Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Monopoly Melts is stocked at 298 licensed dispensaries across Michigan, Missouri, and 2 other states, 145 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Monroe, Lansing, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

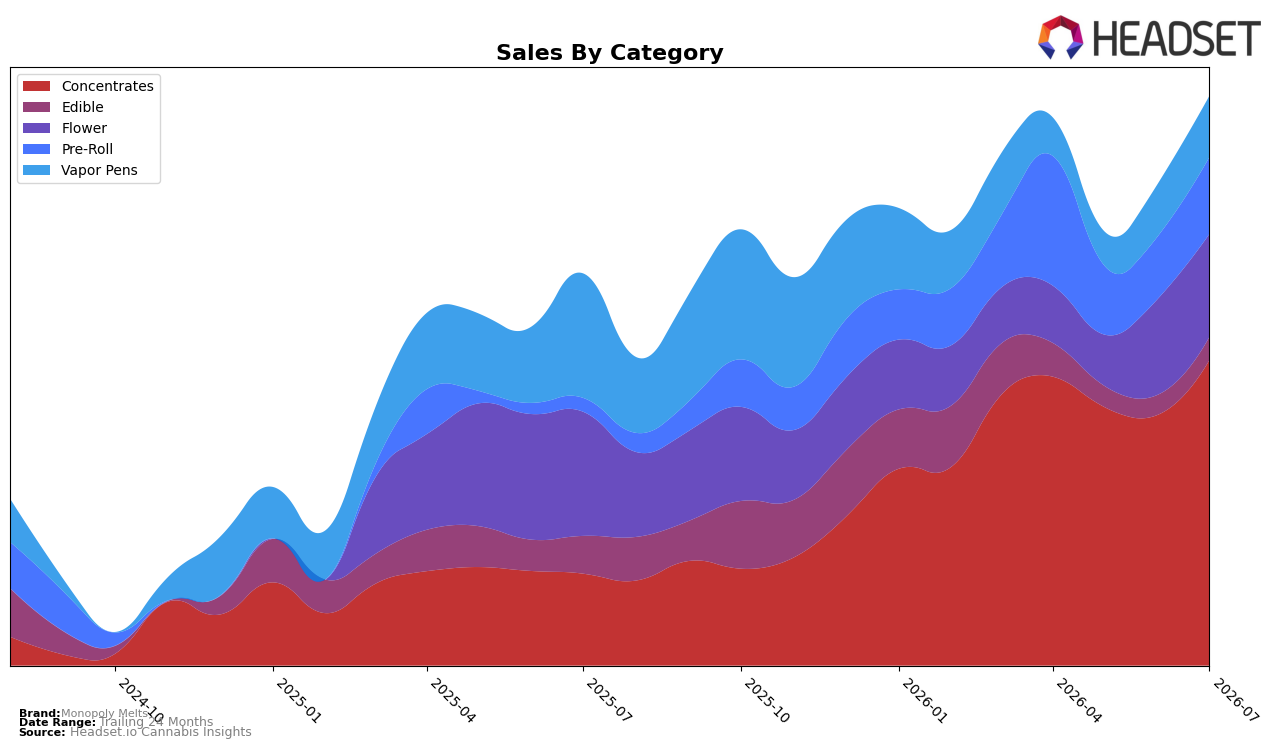

Monopoly Melts concentrated its July 2026 mix around Concentrates at 53.70% share with 233.02% year-over-year growth and 21.80% month-over-month, while Pre-Roll climbed to 13.48% share on 464.81% YoY and 22.95% MoM. In contrast, Flower held 18.05% share with -17.13% YoY and 7.22% MoM, and Vapor Pens at 10.72% share posted -50.94% YoY despite 16.52% MoM; Edible remained 4.04% share with -38.73% YoY and 16.13% MoM. With Concentrates ranked 18 in Michigan, the double-digit MoM across four categories paired with sharply positive YoY in Concentrates and Pre-Roll implies a portfolio skew that is pulling mix toward solventless or hash-driven formats while de-emphasizing inhalable oil and legacy Flower.

The combination of 233.02% YoY in Concentrates and 464.81% YoY in Pre-Roll, alongside -50.94% YoY in Vapor Pens and -17.13% YoY in Flower, signals a demand migration toward higher-terpene formats and infused form factors, supported by a 21.80% MoM in Concentrates and 22.95% MoM in Pre-Roll. Given the 18 position in Concentrates within Michigan and an average price contraction of 26.74% YoY to $32.35, the mix shift likely reflects a deliberate price-to-velocity trade: expanding access in core hash SKUs to win share while using Pre-Roll as an on-ramp, which positions Monopoly Melts to capture incremental trips even if unit economics lean more on volume than margin.

Competitive Landscape

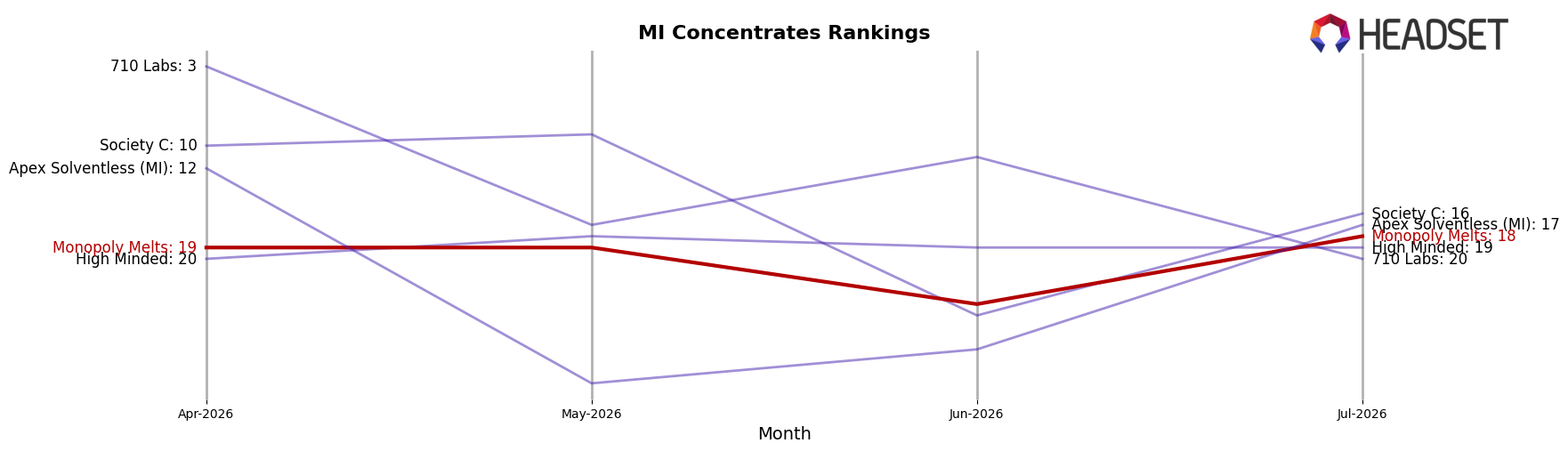

Monopoly Melts sits at rank #18 in Michigan Concentrates, improving 94 positions year over year from #112 to #18, while inching up 1 spot from #19 in April 2026 to #18 in July 2026; in the same period, Rkive Cannabis advanced from #5 to #1 with a 150.2% YoY sales lift and Uniq Pressure vaulted from #145 to #3 with 9,866.4% YoY sales growth, indicating that Monopoly Melts’ rank gains are occurring amid faster-moving rivals at the very top. With a peak position of #18 in July 2026 and competitors like The Limit sliding from #1 to #2 on a -1.7% YoY sales change while Cannalicious Labs moved from #2 to #5 on a -29.6% YoY sales change, the brand’s trajectory implies stabilization just inside the top 20 rather than a near-term leap into the top 10.

Notable Products

Lemon Cherry Papaya Pre-Roll (1g) posted the standout movement in July 2026 with a +101.8% month-over-month surge, while Grape Sherb (3.5g) climbed +67.2% to rank 5. In contrast, Dark Rainbow Live Rosin (1g) fell -21.4% to rank 6 and Super Sherb Live Rosin (1g) declined -22.3% at rank 9, indicating volatility within top-10 Concentrates. With four of the top ten belonging to Concentrates but only Flower SKUs showing large positive MoM gains and the month’s highest single-SKU revenue sitting at $48,705 for Lemon Cherry Papaya Live Rosin (1g) at rank 1, the mix points to a near-term shift toward Flower and Pre-Roll momentum even as flagship Concentrates retain headline scale.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.