Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

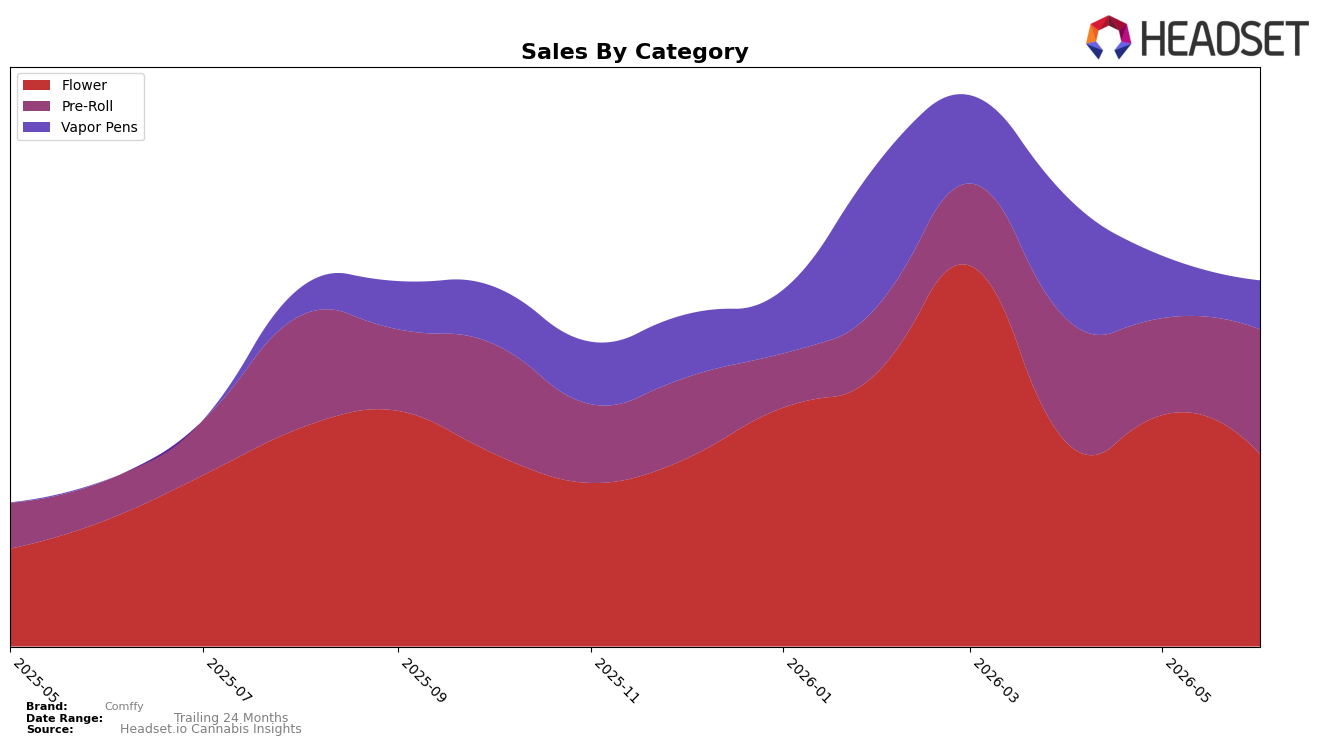

Comffy’s category mix in June 2026 concentrated 52.58% of sales in Flower with year-over-year growth of 51.48% but a month-over-month decline of 16.92%, while Pre-Roll rose to 34.10% share with 216.07% YoY growth and 28.85% MoM expansion. Vapor Pens held 13.32% share with a 21.65% MoM decline and no YoY baseline, and average price across the brand fell 10.66% YoY to $26.62. With Flower ranked 9th in the category in Connecticut and brand sales up 119.79% YoY, the mix implies volume-led gains tilted toward value and multipack dynamics rather than premium pricing power.

The shift toward Pre-Roll gaining 34.10% share alongside a 28.85% MoM increase, while Flower’s share edge at 52.58% coincides with a 16.92% MoM contraction, suggests consumer trade-offs toward convenience formats as prices eased 10.66% YoY. The 21.65% MoM pullback in Vapor Pens paired with a 9th-place Flower ranking in Connecticut indicates positioning anchored in combustion segments where brand equity can convert traffic, implying that maintaining Flower scale while leaning into Pre-Roll momentum is the clearest path to sustained share despite volatility in inhalable hardware.

Competitive Landscape

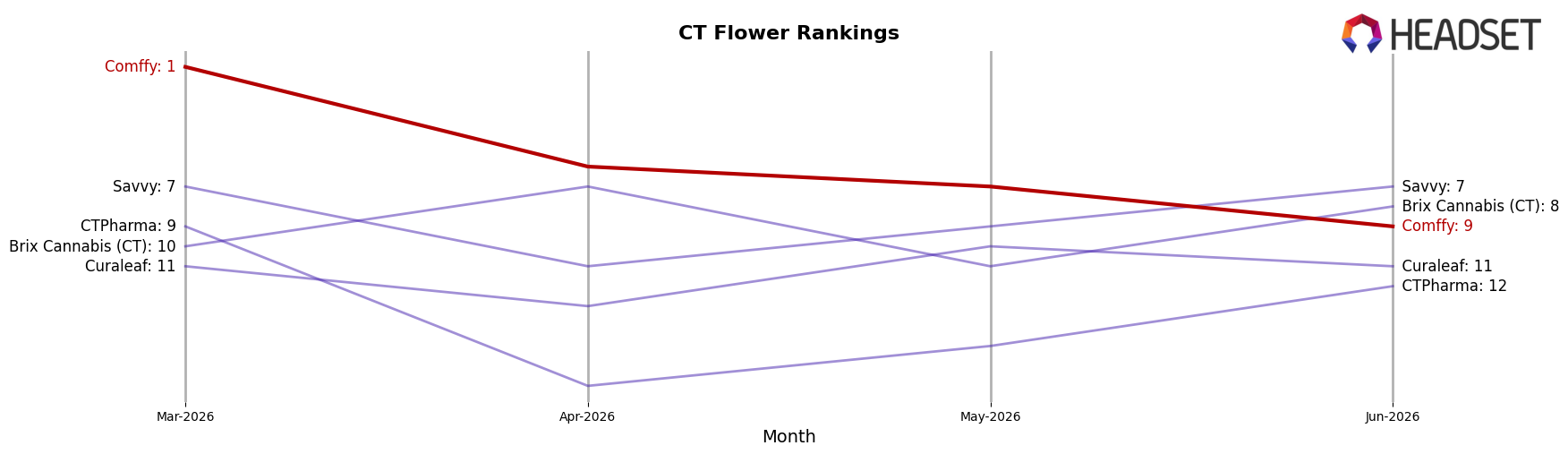

Comffy sits at #9 in CT Flower in June 2026, improving 2 ranks year over year from #11, but falling 8 positions since March 2026 when it peaked at #1 and slipping 8 ranks versus March 2026’s peak to land at #9; meanwhile, Theraplant climbed from #5 to #1 year over year while expanding sales by 69.17%, and Find. advanced from #9 to #4 alongside an 86.85% sales gain, indicating that Comffy’s late-spring drop from #1 in March 2026 to #9 in June 2026 reflects a share reallocation toward faster-advancing leaders and implies Comffy must convert its early-2026 spike into steadier mid-year retention.

Notable Products

Super Chill (3.5g) delivered the sharpest movement in June 2026 with a +50.1% MoM surge to rank 1, while Date Night (3.5g) slid -20.6% to rank 5; this divergence, coupled with Irish Goodbye (3.5g) growing +8.3% at rank 2, indicates demand is consolidating at the very top of the Flower lineup rather than lifting the entire tier. With Flower occupying 7 of the top 10 SKUs and Pre-Roll entries at ranks 3 and 8 showing either no reported MoM or a -7.6% dip, the category mix is skewing toward larger basket drivers even as some adjacent formats lag; this pattern implies Comffy is concentrating velocity into a few flagship Flower SKUs, prioritizing depth over breadth for near-term commercial gains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.