Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Wojo Co is stocked at 305 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Grand Rapids, Detroit, Lansing, and Monroe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

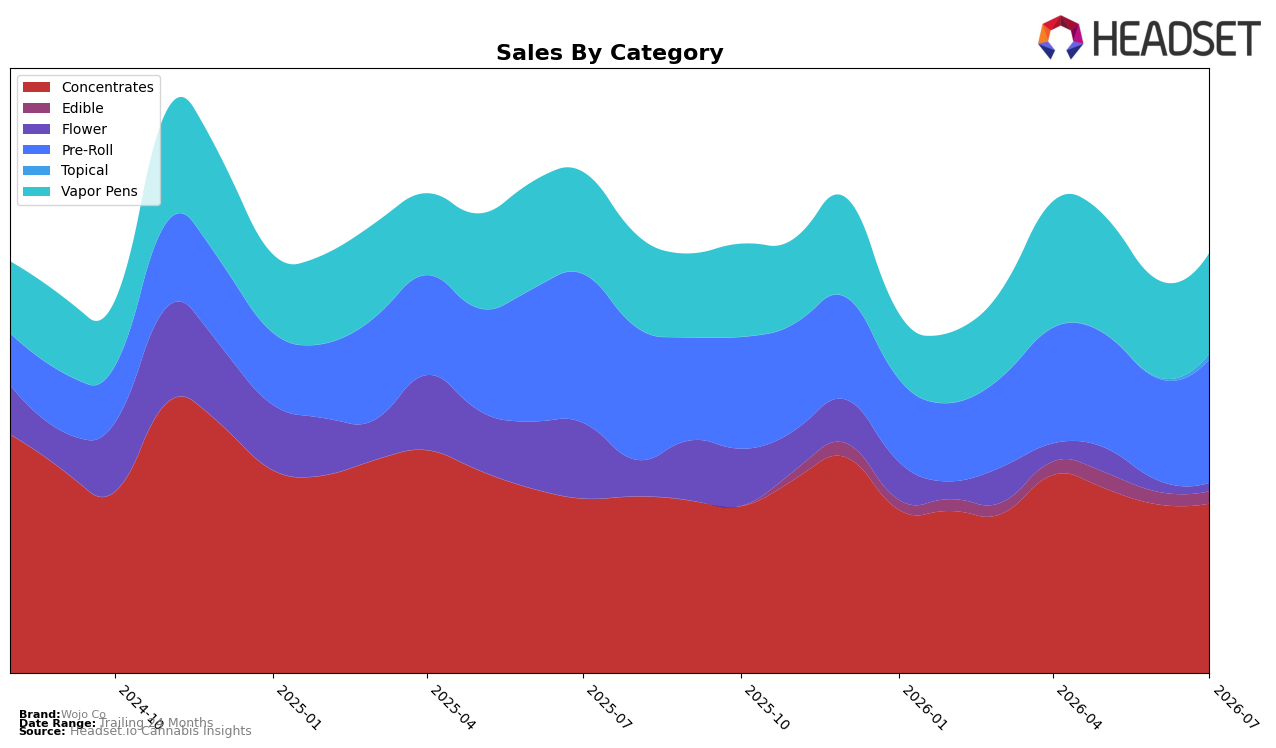

Wojo Co concentrated its July 2026 mix in Concentrates at 40.45% share with a month-over-month gain of 0.48% but a year-over-year dip of 2.82%, while Pre-Roll climbed to 29.39% share on a 21.19% month-over-month jump despite a 17.08% year-over-year decline. Vapor Pens held 23.98% share with 3.48% month-over-month growth and a 1.13% year-over-year decline, as Flower contracted to 1.97% share with a 26.14% month-over-month drop and an 89.06% year-over-year fall. Edible inched down 2.41% month-over-month to 2.90% share, and Topical spiked 486.21% month-over-month to 1.32% share from a small base. With overall brand sales down 16.17% year over year and average price down 7.67% year over year to $24.31, the pattern implies Wojo Co is leaning into inhalables stability while pruning low-velocity Flower and allowing opportunistic Topical bursts to backfill volume without materially changing the core mix.

Positionally, a 7th-place rank in Concentrates in Michigan suggests Wojo Co’s best visibility sits where price points remain above the brand average ($34.54 vs. $24.31), while the 21.19% month-over-month surge in Pre-Roll tilts the portfolio toward value-access volume despite its 17.08% year-over-year drag. The 3.48% month-over-month lift in Vapor Pens, paired with only a 1.13% year-over-year decline, indicates a steadier retention lane than Flower’s 89.06% year-over-year collapse and 26.14% month-over-month slide. Collectively, these shifts imply the brand’s defensible position is mid-to-premium inhalables anchored by Concentrates and supported by steady Pens, using Pre-Roll as an acquisition funnel while exiting Flower to reduce volatility and protect rank in Concentrates.

Competitive Landscape

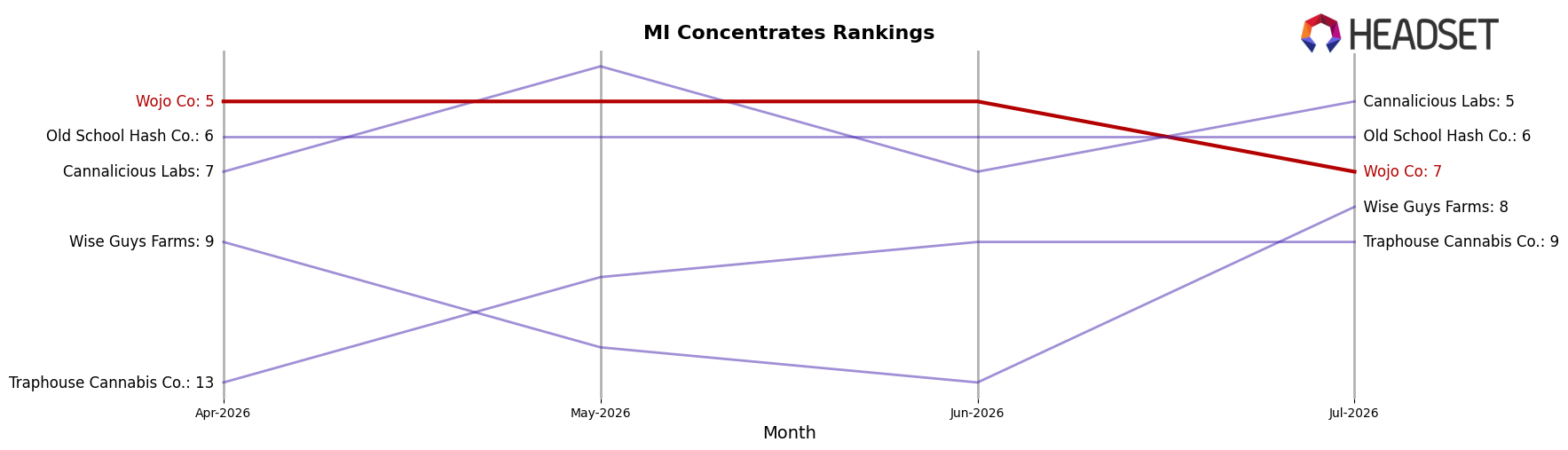

Wojo Co sits at rank #7 in July 2026, down 3 positions year over year from #4, and 2 spots below its April 2026 rank of #5; despite a historical peak at #2 in December 2024, the brand’s three-month slippage contrasts with Rkive Cannabis climbing from #5 to #1 and Uniq Pressure surging 142 places to #3 with 9,866% YoY sales growth. With Cannalicious Labs easing from #2 to #5 amid a 29.6% YoY sales decline while The Limit edged up from #1 to #2 as sales dipped 1.7%, the directional mix indicates Wojo Co is being outpaced by fast risers at the top and losing ground to volatility around it; the rank trajectory implies share reallocation away from mid-tier incumbents and signals that, absent a catalyst, Wojo Co is more likely to continue ceding rank than to reclaim its December 2024 peak.

Notable Products

Beach Wedding Live Rosin Disposable (0.5g) posted the largest month-over-month move in July 2026 with a 60.6% gain, climbing to rank 2 while Luchini Live Rosin Disposable (0.5g) rose 29.2% at rank 7. Within the top ten, five SKUs are Pre-Roll products concentrated across ranks 1, 5, 8, 9, and 10, while Vapor Pens occupy ranks 2, 3, 6, and 7, indicating a tilt toward inhalables that favors higher-velocity disposables. The top Pre-Roll, Stingerz- Strawberry Candy Infused Pre-Roll 3-Pack (1.5g), holds rank 1 as Strawberry Candy Pre-Roll (1g) advanced 21.1% at rank 9, concentrating demand in flavored and infused formats. This mix implies Wojo Co is consolidating around flavored inhalables and live rosin disposables, prioritizing formats that can scale velocity at the expense of breadth in other categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.