May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

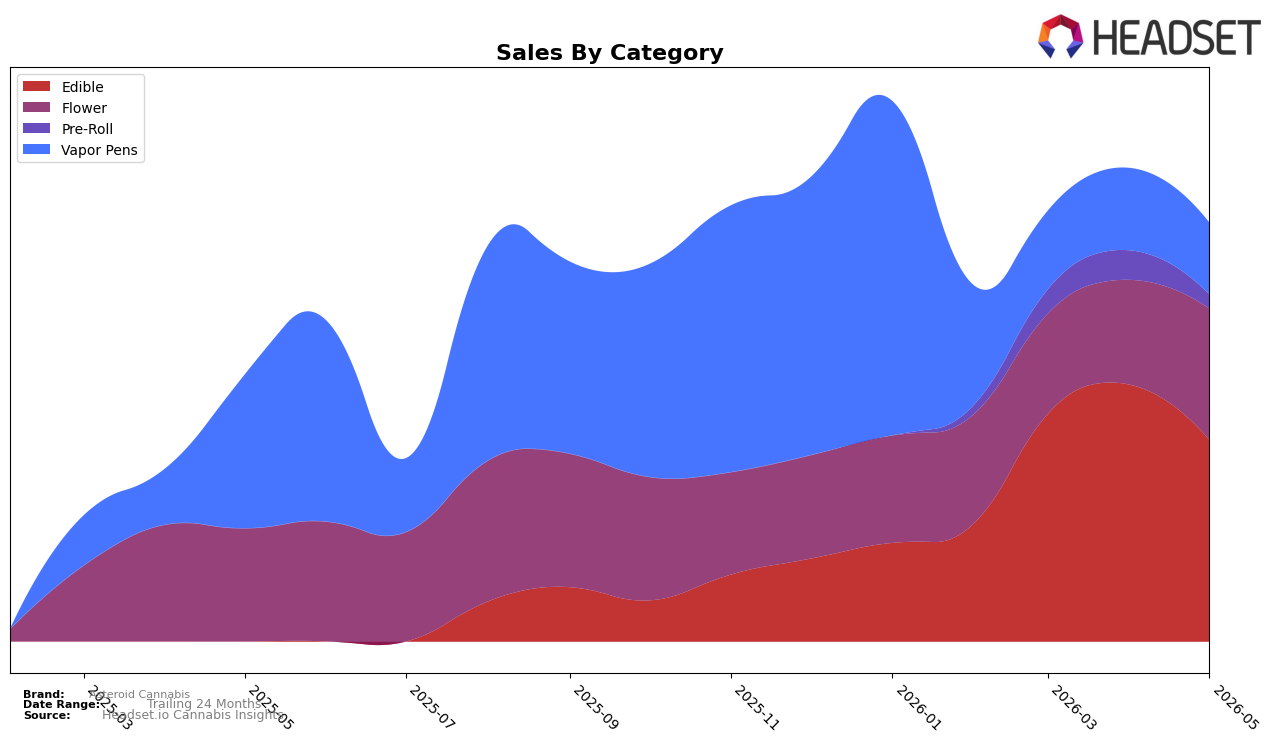

Asteroid Cannabis concentrated nearly half of May 2026 sales in Edible at 48.22% share, while Flower held 31.36% and Vapor Pens 17.11%, a mix that shifted month over month as Edible declined 21.50% and Pre-Roll fell 52.48%, contrasted by a 25.30% Flower increase. Year over year, Flower grew 16.33% as Vapor Pens contracted 53.57%, and brand-wide sales rose 56.74% alongside a 44.14% drop in average price, indicating volume expansion. In Connecticut Edible, the brand ranked 5, so the category-led pullback and rank position together imply the portfolio is leaning on Flower momentum to offset Edible softness while price compression recruits buyers.

The mix pivot implies a strategic reweighting: with Edible’s 48.22% share shrinking on a 21.50% month-over-month decline versus Flower’s 25.30% month-over-month gain and 16.33% year-over-year lift, the brand’s positioning is migrating toward inhalables for near-term growth. Given Vapor Pens’ 53.57% year-over-year contraction and 12.95% month-over-month dip alongside a 44.14% brand-wide price decrease, pricing is likely being used to defend share in lagging formats while Flower absorbs demand; coupled with a rank of 5 in Connecticut Edible, the pattern implies prioritizing Flower depth and targeted Edible retention to sustain the 56.74% year-over-year sales increase.

Competitive Landscape

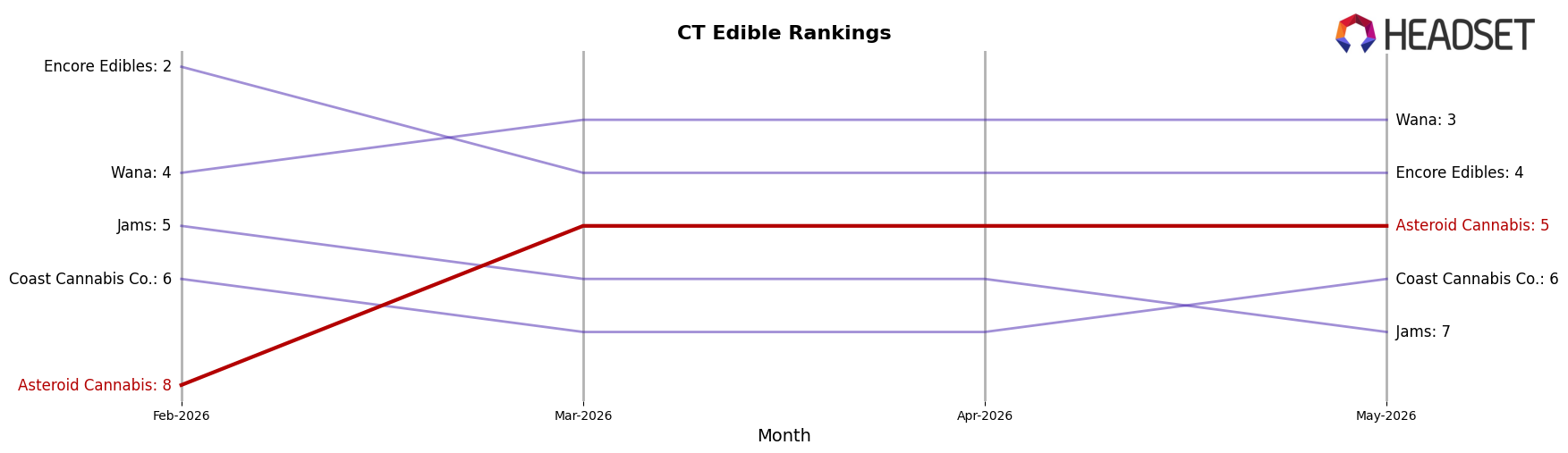

Asteroid Cannabis is ranked #5 in CT Edible in May 2026, up 3 positions from #8 in February 2026, marking its peak-to-date at #5 in May 2026; meanwhile, Soundview sits at #1 with a year-over-year rank shift of +2 and Encore Edibles holds #4 despite a -56.3% YoY sales change, indicating Asteroid Cannabis has closed the gap on a weakening adjacent rival while still trailing a rising leader. Compared with Wana at #3 with a +3 YoY rank and +42.5% YoY sales growth, and Camino at #2 with a +6 YoY rank and +384.4% YoY sales growth, Asteroid Cannabis’s climb from #8 to #5 over three months occurs amid competitors accelerating or contracting around it, implying the brand’s trajectory is upward but will require share wins against faster-moving leaders to break into the top three.

Notable Products

Galaxeats - Sour Watermelon Gummies 20-Pack (100mg) posted the standout move in May 2026 with a +93.99% month-over-month surge while climbing to rank 6, contrasting with Galaxeats - Piña Colada Gummies 20-Pack (100mg) dropping -42.84% to rank 4. Galaxeats - Pink Lemonade Gummies 20-Pack (100mg) led at rank 1 despite a -30.43% decline, and Galaxeats - Raspberry Rush Gummies 20-Pack (100mg) advanced +26.04% at rank 2, indicating a redistribution of demand within the same family. Eight of the top ten SKUs were Edibles under the Galaxeats line, concentrating mix away from Flower and Vapor Pens despite Black Hole Gum Infused Pre-Ground (3.5g) holding rank 5 and Northern Light Cookies Distillate Cartridge (1g) at rank 8 with $18,649 in sales. The pattern points to an Edibles-led portfolio where volatility within flavors is redefining the leaderboard, implying Asteroid Cannabis is leaning into confection SKUs as the commercial fulcrum while non-edible formats act as secondary stabilizers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.