Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

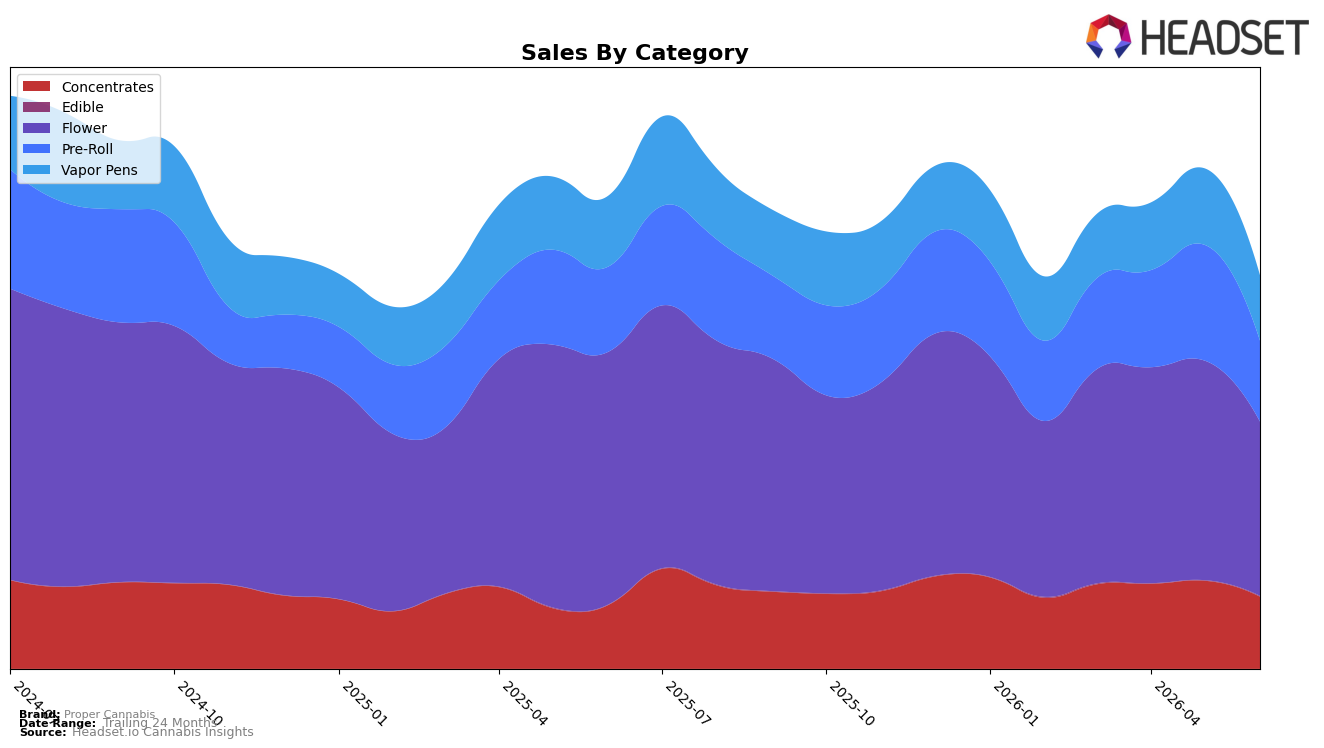

In June 2026, Proper Cannabis concentrated 44.36% of sales in Flower with a year-over-year decline of 31.07% and a month-over-month drop of 20.64%, while Pre-Roll held 20.55% share with a 5.10% YoY decline and a 30.18% MoM decline. Concentrates rose 13.16% YoY but fell 18.13% MoM to 18.34% share, and Vapor Pens, at 16.62% share, declined 7.69% YoY and 14.53% MoM. Edible remained a micro-mix at 0.13% share despite a 122.80% YoY and 65.03% MoM increase. With an average price down 10.31% YoY and overall brand sales down 16.86% YoY, the mix indicates price-led pressure in core inhalables and a partial offset from Concentrates, implying that over-reliance on Flower in Missouri is amplifying volatility as category-specific headwinds outweigh gains in smaller segments.

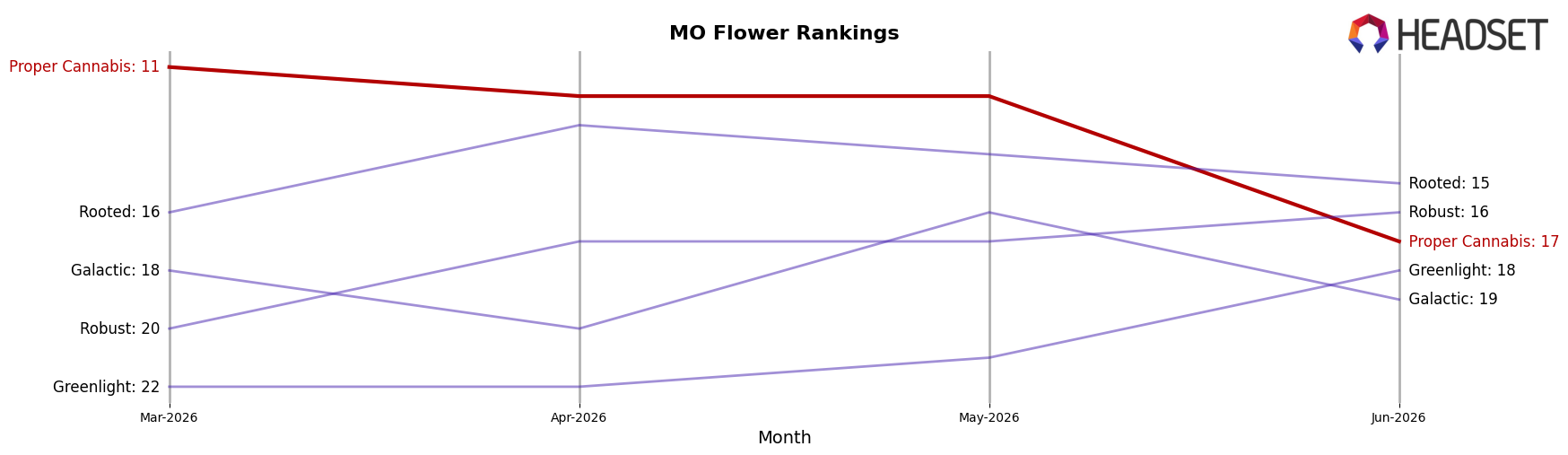

Proper Cannabis ranked 17 in Flower in Missouri, while the category’s 31.07% YoY and 20.64% MoM declines, combined with Vapor Pens’ 7.69% YoY and 14.53% MoM drops, point to a need to rebalance toward Concentrates, which grew 13.16% YoY despite an 18.13% MoM pullback. The 20.55% Pre-Roll share contracting 5.10% YoY and 30.18% MoM, alongside a brand-level 32.95% sales decline over 24 months and a 10.31% YoY price decrease, suggests margin and rank risk if Flower mix remains near 44%, implying that shifting mix points into higher-velocity Concentrates and testing Edible’s 122.80% YoY growth could stabilize month-to-month swings while creating headroom to improve price architecture.

Competitive Landscape

Proper Cannabis sits at rank #17 in June 2026, down 5 positions year over year from #12, and 6 positions below its March 2026 placement at #11, while the prior peak of #9 in June 2024 marks a two-year slide; meanwhile, Flora Farms held #1 with a 0-position YoY change as its sales fell 5.1%, and Sinse Cannabis climbed from #5 to #2 alongside a 33.2% YoY sales increase, indicating that Proper Cannabis is ceding relative share to faster risers and that its downward rank trajectory implies the need to regain velocity to avoid further mid-tier compression.

Notable Products

High Fructose Corn Syrup Pre-Roll (0.5g) posted the steepest movement in June 2026 with a -7.6% month-over-month change while sitting at rank 8, contrasting with rank 1 and rank 2 placements for Kiwi Sours Pre-Roll (0.5g) and Paris Rock Candy x Marshmallowz Pre-Roll (0.5g). Nine of the top ten SKUs are Pre-Roll items, concentrating the lineup around ranks 1–4 and 6–10 and leaving Flower represented only at rank 5. This clustering by both rank density in Pre-Roll and a single Flower anchor implies a channel strategy prioritizing breadth in Pre-Roll formats while using one higher-ticket Flower SKU to underpin basket value at approximately $47,465.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.