Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

High Heads is stocked at 11 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, Henderson, North Las Vegas, Mesquite, and Pahrump. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

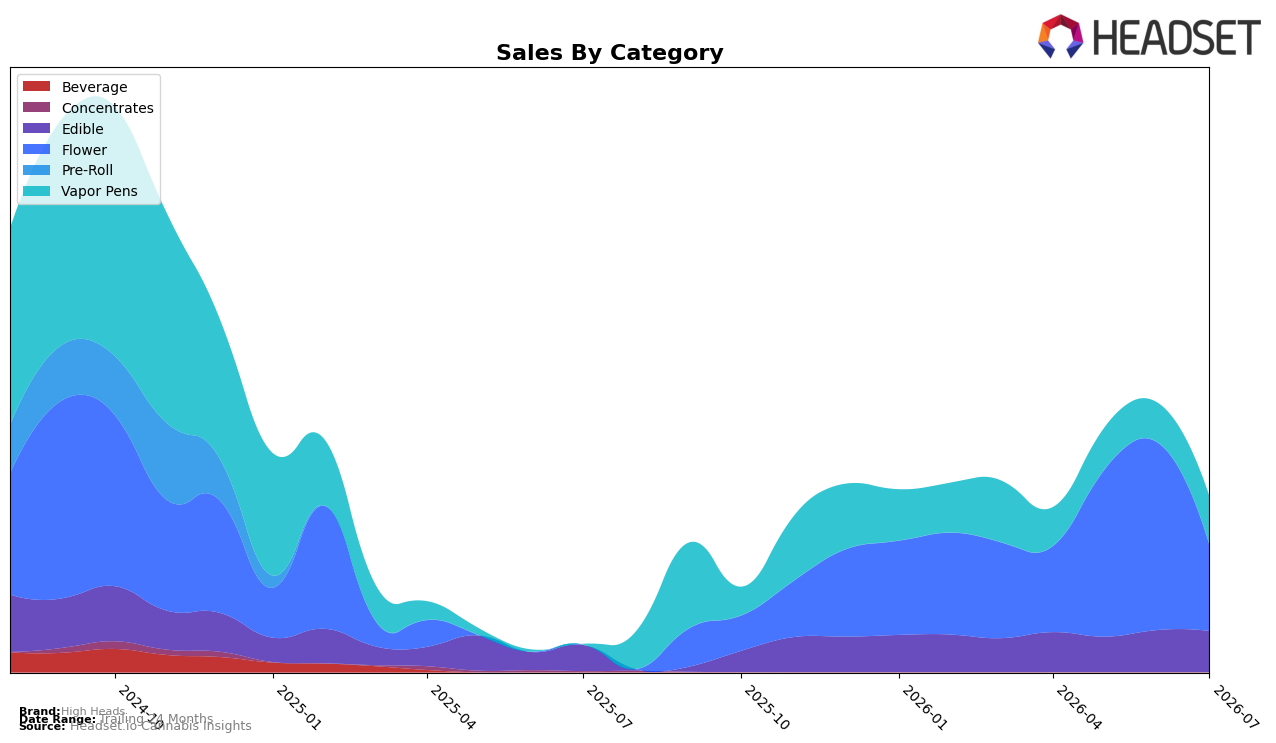

High Heads concentrated 48.96% of July 2026 sales in Flower while Vapor Pens and Edible split the remainder at 27.67% and 23.37%, respectively, and the brand held rank 30 in Flower in Nevada. Within that mix, Flower contracted month-over-month by 54.15% while Vapor Pens expanded 22.67% MoM, and Edible slipped 2.37% MoM; year-over-year, Vapor Pens surged 9,268.06% and Edible rose 58.33% YoY, with Flower lacking a YoY comp. The pattern implies a pivot away from a shrinking Flower base toward faster-growing inhalable and ingestible formats, with the July 2026 price architecture (average price up 170.06% YoY to $17.45) signaling a margin-first stance that risks ceding Flower share as the brand leans into categories showing outsized YoY momentum.

The simultaneous 54.15% MoM decline in Flower alongside a 22.67% MoM gain in Vapor Pens suggests shelf and promotional resources are being reallocated toward higher-trajectory formats, aligning with the 9,268.06% YoY Vapor Pens expansion and the brand’s 539.07% YoY sales growth. Holding rank 30 in Flower while Flower still represents 48.96% of the mix creates a positioning gap: sustaining overall growth likely requires pushing Vapor Pens beyond 27.67% share or stabilizing Flower’s MoM volatility, because a 2.37% MoM dip in Edible cannot counterbalance a majority-category contraction. The implication is that High Heads’s competitive footing will hinge on accelerating the Vapor Pens contribution while selectively defending Flower in Nevada, using price-pack architecture shaped by a 170.06% YoY average price increase to trade shoppers up without deepening the month-over-month Flower slide.

Competitive Landscape

High Heads sits at rank #30 in Nevada Flower in July 2026, down 2 positions from #28 in April 2026, with no year-over-year rank reported, and well off its peak of #12 in September 2024; meanwhile, STIIIZY leads at #1 after a +2 YoY climb with 31.5% sales growth, and FloraVega / Welleaf advanced to #5 with a +24 YoY rank jump and 299.7% sales growth, indicating that High Heads’ slide from #28 to #30 while top rivals gained rank suggests a relative share squeeze and a need to re-enter the top-20 tier to avoid further displacement.

Notable Products

The steepest decline came from CBD/THC 2:1 Citrus Sizzle Gummies 10-Pack (200mg CBD, 100mg THC), down 26.0% MoM and slipping to rank 6, while CBD/THC 1:1 Sour Cherry Blast Gummies 10-Pack (100mg CBD, 100mg THC) fell 22.9% MoM at rank 4, implying consumer fatigue for higher-CBD ratios relative to THC-balanced options. In contrast, Razzle Dazzle Gummies 10-Pack (100mg) rose 14.0% MoM to rank 1 and generated $23,355, and the CBG/CBC/THC 1:1:1 Sour Wonder Melon Gummies 10-Pack (100mg CBG, 100mg CBC, 100mg THC) climbed 36.0% MoM to rank 3, indicating momentum for multi-cannabinoid SKUs over CBD-heavy formulas. Six of the top ten are Edible SKUs concentrated in gummy formats, while new or re-entering Flower and Vapor Pens at ranks 7–10 carry no MoM baseline and trail the edible leaders, which suggests gummies remain the volume anchor as inhalables rebuild placement. The product mix points to a pivot toward diversified minor-cannabinoid gummies and away from high-CBD ratios, shaping High Heads toward breadth in functional formulations rather than a single-dominant CBD profile.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.