Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Vertical (MO) is stocked at 151 licensed dispensaries across Missouri and Illinois, 150 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Springfield, and Joplin. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

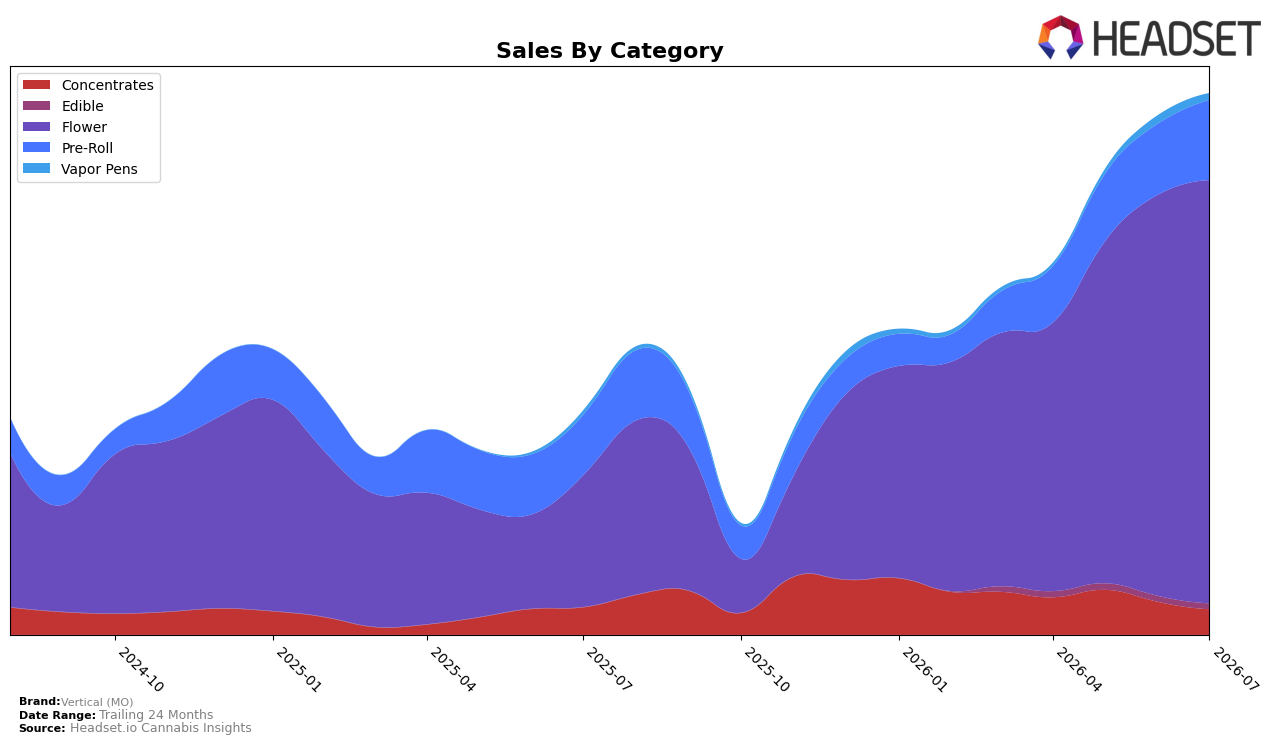

Vertical (MO) concentrated 78.31% of July 2026 sales in Flower, up 222.17% year over year and 5.49% month over month, while Pre-Roll accounted for 14.80% with 33.03% YoY growth and 12.96% MoM growth; meanwhile, Concentrates fell 6.99% YoY and 22.74% MoM to 4.67% share, and Vapor Pens declined 20.94% MoM despite a 56.52% YoY lift to 1.20% share. The brand’s overall July 2026 sales were up 142.59% YoY with an average price down 3.92%, and within its leading category the Flower rank in Missouri sat at position 12; this combination implies a volume-led expansion anchored by Flower mix concentration and tactical pricing while THC-adjacent formats retrench.

With Flower at 78.31% share and rank 12 in Missouri Flower, the 5.49% MoM gain paired with a 3.92% brand-wide price decline suggests Vertical (MO) is trading for velocity over ticket, whereas the 12.96% MoM rise in Pre-Roll against a 22.74% MoM drop in Concentrates signals portfolio simplification toward fast-turn inhalables. The 20.94% MoM contraction in Vapor Pens alongside a 56.52% YoY rise and the 1.16% MoM dip in Edible at 1.02% share indicate a deliberate de-emphasis of niche formats to protect Flower momentum; the implication is a positioning bet on Flower-driven shelf dominance with Pre-Roll as the secondary growth lane while higher-complexity categories are deprioritized.

Competitive Landscape

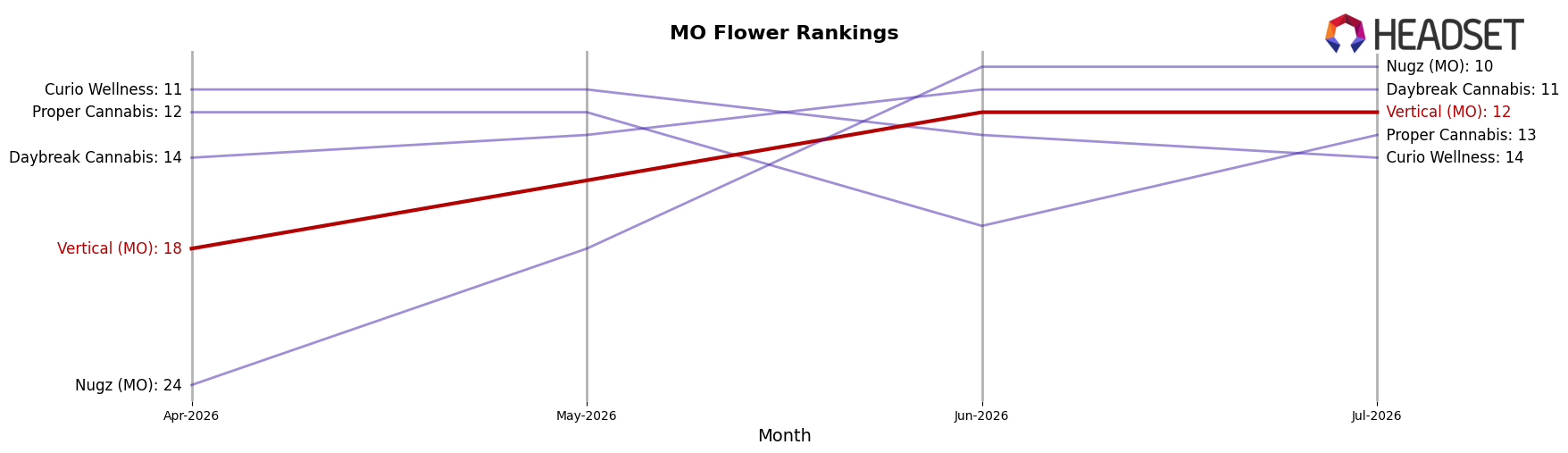

Vertical (MO) sits at rank #12 in Missouri Flower in July 2026, improving 20 positions from #32 year over year, and climbing 6 spots from #18 in April 2026; the brand also hit its peak rank of #12 in July 2026, indicating a ceiling test concurrent with its latest move. In contrast, Flora Farms held #1 with a 1.3% year-over-year sales decline while Sinse Cannabis advanced to #2 with a 9.0% sales increase, showing that Vertical (MO)’s 20-rank YoY surge is driven more by share capture below the top tier than displacement at the very top. The pattern implies Vertical (MO)’s rank trajectory is momentum-based within the mid-tier, with further gains requiring outpacing competitors who are either stable at #1 or growing into #2.

Notable Products

LA Kush Cake (3.5g) set the tone in July 2026 with an 83.1% month-over-month surge to rank 1, while Jokerz Candy (3.5g) slid 22.2% to rank 3 and Blueberry Cupcake (3.5g) fell 15.2% to rank 10. Four of the top ten are Flower SKUs from the same 3.5g format, and their mixed momentum — from Applescotti (3.5g) down 1.4% at rank 2 to Lemon Batter (3.5g) down 21.6% at rank 9 — indicates reliance on strain rotation to carry the leaderboard. With LA Kush Cake (3.5g) adding over $114,000 and widening the gap over mid-pack items, the pattern implies Vertical (MO) is consolidating share around one breakout strain while the rest of the 3.5g lineup undergoes pruning and repositioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.