Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ithaca Organics Cannabis Co. is stocked at 58 licensed dispensaries across New York, with the deepest coverage in New York, Ithaca, Boerum Hill, Brooklyn, and Queens. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

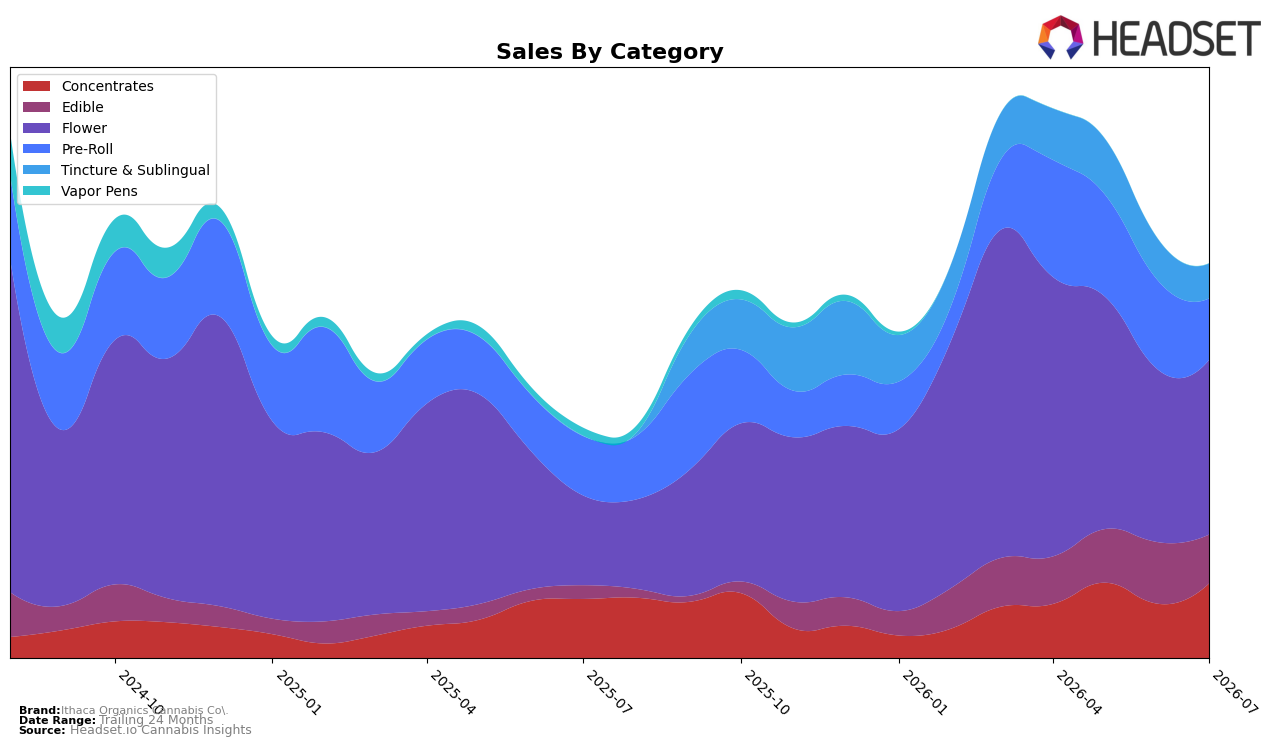

In July 2026, Ithaca Organics Cannabis Co. concentrated 44.35% of sales in Flower while holding rank 83 in Flower within New York, with category sales up 94.78% year over year but only 1.12% month over month; this split indicates the core is expanding faster annually than it is comping intra-month. Concentrates accounted for 18.93% share with 26.29% YoY growth and a 37.40% MoM surge, whereas Pre-Roll at 15.57% share grew 3.62% YoY but fell 31.14% MoM; combined with Edible at 12.35% share posting 261.63% YoY yet dropping 20.75% MoM, and Tincture & Sublingual at 8.81% share declining 16.38% MoM, the month-level volatility contrasts with a 71.91% brand-level YoY lift and an 18.62% average price increase to $31.55, implying mix is tilting toward higher-priced units even as several formats retrench month to month.

The pattern suggests positioning anchored in Flower but increasingly leveraged by higher-velocity Concentrates and episodic Edible spikes: Flower’s 94.78% YoY alongside rank 83 in New York sets a volume base, while the 37.40% MoM rise in Concentrates and the 261.63% YoY in Edible counterbalance a 31.14% MoM Pre-Roll dip and a 16.38% MoM decline in Tincture & Sublingual. With brand sales up 71.91% YoY and an 18.62% YoY price lift, the mix points to a trade-up dynamic where premium-priced Flower and Concentrates can carry near-term rank improvement if Edible volatility is harnessed and Pre-Roll exposure is right-sized.

Competitive Landscape

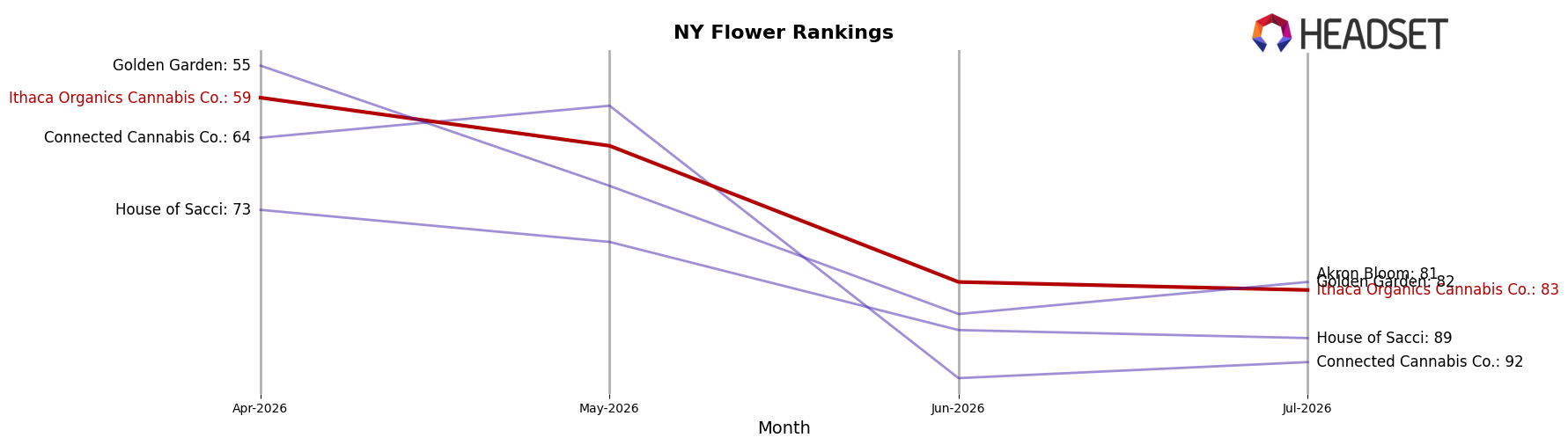

Ithaca Organics Cannabis Co. sits at rank #83 in NY Flower for July 2026, improving 29 positions from #112 year over year, but slipping 24 places from #59 in April 2026 and far below its #32 peak in August 2024; in contrast, Find. advanced from #8 to #1 while Grassroots moved up from #15 to #5 alongside a 79.75% YoY sales gain, indicating that Ithaca Organics Cannabis Co.’s upward YoY rank gain is not translating into near-term momentum against leaders who are consolidating top-5 positions.

Notable Products

White Runtz Pre-Roll (1g) delivered the largest month-over-month surge at +78.3% to rank 1, while Peach Maraschino Pre-Roll (1g) fell -21.6% to rank 2, indicating share is consolidating at the top of the Pre-Roll list. Lilac Diesel GMO Pre-Roll (1g) slid -50.0% to rank 8 as Guava Runtz Hash Infused Pre-Roll 2-Pack (1.5g) declined -25.2% to rank 10, and five of the top ten are Pre-Roll SKUs, concentrating demand in one format despite mixed trajectories. Tart Cherry Full Spectrum Rosin Gummies 10-Pack (100mg) dropped -24.4% at rank 3, while Flower entries Divine Lime (3.5g) and Ithaca OG (3.5g) held ranks 4 and 6 with no reported month-over-month change and a combined $24,480, pointing to steadier base volume outside Edibles. The pattern implies Ithaca Organics Cannabis Co. is leaning into Pre-Rolls for velocity while Flower anchors stability, with Edibles requiring repositioning to prevent further share dilution.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.