May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

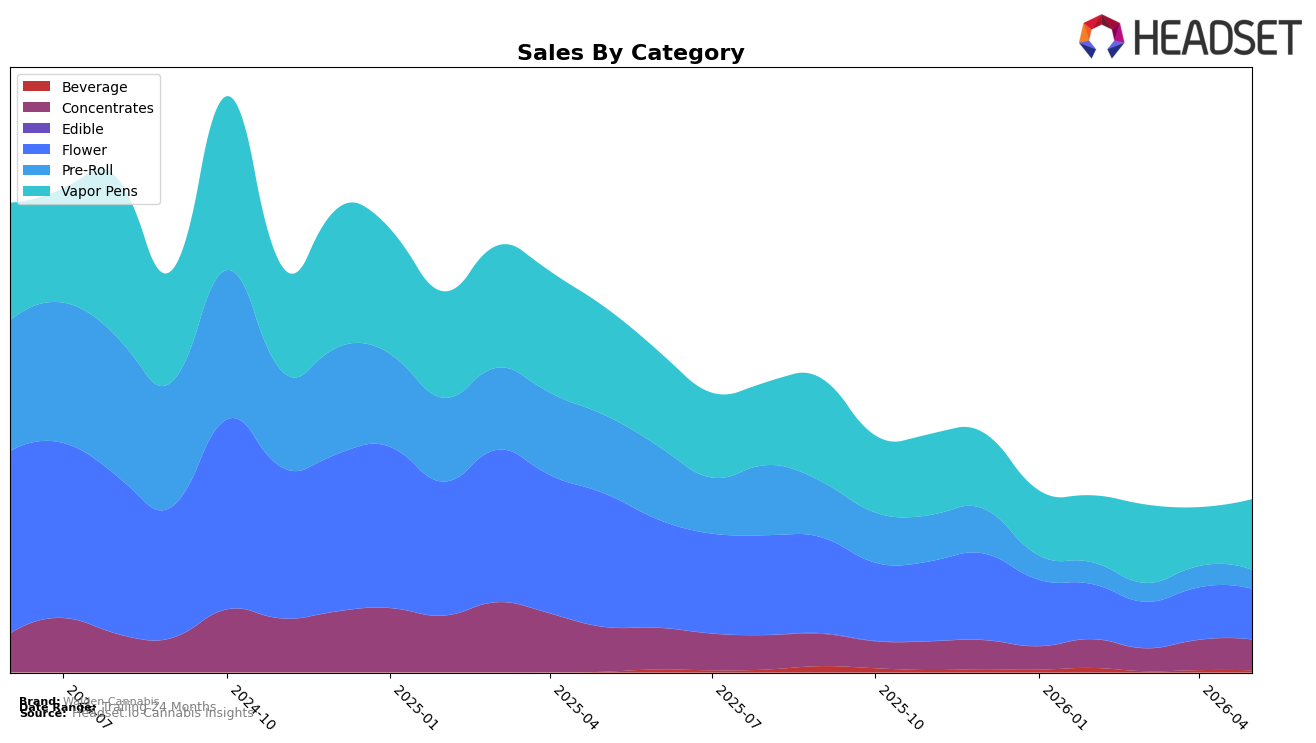

Walden Cannabis concentrated 40.82% of May 2026 sales in Vapor Pens, where month-over-month growth of 19.57% contrasted with a year-over-year decline of 35.01%, while Flower held 29.26% share with a -3.28% MoM and -62.21% YoY drop. Concentrates accounted for 17.76% share with a 1.94% MoM uptick against a -31.44% YoY decline, and Pre-Roll slipped to 10.93% share with -10.65% MoM and -75.94% YoY. Beverage remained niche at 1.23% share with -7.85% MoM despite 202.89% YoY growth, and average price across the brand fell 9.94% YoY. The pattern implies the mix is tilting back toward Vapor Pens as a near-term volume stabilizer despite broad YoY contraction, while Pre-Roll and Flower remain the principal drag on annual comps.

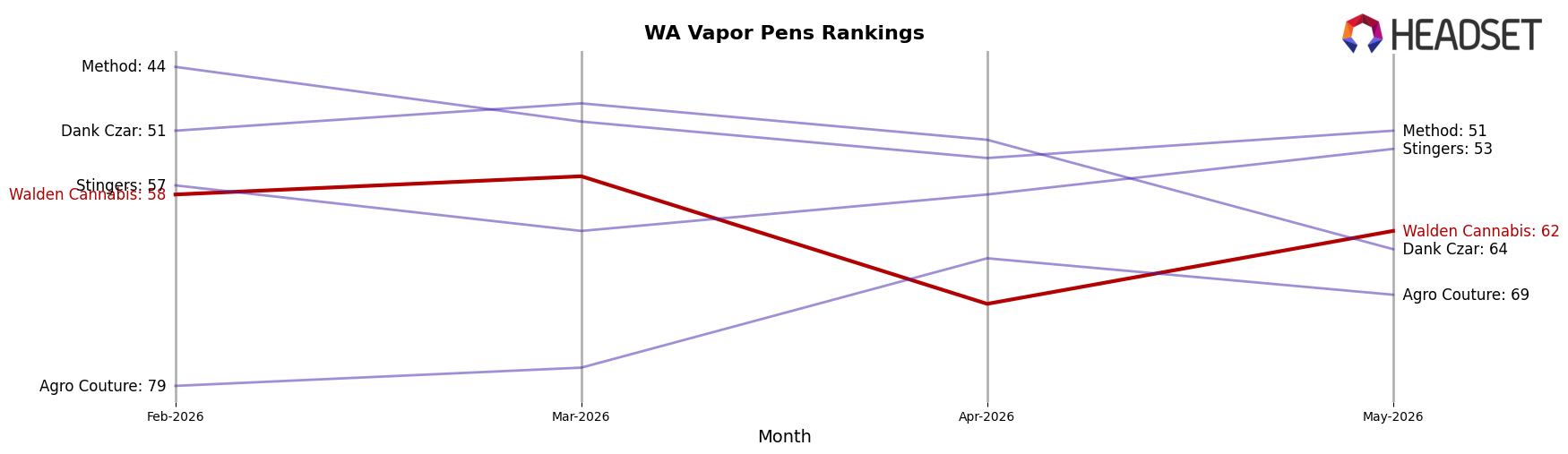

Within Washington Vapor Pens, Walden Cannabis sat at rank 62 in May 2026, signaling mid-pack visibility, and the 19.57% MoM lift in Vapor Pens versus -3.28% MoM in Flower suggests channel or assortment execution is currently favoring inhalables over traditional flower formats. The -75.94% YoY fall in Pre-Roll alongside a -31.44% YoY in Concentrates indicates the brand’s combustion-heavy segments are ceding share to cartridges, while a 202.89% YoY rise in Beverage from a 1.23% base has not yet altered positioning. The implication is that defending and selectively expanding Vapor Pens should anchor positioning while Flower and Pre-Roll require SKU rationalization or price-pack adjustments to prevent further share erosion.

Competitive Landscape

Walden Cannabis sits at rank #62 in WA Vapor Pens in May 2026, down 10 positions year over year from #52 and 4 positions lower than its #58 rank in February 2026, while also trailing its peak at #41 from August 2024; in contrast, Full Spec climbed from #5 to #3 with a 13.7% YoY sales gain and Mfused held #1 despite a 22.3% YoY sales decline, indicating Walden’s relative slippage is driven more by lost share than overall category contraction, and the trajectory implies further rank erosion unless mix or pricing resets shift momentum back toward prior top-50 positioning.

Notable Products

Grilled Peaches Wax (1g) posted the steepest decline at -12.8% month over month and slid to rank 5, while Trainwreck Distillate Cartridge (1g) fell -9.9% to rank 3, signaling pressure on legacy formats even as Granny Derkle Sugar Wax (1g) rose 12.0% to rank 1. Dutch Treat Distillate Cartridge (1g) and Purple Punch Cured Resin Cartridge (1g) each surged roughly +30% MoM to ranks 4 and 6, and five of the top eight are Vapor Pens, indicating an assortment tilt toward cartridges over concentrates despite one wax leader; this mix implies the brand is reallocating demand toward faster-moving pen SKUs. Northern Lights #5 Distillate Cartridge (1g) grew 3.4% MoM at rank 2 against Jack Herer Distillate Cartridge (1g) down -8.1% at rank 7, and the single highest-revenue item delivered $5,490 in May 2026; the contrasting momentum across pen strains implies targeted strain rotation will matter more than category shifts for sustaining share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.