Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

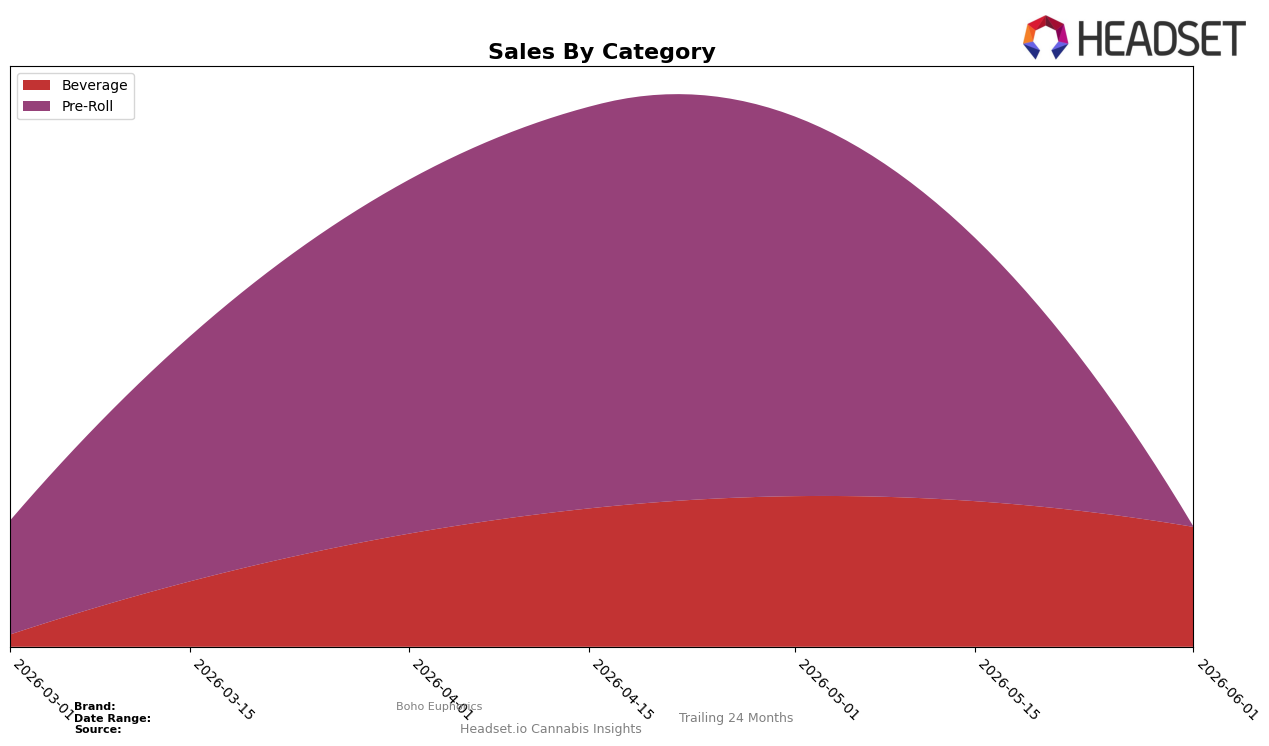

Boho Euphorics concentrated 74.08% of June 2026 sales in Beverage while Pre-Roll held 25.92%, and within-month shifts were steep: Beverage declined 14.32% month over month and Pre-Roll fell 85.50% month over month. In the Beverage category, the brand sat at rank 4 in New Jersey, and the category’s lower average price of $14.59 versus $27.06 in Pre-Roll indicates a deliberate tilt toward lower-ticket velocity; the pattern implies a defensive pivot toward core Beverage volume even as category breadth narrows.

The rapid contraction in Pre-Roll share alongside a 14.32% month-over-month dip in Beverage suggests the brand is trading assortment depth for price-accessible throughput, with rank 4 signaling viable visibility despite the pullback. Given that 74.08% of mix now hinges on Beverage and Pre-Roll’s 85.50% month-over-month drop reduces higher-price exposure, the implication is a positioning anchored in repeat, value-driven Beverage occasions rather than premium basket expansion, which may support rank stability in New Jersey but caps upside without renewed cross-category contribution.

Competitive Landscape

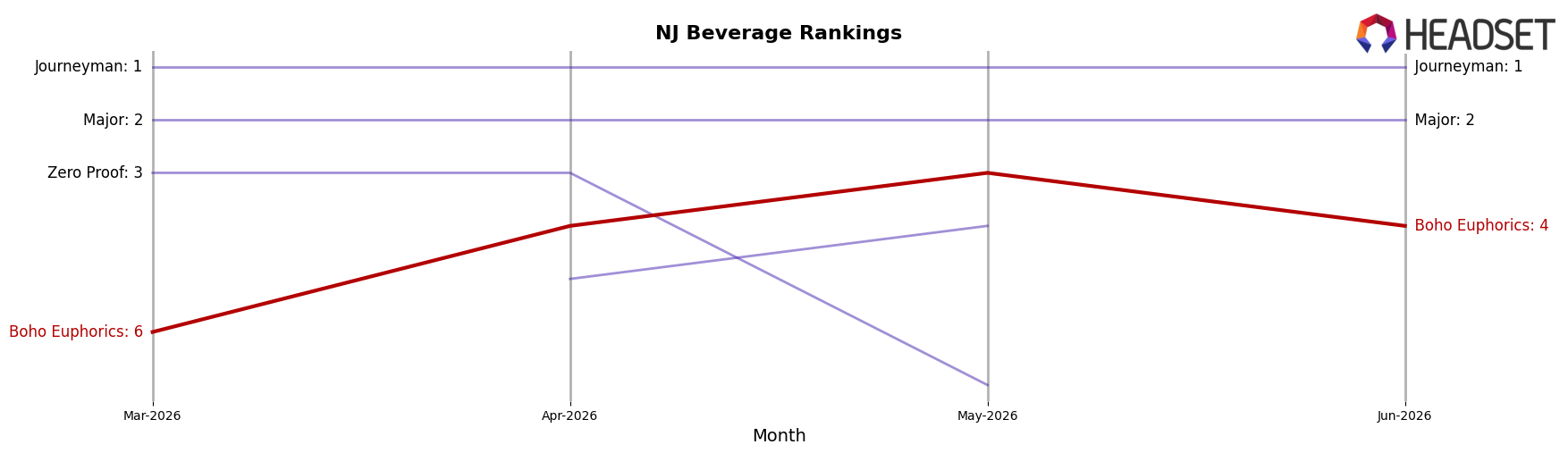

Boho Euphorics sits at rank #4 in New Jersey Beverage for June 2026, up two positions from #6 in March 2026, while its peak at #3 in May 2026 represents a one-rank retreat month over month; in the same window, Journeyman holds #1 after climbing from #2 year over year and posting 332.5% YoY sales growth, whereas Major slipped from #1 to #2 with an 11.2% YoY sales decline. With Select advancing from #4 to #3 on 80.2% YoY growth and Highly (NJ) positioned at #5, the immediate competitive set tightened by two rank positions around Boho Euphorics in May–June; the pattern implies Boho Euphorics is consolidating into the upper tier but requires sustained share capture to convert a short-lived peak into a stable top‑3 berth.

Notable Products

Blueberry Infused Pre-Roll 5-Pack (2.5g) posted the steepest decline in June 2026 at -85.5% MoM while sliding to rank 9, and Lemonade (5mg THC, 12oz, 355ml) fell -54.4% at rank 6, indicating demand is rotating away from legacy pre-rolls and certain low-dose beverages. Cherry Syrup Shot (100mg THC, 5oz, 148ml) also contracted -37.8% at rank 7, whereas Blue Raspberry Syrup Shot (100mg THC, 5oz, 148ml) grew +10.1% at rank 2; with five of the top ten in the Beverage category, the mix is concentrating around syrups even as some 5mg cans retrench. Green Apple Syrup Shots (100mg THC, 5oz, 148ml) led at rank 1 with $5,429 despite no MoM baseline, and Grape Beverage (5mg THC, 12oz, 355ml) was comparatively flat at -0.9% at rank 4, suggesting potency-forward syrup shots are becoming the commercial anchor while lower-dose formats and pre-rolls face downdrafts.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.