Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Traphouse Cannabis Co. is stocked at 188 licensed dispensaries across Michigan and Washington, 185 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Lansing, Monroe, and Ann Arbor. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

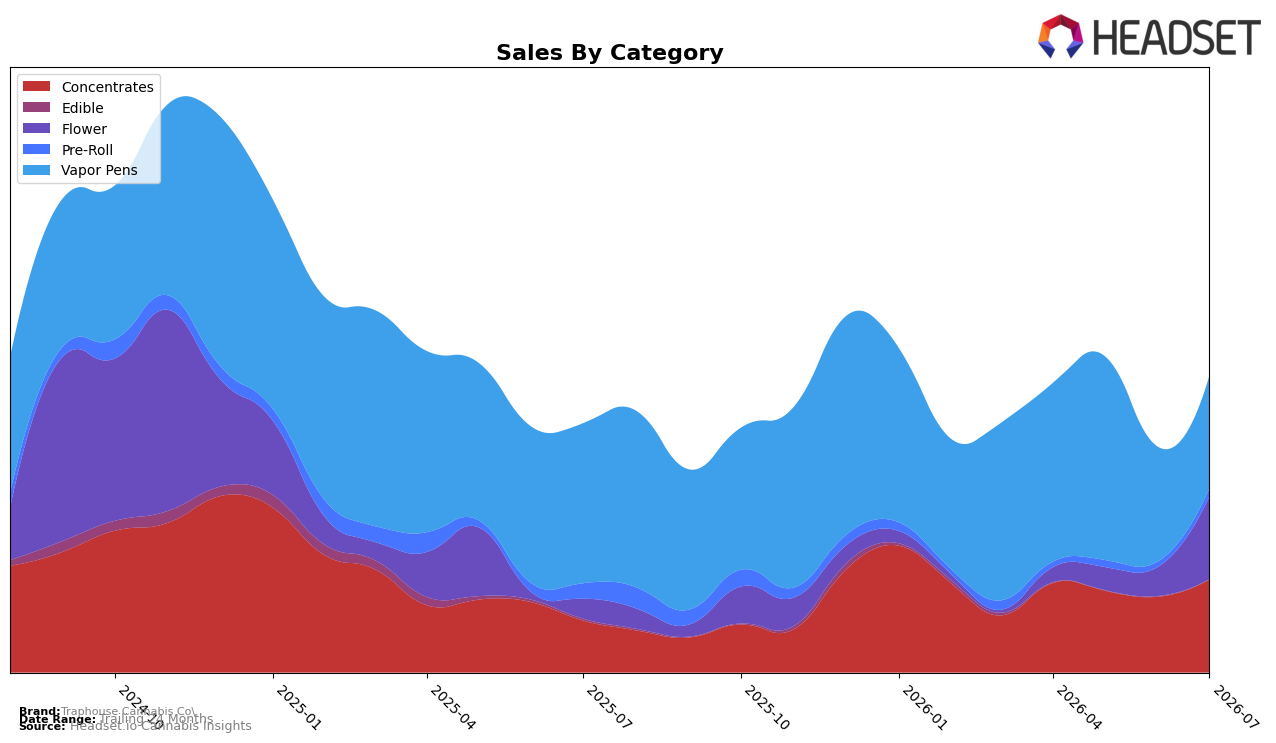

Traphouse Cannabis Co. concentrated its July 2026 mix in Vapor Pens at 37.90% share (ranked 28th in Michigan Vapor Pens) even as that category declined 29.52% year over year and slipped 1.55% month over month, while Concentrates expanded to 31.32% share with sales up 78.53% YoY and 22.77% MoM. Flower surged to 27.86% share on 311.62% YoY growth and 183.36% MoM, whereas Pre-Roll held just 2.78% share after a 47.04% YoY drop despite a 45.50% MoM rebound. The net effect is a pivot from a single-category concentration toward a three-pillar base led by Vapor Pens, Concentrates, and Flower, implying the July 2026 recovery in total sales (+19.07% YoY) hinges on sustaining double- and triple-digit growth in Concentrates and Flower while managing the Vapor Pens rank at 28.

With average price flat at +0.40% YoY to $7.99 and category-specific price points spanning $6.29 in Concentrates and $10.43 in Flower, the brand is trading mix rather than price to drive growth, as seen in Concentrates’ 22.77% MoM and Flower’s 183.36% MoM surges. The 78.93% YoY contraction in Edible (0.14% share) and the 47.04% YoY decline in Pre-Roll (2.78% share) indicate deliberate deprioritization of low share, low price pools, suggesting positioning that concentrates resources on higher-velocity extract formats; the implication is that maintaining Vapor Pens scale while expanding extract-adjacent share gives Traphouse Cannabis Co. a pathway to outgrow the July 2026 category headwind in Vapor Pens despite its 28th-place ranking.

Competitive Landscape

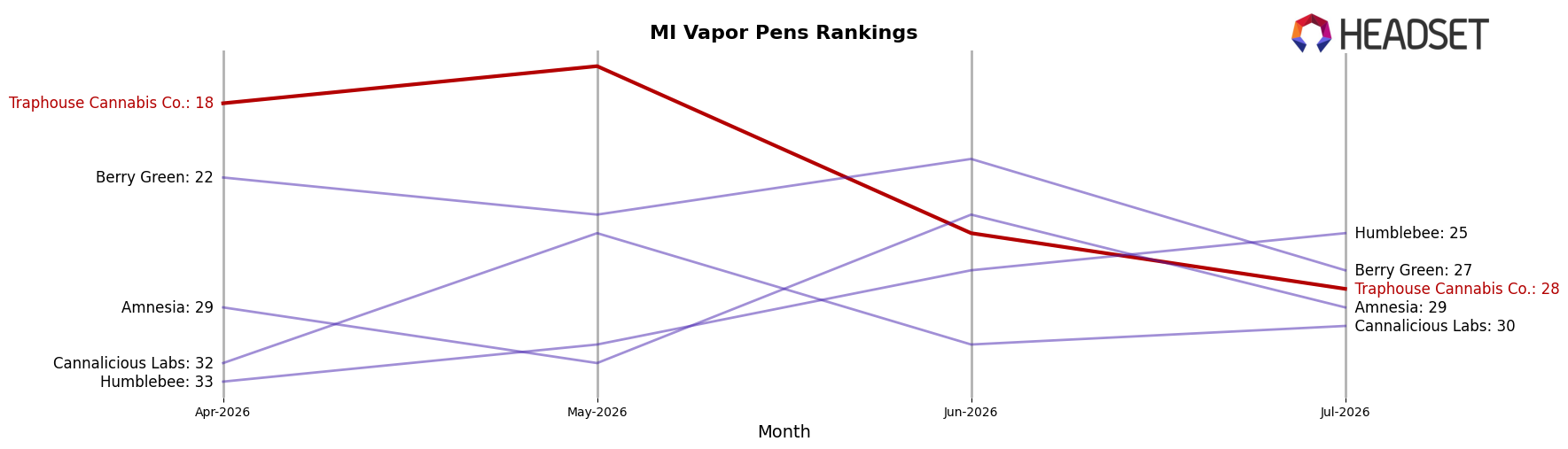

Traphouse Cannabis Co. sits at rank #28 in July 2026, down 11 positions year over year from #17 and 10 spots below April 2026’s #18, while remaining 16 places off its December 2024 peak at #12; against this slide, MKX Oil Company advanced to #1 with a 3-place YoY climb and 42.9% YoY sales growth, and Society C rose 14 ranks to #4 alongside a 360.8% YoY sales surge, indicating that Traphouse Cannabis Co.’s relative decline is tied less to absolute share loss and more to faster-moving leaders compressing the middle tier, a trajectory that implies further erosion unless rank-recovery levers reverse the 10-rank three-month slide.

Notable Products

Sweet Island Punch Distillate Cartridge (1g) fell 17.6% month over month to rank 4 while Super Lemon Haze Distillate Cartridge (1g) dropped 23.2% to rank 10, signaling volatility in lower-ranked Vapor Pens that contrasts with category leadership. Sour Tangie Distillate Cartridge (1g) gained 47.7% month over month to hold rank 1, and Strawberry Shortcake Distillate Cartridge (1g) dipped 3.9% at rank 2, meaning four of the top ten are Vapor Pens concentrated at the top but softening below the podium. With three Concentrates sitting at ranks 5, 8, and 9 alongside three Flower bulk SKUs at ranks 3, 6, and 7, the mix spreads revenue across inhalable formats while anchoring traffic in Vapor Pens, implying Traphouse Cannabis Co. is leaning into cartridges for headline velocity while using bulk Flower and Cured Resin to stabilize volume.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.