Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

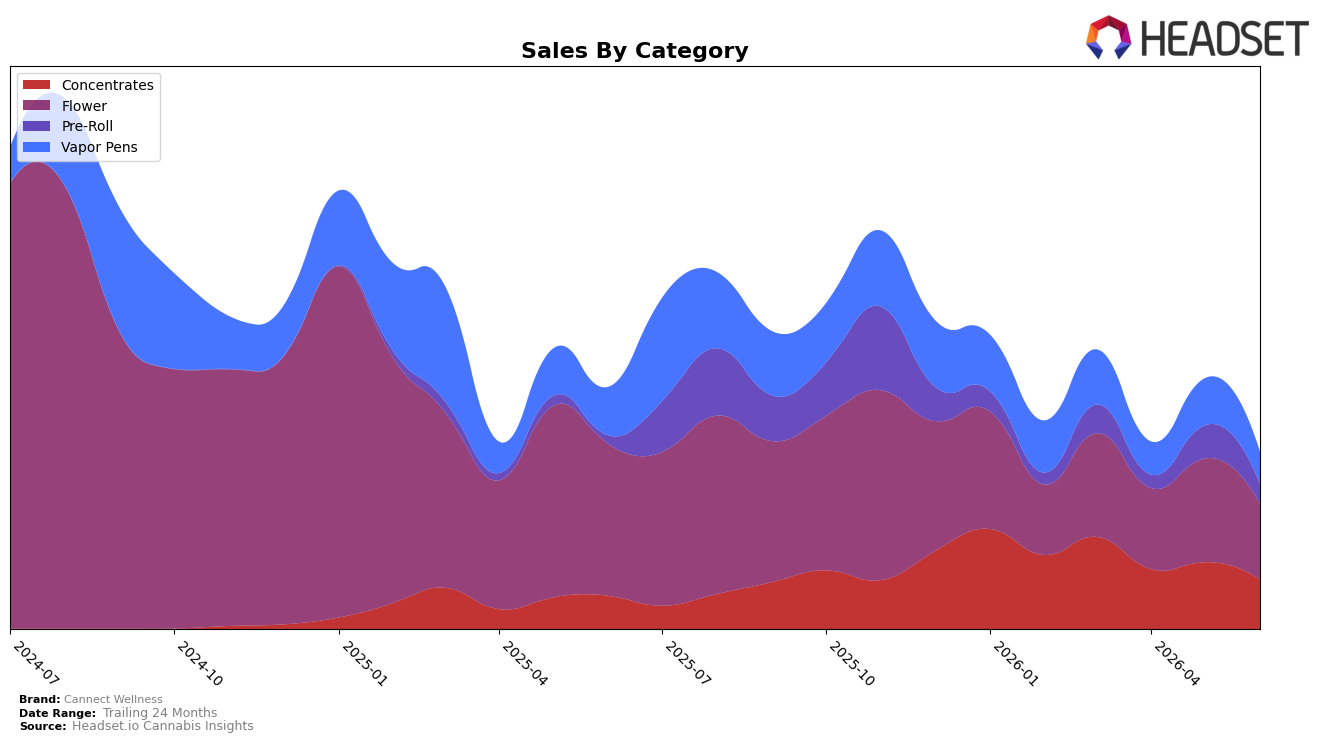

Cannect Wellness concentrated over half its June 2026 volume in Flower and Concentrates, with Flower at 42.74% share and a rank of 65 in Illinois Flower, while Concentrates reached 27.99% share; yet the splits moved sharply month over month with Flower down 27.27% MoM and Vapor Pens down 31.91% MoM. Year over year, the brand’s category polarity widened: Flower fell 50.53% YoY as Vapor Pens declined 33.77% YoY, while Concentrates grew 49.98% YoY and Pre-Roll surged 147.62% YoY; however, both growth categories still contracted MoM at 25.95% and 40.18% respectively. The implication is a pivot underway from legacy inhalables toward form factors with faster YoY traction, but near-term execution pressure is evident in the simultaneous MoM pullback across all four categories.

With average prices down 9.24% YoY to $32.88, mix-shift levers rather than price appear central to positioning: Pre-Roll’s 11.13% share and 147.62% YoY growth alongside Concentrates’ 27.99% share and 49.98% YoY growth indicate headroom to rebalance away from a Flower base that is 42.74% share yet down 50.53% YoY and ranked 65 in Illinois. The concurrent MoM declines of 27.27% in Flower and 25.95% in Concentrates, plus 31.91% in Vapor Pens and 40.18% in Pre-Roll, suggest distribution or activation gaps rather than demand isolated to one category. The thesis is that Cannect Wellness can stabilize by reallocating assortment and marketing weight toward Concentrates and Pre-Roll while selectively defending Flower in Illinois where ranking at 65 signals room for targeted improvement.

Competitive Landscape

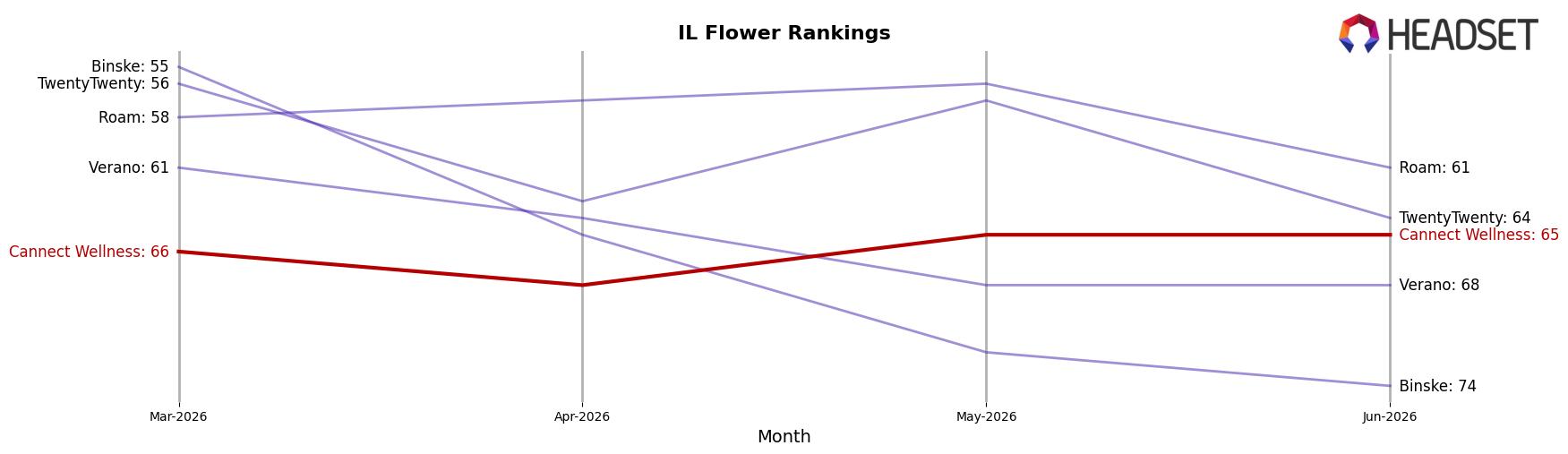

Cannect Wellness sits at rank #65 in June 2026 in IL Flower, down 8 places year over year from #57 and roughly flat versus March 2026 when it was #66; the brand remains well below its peak of #39 reached in August 2024 while category leaders moved differently, as High Supply / Supply held #1 with a 32.1% YoY sales increase and RYTHM stayed at #2 despite a -5.2% YoY change. With Good Green climbing from #4 to #3 alongside a 30.9% YoY gain and &Shine advancing from #10 to #5 with 28.5% YoY growth, Cannect Wellness’s slip from #57 to #65 while holding near #66 over three months signals stalled share recapture and suggests the brand is ceding rank to faster-advancing value and mid-tier competitors.

Notable Products

Blueberry Blintz Pre-Roll 3-Pack (3g) posted the steepest decline at -42.6% and slid to rank 8, while Cakelato Pre-Roll 3-Pack (3g) fell -38.1% to rank 6, indicating Pre-Rolls as a segment lost momentum relative to Flower. Acai Gelato x Sherb (3.5g) dipped -1.6% yet held rank 2, whereas Guillotine (3.5g) led at rank 1 with approximately $10.7k in June 2026, signaling Flower resilience despite mixed product-level shifts. Three of the top ten are Flower SKUs and three are Pre-Rolls, but the Vapor Pens duo also contracted with Juicee J Live Resin Cartridge (0.5g) down -37.4% at rank 7, concentrating risk in formats sensitive to month-to-month volatility. The pattern implies Cannect Wellness is anchored by Flower leadership while Pre-Roll and Vapor Pen softness narrows format breadth, suggesting near-term focus on stabilizing inhalables beyond core Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.