Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Plume Cannabis (MO) is stocked at 75 licensed dispensaries across Missouri, with the deepest coverage in KCMO, St. Louis, Columbia, Independence, and Kansas City. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

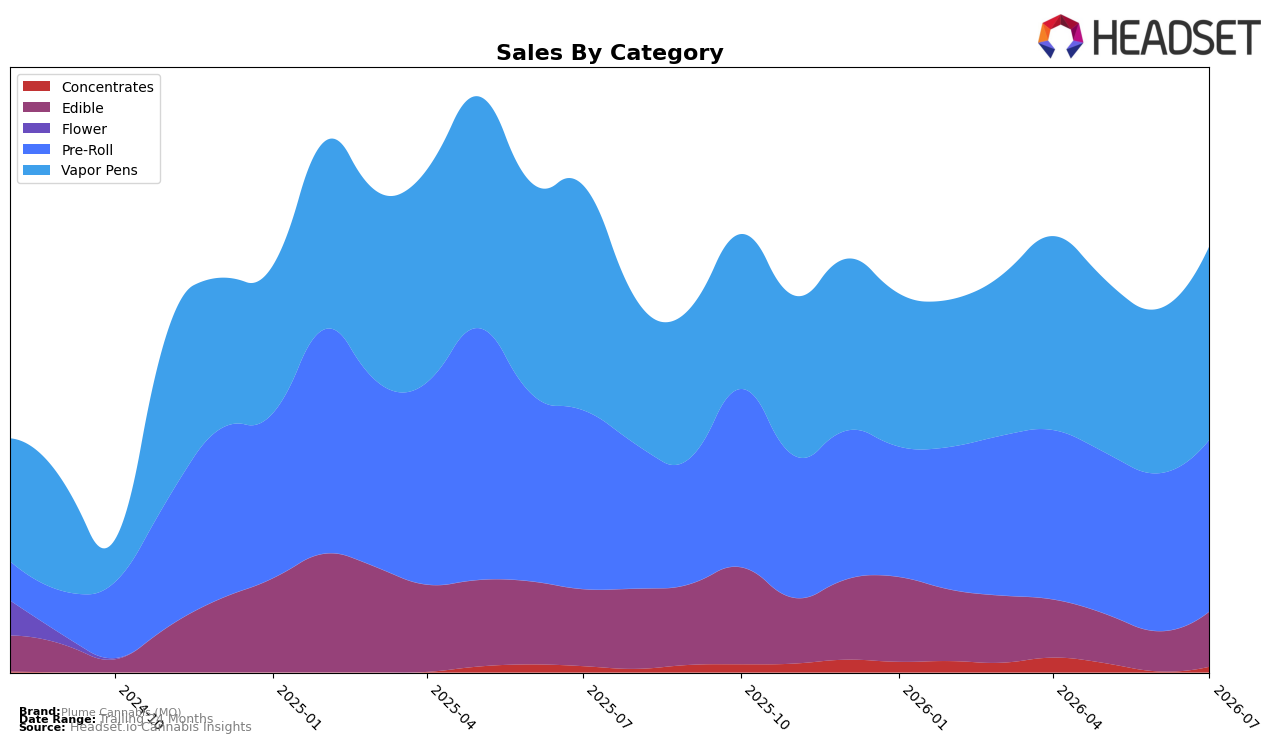

In July 2026, Plume Cannabis (MO) concentrated 45.46% of sales in Vapor Pens and 40.32% in Pre-Roll, with Edible at 12.89% and Concentrates at 1.33%, forming a two-category core. Year over year, Vapor Pens declined 13.93% while Pre-Roll slipped 3.93%, yet month over month both expanded, up 17.77% and 8.92% respectively; Edible contracted 28.44% YoY but surged 37.63% MoM, and Concentrates fell 8.85% YoY while spiking 467.68% MoM from a low base. With brand sales down 12.48% YoY and average price up 4.48% to $24.41, the pattern implies July 2026 momentum is driven by short-term recovery in core inhalables and opportunistic lift in smaller formats, rather than broad-based YoY strength.

The mix shift suggests positioning is tilting back toward higher-ticket inhalables: Vapor Pens, with a $41.52 average price, gained share via a 17.77% MoM rise as Pre-Roll at $19.41 grew 8.92% MoM, while Edible at $14.49 rebounded 37.63% MoM without offsetting its 28.44% YoY decline. Concentrates’ 467.68% MoM spike from 1.33% share indicates a testable niche rather than a scale driver, and the Vapor Pens rank at 30 in Missouri frames headroom within the top category mix. Together, these shifts imply that near-term gains will most efficiently come from reinforcing Vapor Pens while stabilizing Pre-Roll churn, using Edible for incremental basket reach and treating Concentrates as a targeted upsell rather than a volume lever.

Competitive Landscape

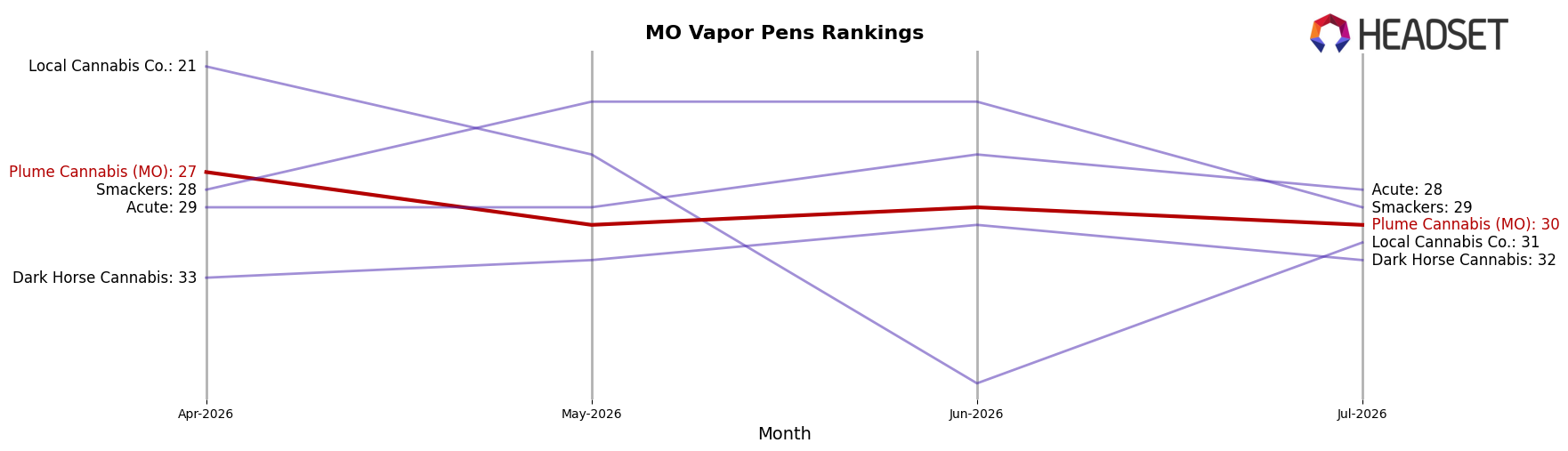

Plume Cannabis (MO) sits at rank #30 in MO Vapor Pens in July 2026, down 6 positions from #24 year over year and 3 spots from #27 in April 2026, while its historical peak was #24 in July 2025; in contrast, Galactic climbed from #5 to #2 and Good Day Farm moved from #8 to #3 as their sales grew 51.4% and 61.8% YoY, respectively, indicating share consolidation at the top as Plume Cannabis (MO) slips deeper into the 20s-to-30s tier—this rank drift implies the brand is losing relative velocity in a category where leaders are accelerating.

Notable Products

Watermelon Sugar Infused Pre-Roll 5-Pack (2.5g) posted the headline move in July 2026 with +78.8% month over month and rose to rank 2, while Space Donuts Infused Pre-Roll 2-Pack (1g) fell -26.1% MoM yet still held rank 1. Blueberry Cream Infused Pre-Roll 2-Pack (1g) slipped a modest -3.3% MoM at rank 3, and Cannalope Haze Infused Pre-Roll 2-Pack (1g) gained +18.4% MoM at rank 4. Eight of the top ten are Pre-Roll SKUs, indicating a portfolio concentrated in infused joints, and the surge in the 5-Pack alongside a decline in a 2-Pack suggests a shift toward multi-pack value rather than single-occasion formats; the single notable dollar outlier is $41,876 for Watermelon Sugar in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.