Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

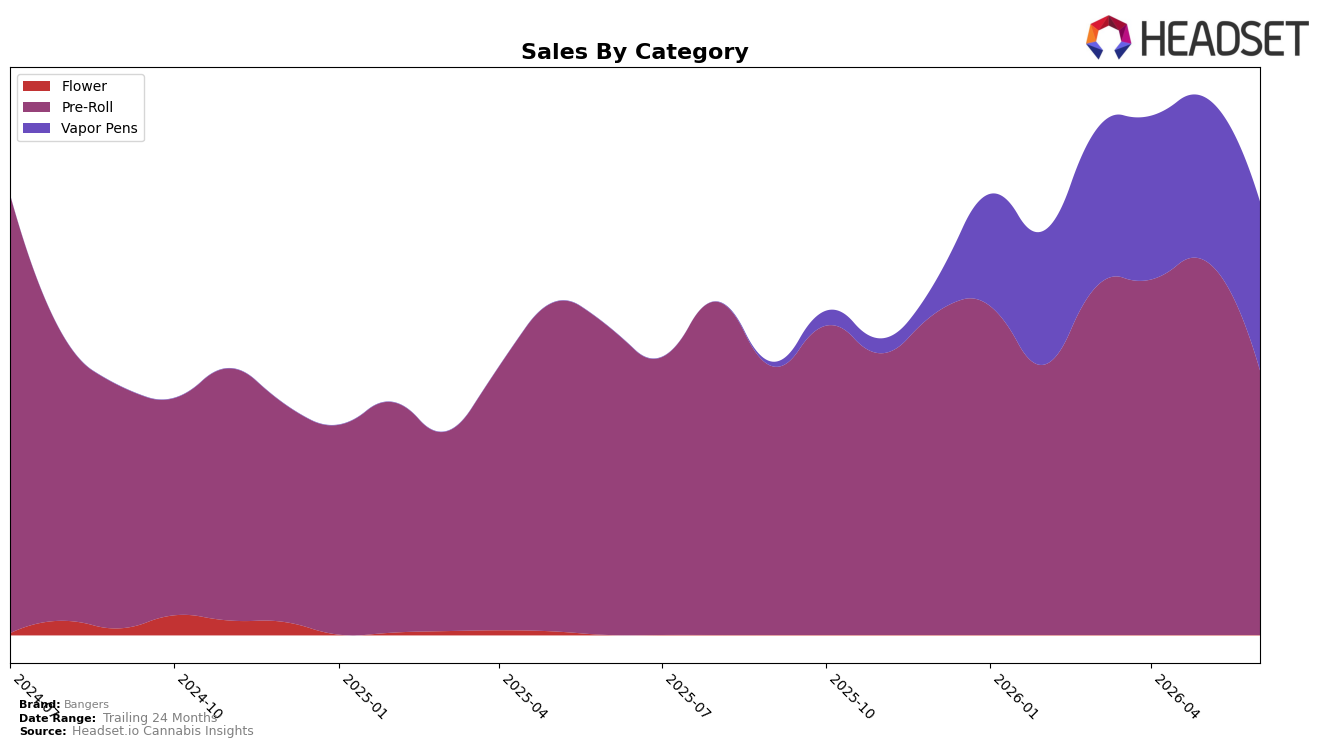

In June 2026, Bangers’ mix pivoted toward Vapor Pens as Pre-Roll share fell to 61.05% with a year-over-year decline of 14.29% and a month-over-month drop of 29.40%, while Vapor Pens rose to 38.95% share with a 3.44% month-over-month gain; this shift occurred alongside a 27.09% YoY increase in average price and a 40.41% YoY lift in total brand sales. Within Oregon Vapor Pens, Bangers held rank 30, indicating category momentum that contrasts with the double-digit Pre-Roll contractions; the implication is a reallocation toward a higher-price segment where the brand’s mix is becoming more concentrated despite Pre-Roll volume erosion.

The mix change implies a deliberate tilt toward higher ticket items, as Vapor Pens’ 38.95% share plus a 3.44% MoM lift offsets Pre-Roll’s 29.40% MoM contraction, helping sustain a 40.41% YoY brand sales increase despite Pre-Roll’s 14.29% YoY retreat. Sitting at rank 30 in Oregon Vapor Pens while Pre-Roll weakens suggests Bangers is migrating its demand base to a segment where pricing power, reflected in the 27.09% YoY average price rise, can carry growth; operationally, this points to prioritizing pen assortment and velocity over Pre-Roll recovery to consolidate share gains.

Competitive Landscape

Bangers sits at rank #30 in OR Vapor Pens in June 2026, a 3-position improvement from #33 in March 2026, with its peak rank also #30 in June 2026; meanwhile, Buddies holds #1 with a year-over-year position gain from #2 and FRESHY advanced from #5 to #2 alongside an 81.5% sales increase, indicating that upward mobility at the top is accelerating faster than Bangers’ incremental climb. Compared with Oregrown rising from #11 to #5 and Entourage Cannabis / CBDiscovery sliding from #1 to #3 with a 38.9% sales decline, Bangers’ 3-rank quarter-over-quarter gain to #30 suggests it is stabilizing at the category’s fringe while leadership churn concentrates in the top 5; the trajectory implies Bangers is improving tactically but not yet pacing with the rapid rank shifts that are reshaping the leaderboard.

Notable Products

Frosted Blueberry OG Infused Pre-Roll 2-Pack (1.2g) posted the steepest decline at -55.1% and sat at rank 6, while Cherry Zlushie Infused Pre-Roll 2-Pack (1.2g) fell -59.5% to rank 8, marking a sharp retrenchment in infused Pre-Rolls. By contrast, White Widow Distillate Cartridge (2g) surged +96.7% to rank 2 with $40,951 in June 2026, and Blue Dream Distillate Cartridge (2g) rose +36.8% at rank 5, signaling a pull of demand toward Vapor Pens. The top ten skew toward Pre-Rolls with six of the top ten in that family, yet the only MoM gains above +30% are in Vapor Pens, implying a category mix that is over-indexed to declining formats. The pattern indicates Bangers is pivoting in-market toward higher-momentum Vapor Pens even as its shelf remains concentrated in Pre-Rolls, suggesting reallocation could accelerate share capture.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.