide point to deprioritization of medical-adjacent SKUs. The implication is that Theraplant’s competitive stance is shifting toward higher-velocity inhalables where scale can be defended via price architecture, with the Vapor Pens rank of 3 in Connecticut serving as a platform to cross-convert consumers into Flower and Pre-Roll during promotional windows.

Competitive Landscape

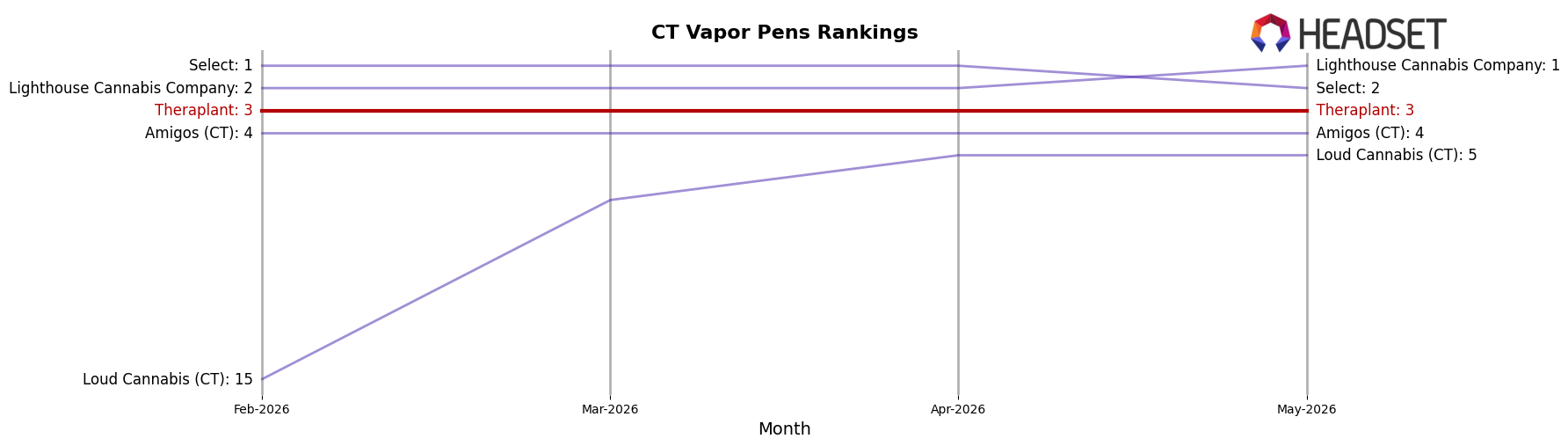

Theraplant holds rank #3 in CT Vapor Pens in May 2026, down 2 positions year over year from rank #1, and unchanged versus February 2026 at #3; this follows a prior peak at rank #1 in December 2025 and a quarter-stable placement at #3, indicating a slide from leadership to a persistent second-tier slot. Competitively, Lighthouse Cannabis Company moved up from rank #4 to #1 with a 50.3% year-over-year sales increase, while Select advanced from rank #3 to #2 on 36.0% year-over-year growth, placing Theraplant behind two brands that gained share and rank momentum in the same period. The pattern implies Theraplant’s trajectory is stabilizing below the leaders, where recovering from a 2-rank YoY decline will require reversing share losses that coincided with competitor climbs from #4 to #1 and #3 to #2.

Notable Products

Black Ch GMO (3.5g) posted the headline move with a 78.7% month-over-month jump to rank 2, while Permanent Marker Pre-Roll (1g) also cleared the +50% threshold with a 50.8% gain to rank 6. Pre-Rolls concentrated the leaderboard with six of the top ten slots, including Bananapple Medellin Infused Pre-Roll (1g) at rank 1 and Strawberry Candy Pre-Roll (1g) at rank 3, indicating share is tilting toward ready-to-use formats over Vapor Pens at ranks 7 and 9. The single highest dollar contributor among named movers was Black Ch GMO (3.5g) at $102,026, paired with a Pre-Roll surge that includes a 23.3% lift for Strawberry Candy Pre-Roll 5-Pack (2g) at rank 8, implying Theraplant is converting demand toward high-velocity Flower and value multi-pack Pre-Rolls rather than cartridge-led growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.