Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Treetown is stocked at 123 licensed dispensaries across Michigan, with the deepest coverage in Detroit, Lansing, Grand Rapids, Monroe, and New Buffalo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

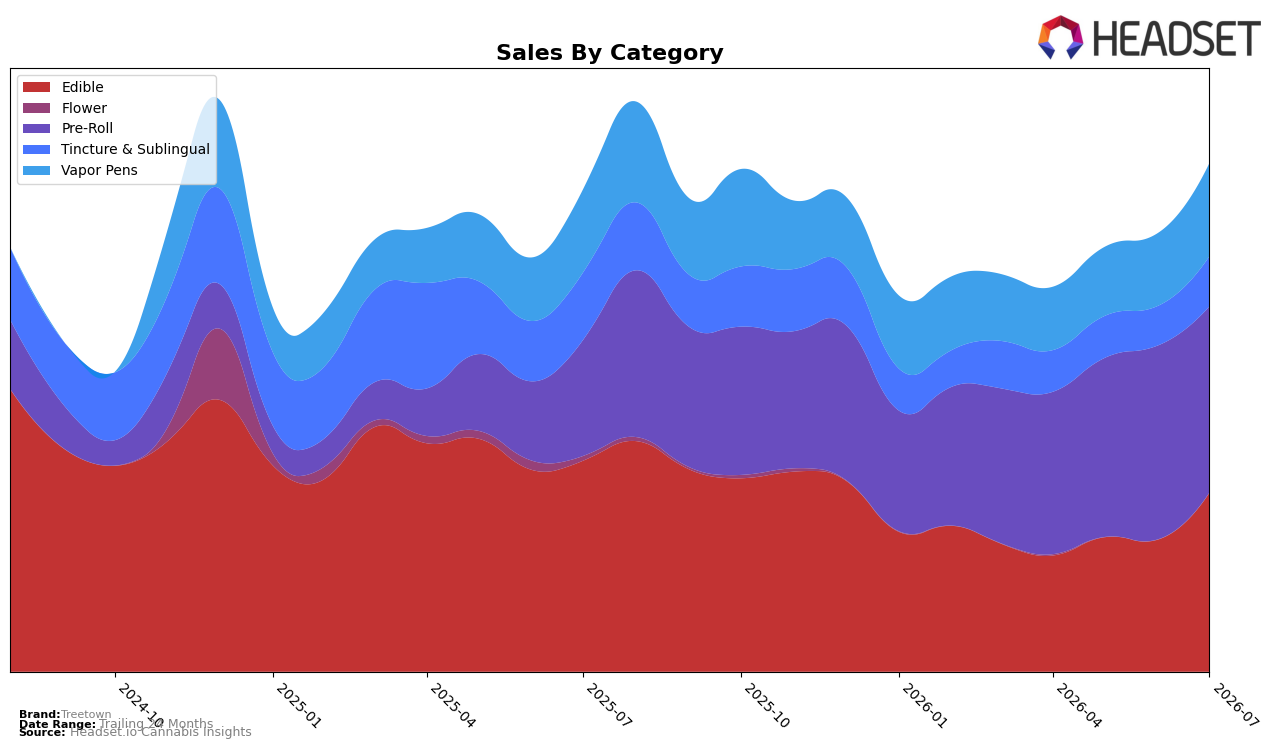

Treetown’s category mix in July 2026 tilted toward Pre-Roll at 36.64% share with 60.48% year-over-year growth but a 3.99% month-over-month decline, while Edible held 35.22% share with a 15.24% year-over-year decline but a 35.46% month-over-month rebound. Vapor Pens accounted for 18.31% share with 11.96% year-over-year growth and a 27.92% month-over-month lift, and Tincture & Sublingual stood at 9.83% share with a 25.79% year-over-year decline alongside a 26.86% month-over-month increase. Coupled with a July 2026 brand-level year-over-year sales change of 5.41% and a 27.16% year-over-year increase in average price, these cross-currents imply a portfolio rotating toward higher-velocity inhalables while legacy wellness formats retrench, setting up uneven momentum by channel.

The shift places Treetown as a Pre-Roll-led player that still relies on Edible for over one-third of mix, a combination that can buffer volatility: Pre-Roll’s 60.48% year-over-year surge offsets Edible’s 15.24% year-over-year drop, while the 27.92% month-over-month Vapor Pens lift complements Edible’s 35.46% month-over-month rebound. Given a 3.99% month-over-month dip in Pre-Roll against a 26.86% month-over-month rise in Tincture & Sublingual and an overall 27.16% year-over-year price increase, the pattern implies near-term pricing power anchored in inhalables with a tactical need to stabilize wellness formats; in Michigan Pre-Roll at rank 65 suggests headroom if the brand converts MoM gains in Vapor Pens into sustained share capture.

Competitive Landscape

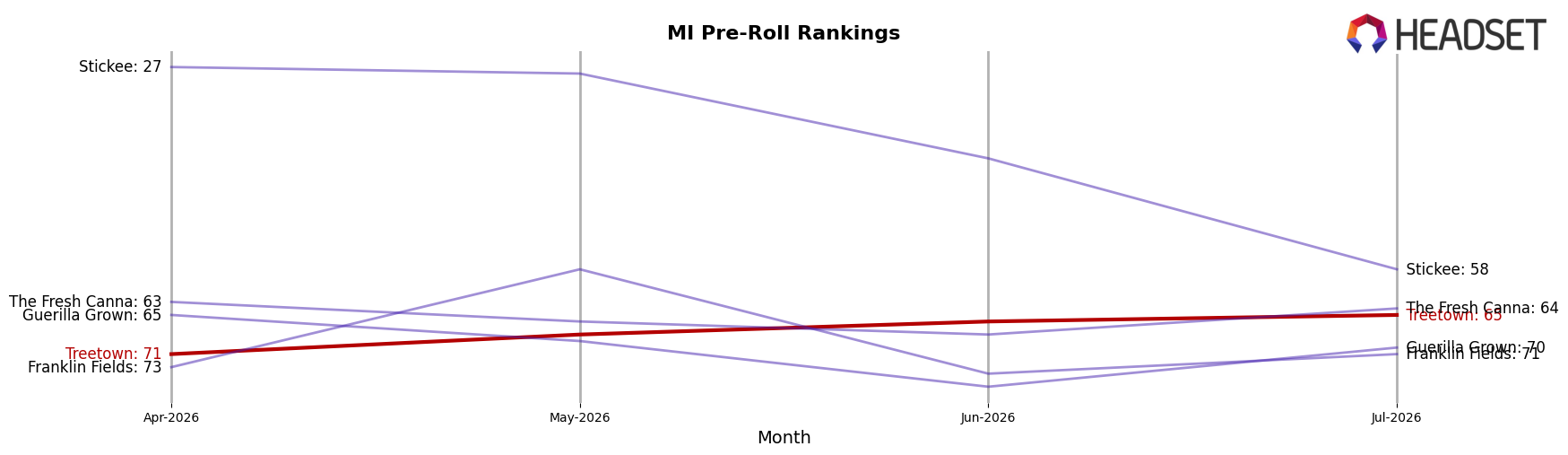

Treetown ranks #65 in Michigan Pre-Roll in July 2026, improving 26 positions YoY from #91 while edging up 6 ranks from April 2026’s #71; the brand also hit a peak rank of #65 in July 2026, indicating a recent ceiling. At the top end, Jeeter held #1 with a 4.0% YoY sales gain while Cali-Blaze stayed at #2 despite a 38.5% YoY decline, and Mitten Extracts climbed from #7 to #4 on 68.5% YoY growth, signaling that Treetown’s ascent is occurring as the leaderboard polarizes between gains and contractions. The pattern implies Treetown’s rank trajectory is upward but capped near the mid-60s unless it converts recent momentum into share-taking comparable to competitors that moved multiple top-10 slots.

Notable Products

CBD/THC 1:2 Euphoria Melon Gummies 10-Pack (50mg CBD, 100mg THC) posted the largest month-over-month change in July 2026 at +83.3%, jumping to rank 2 while Blue Raz Full Spectrum CannaMelt (200mg) fell -11.5% and slid to rank 8. Sleep - CBN/THC 2:1 Blackberry Lavender Gummies 10-Pack (100mg CBN, 50mg THC) grew +40.6% to hold rank 1 as CBD/THC 2:1 Tranquil Dragonfruit Gummies 10-Pack (100mg CBD, 50mg THC) advanced +40.6% into rank 10. With eight of the top ten SKUs in Edibles and only one Tincture & Sublingual product declining, the mix points to Treetown consolidating around functional gummy formats and deprioritizing non-edible form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.