Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

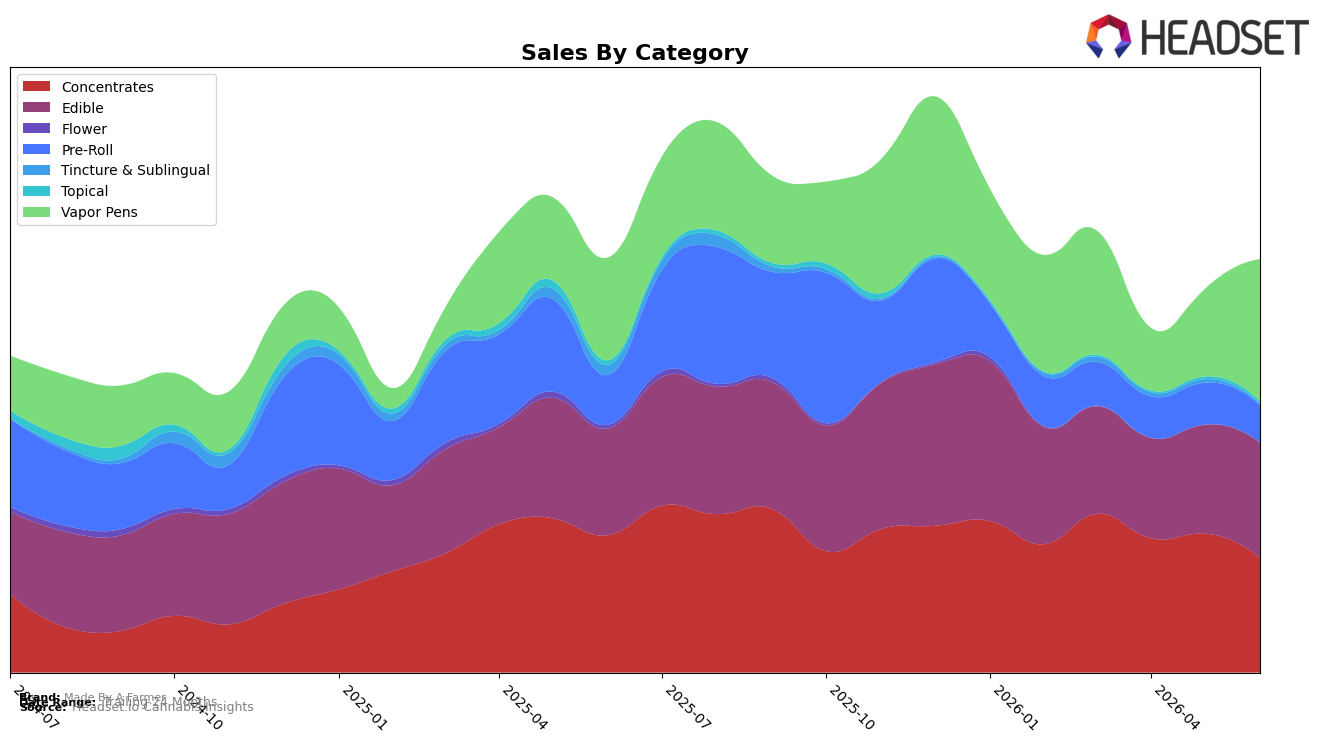

In June 2026, Made By A Farmer’s mix tilted toward Vapor Pens at 34.41% share with year-over-year growth of 38.31% and month-over-month growth of 62.70%, while Edible held 27.93% share with 8.07% YoY and 5.92% MoM increases. In contrast, Concentrates at 27.77% share declined 16.66% YoY and 17.47% MoM, and Pre-Roll at 9.04% share fell 24.90% YoY and 10.62% MoM. The net effect is a rotation from Concentrates and Pre-Roll into Vapor Pens and Edible, implying the brand is concentrating volume into faster-growing formats despite a June 2026 brand-wide YoY sales decline of 41.18%.

The pivot into Vapor Pens aligns with the brand’s rank of 67 in Vapor Pens in Michigan, but the 12.90% YoY drop in average price alongside a 62.70% MoM surge in Vapor Pen sales indicates that price compression is being used to gain share quickly within a single, scalable lane. Meanwhile, double-digit contractions in Concentrates (−16.66% YoY) and Pre-Roll (−24.90% YoY) suggest de-prioritization of higher-variance or slower-converting segments, positioning Made By A Farmer to compete on velocity and basket conversion in value-sensitive formats rather than distributing effort evenly across declining categories.

Competitive Landscape

Made By A Farmer sits at rank 67 in MI Vapor Pens for June 2026, improving 18 positions from rank 85 year over year, while slipping 3 spots from rank 70 in March 2026; the brand also remains 4 places below its peak rank 63 from December 2025. Against the competitive set, MKX Oil Company advanced from rank 3 to rank 1 with sales up 68.3% year over year, and Mitten Extracts moved down from rank 1 to rank 2 with a 20.1% YoY sales decline, indicating that Made By A Farmer’s modest rank recovery is occurring amid a reshuffle at the very top. The pattern implies Made By A Farmer’s trajectory is stabilizing upward on a yearly basis but remains vulnerable to quarter-to-quarter slippage unless it converts incremental rank gains into sustained share capture.

Notable Products

Blueberry Fast Acting Gummies 10-Pack (200mg) posted the steepest move in June 2026 with a -24.1% month-over-month decline while falling to rank 3, as Lemon Gelato Bubble Hash Infused Pre-Roll 3-Pack (1.5g) also slid -20.8% at rank 10, signaling that volatility is concentrated outside the top two seats. In contrast, THC/CBN 1:1 Grape Full Spectrum Nano Vegan Gummies 10-Pack (200mg THC, 200mg CBN) rose +26.8% to hold rank 1 and the CBD/THC 1:1 Strawberry Kiwi Full Spectrum Nano Vegan Full Spectrum Gummies 10-Pack (200mg CBD, 200mg THC) climbed +28.6% at rank 2, with both outpacing Green Apple Fast Acting Gummies 10-Pack (200mg) at +29.2% from rank 6 on a smaller base near $2.6k. Eight of the top ten SKUs are Edibles, concentrating share in functional ratio gummies even as one fast-acting variant retreats and a hash rosin newcomer sits at rank 4 without a trend line. The pattern implies Made By A Farmer is pivoting toward ratio-led Edibles dominance while trimming exposure to underperforming fast-acting lines and deprioritizing Pre-Roll momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.