Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

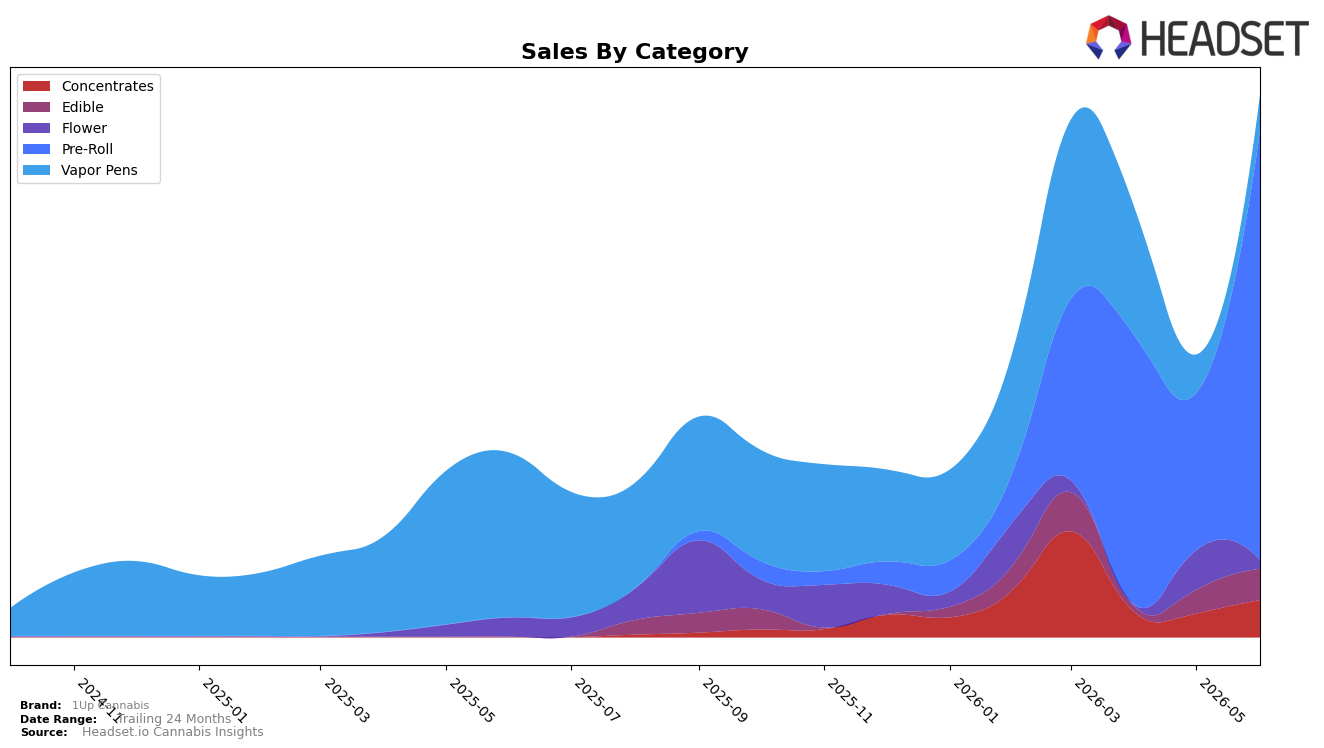

In June 2026, 1Up Cannabis concentrated 79.24% of sales in Pre-Roll with a month-over-month surge of 173.36%, while Vapor Pens fell 5.82% MoM and 78.17% YoY to 6.62% share; Flower contracted to 1.60% share with a 77.97% MoM decline and 53.74% YoY drop. Secondary categories expanded unevenly: Concentrates reached 6.85% share with 58.02% MoM growth, and Edible climbed 31.48% MoM to 5.69% share, alongside a 6.18% YoY rise in overall average price and a brand-level 195.82% YoY sales increase. The pattern implies a deliberate pivot toward Pre-Roll scale at higher ticket sizes in June 2026 while de-emphasizing Vapor Pens and Flower, using Concentrates and Edible as incremental volume buffers.

That mix shift puts 1Up Cannabis into a volume-led, impulse-friendly posture anchored by Pre-Roll, which correlates with a rank of 14 in Pre-Roll in Michigan and suggests near-term headroom if the 173.36% MoM acceleration can convert to sustained share gains. However, the concurrent contraction in Vapor Pens (-78.17% YoY) and Flower (-77.97% MoM) concentrates category risk into a single format even as Concentrates posted 58.02% MoM growth and Edible added 31.48% MoM, implying positioning that trades breadth for depth; the thesis is that Pre-Roll-led scale can lift rank, but resilience will depend on whether secondary categories maintain 30–60% MoM momentum as Vapor Pens and Flower retrench.

Competitive Landscape

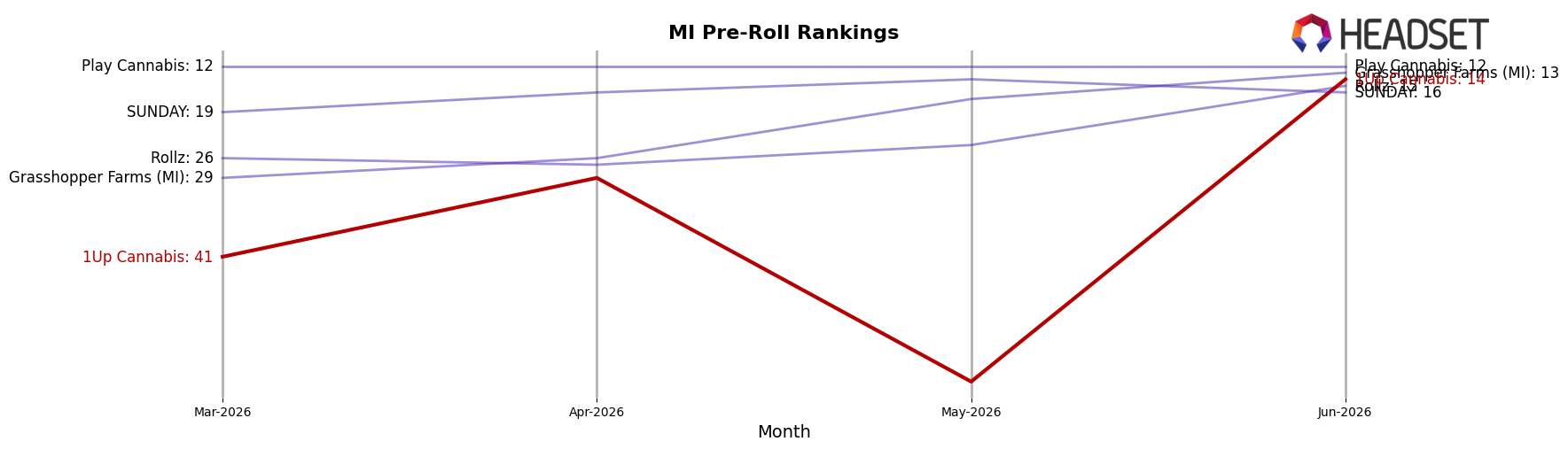

1Up Cannabis sits at rank #14 in MI Pre-Roll in June 2026, improving 27 positions from #41 in March 2026 and setting a new peak at #14 in June 2026; with no June 2025 rank available, the near-term climb is the clearest signal of momentum. Against incumbents, Jeeter holds #1 while posting a -7.9% year-over-year sales change, and Cali-Blaze remains #2 with a -33.1% year-over-year sales change, whereas Dragonfly Cannabis is #3 with a +13.7% year-over-year gain; this mix suggests headroom for share capture as 1Up Cannabis advances from #41 to #14. Meanwhile, Mitten Extracts rose to #4 from #8 year over year alongside +114.4% sales growth, and Goodlyfe Farms slid from #4 to #5 with -32.3% year-over-year sales change, indicating that volatility in the top five coexists with 1Up Cannabis’s 27-rank climb; the trajectory implies 1Up Cannabis is transitioning from fringe presence to mid-tier contender with a path to breach the top 10 if the recent rank acceleration persists.

Notable Products

AK47 Infused Blunt 5-Pack (3.75g) posted the standout move with a +272% month-over-month surge, jumping into rank 5 while Blue Dream Infused Pre-Roll 5-Pack (3.75g) climbed +125% to rank 10, and Skittles Infused Blunt 5-Pack (3.75g) added +161% at rank 6. Edibles remained concentrated at the very top with three gummy SKUs holding ranks 1–3 and another at rank 4, yet their MoM gains of +26% to +49% lagged the triple-digit acceleration in Pre-Rolls, indicating a category power shift despite Cherry Berry Gummies 4-Pack (200mg) retaining rank 1. The presence of five infused Pre-Roll 5-Packs in ranks 5–10, three of which grew between +125% and +272%, signals a pivot in consumer pull toward infused multi-packs even as gummies continue to anchor headline positions. The mix implies 1Up Cannabis is transitioning from gummy-led volume to infused Pre-Roll momentum, with bigger upside concentrated in the mid-ranking SKUs where absolute sales like $81,813 for AK47 Infused Blunt 5-Pack (3.75g) can scale further.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.