Feb-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

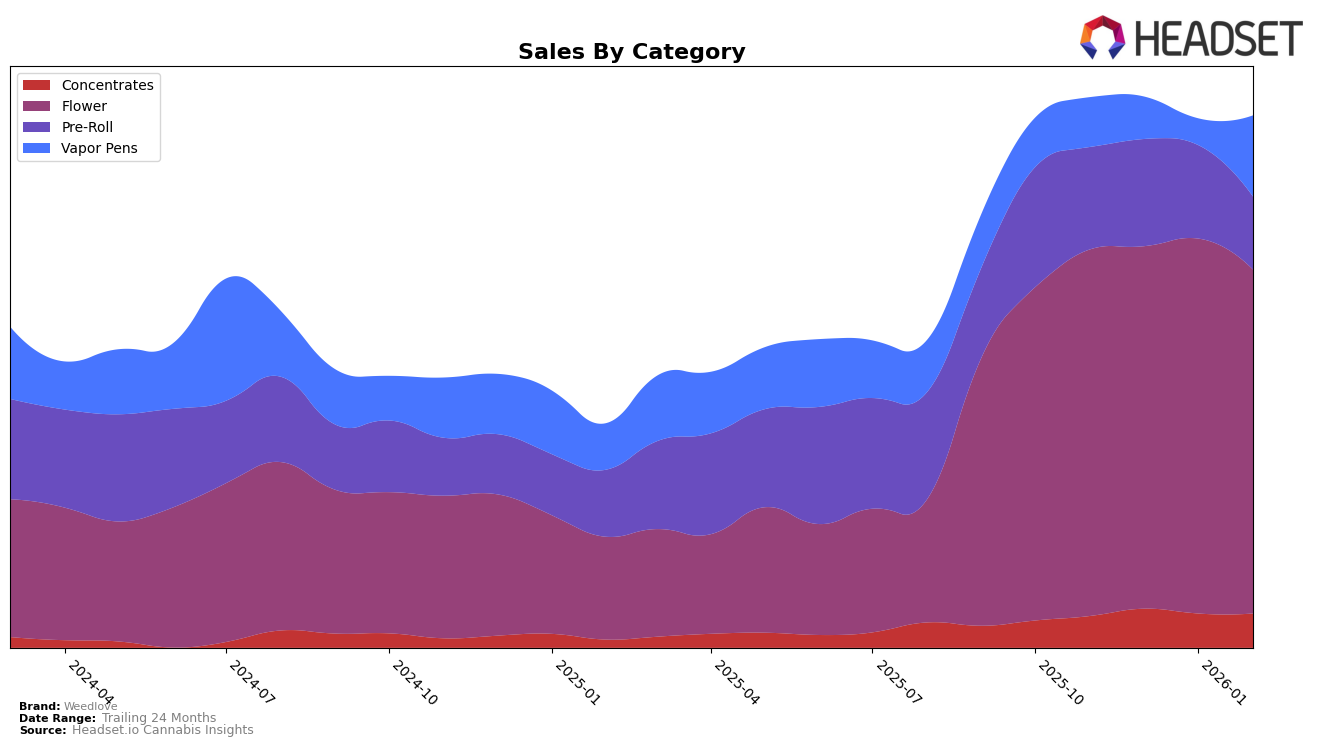

Weedlove's performance in California showcases a dynamic trajectory across various product categories. In the Concentrates category, Weedlove has demonstrated a steady climb, moving from 42nd place in November 2025 to breaking into the top 30 by February 2026. This upward movement indicates a growing consumer preference or effective market strategies in this category. Conversely, the Flower category saw a slight dip, with Weedlove dropping from 33rd to 35th place in February 2026, suggesting potential challenges in maintaining its competitive edge or shifts in consumer preferences. The Pre-Roll category presented a more pronounced decline, with the brand slipping from 56th to 61st place, reflecting a need for strategic reassessment or innovation to regain market presence.

In the Vapor Pens category, Weedlove's performance is notably volatile. The brand was not ranked in January 2026, indicating it fell out of the top 30 during that period, which could be a red flag for stakeholders. However, by February 2026, Weedlove made a significant leap to 59th place, suggesting a potential recovery or a successful marketing push. These fluctuations highlight the competitive nature of the Vapor Pens market in California and underscore the importance of agility in product offerings and marketing strategies. Overall, Weedlove's mixed performance across categories and months provides insights into both its strengths and areas for improvement in a highly dynamic market.

Competitive Landscape

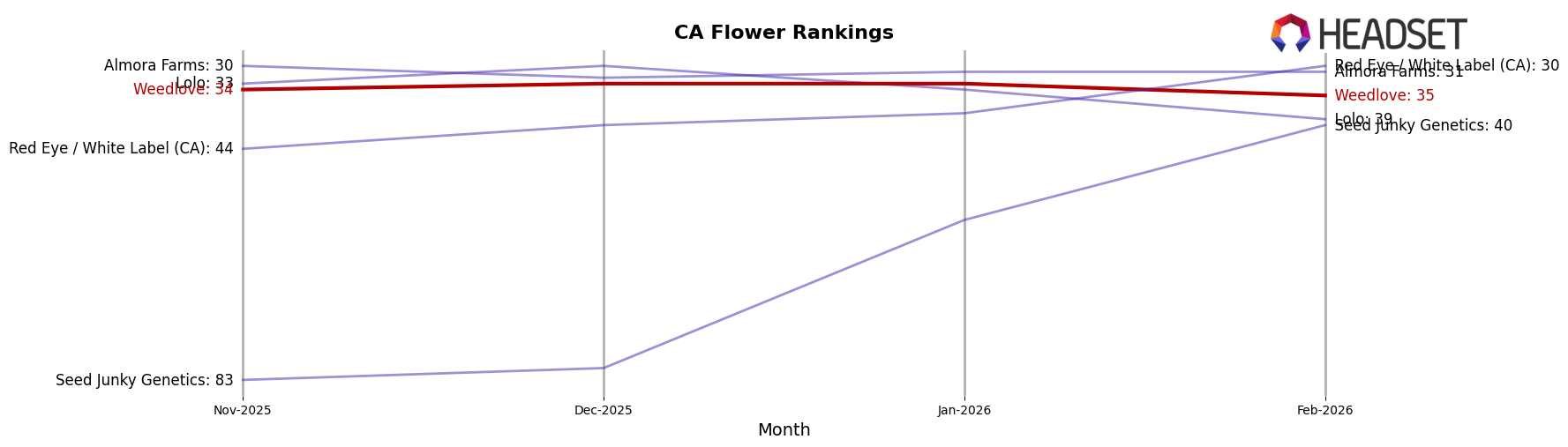

In the competitive landscape of the Flower category in California, Weedlove's performance has shown moderate consistency, maintaining a rank around the mid-30s over the past few months. Notably, Weedlove's rank slightly fluctuated from 34th in November 2025 to 35th in February 2026, indicating a relatively stable position amidst a competitive market. In contrast, Almora Farms maintained a slightly higher and more stable rank, consistently around 30th, which suggests a stronger foothold in the market. Meanwhile, Red Eye / White Label (CA) showed a significant improvement, jumping from 44th to 30th, which could indicate a potential threat to Weedlove's market share if this upward trend continues. Additionally, Seed Junky Genetics demonstrated remarkable progress, climbing from 83rd to 40th, showcasing a rapid growth trajectory that could further intensify competition. These dynamics suggest that while Weedlove maintains a steady presence, there is a need for strategic initiatives to enhance its competitive edge and prevent potential market share erosion.

```

Notable Products

In February 2026, Super Boof (14g) maintained its position as the top-selling product for Weedlove, showing consistent performance with a sales figure of 1431. Purple Milkshake (14g) secured the second spot, climbing back into the rankings after not appearing in January. Atomic Funk (14g) emerged as a new contender in third place, indicating a strong market entry. Berry Spritzer (14g) followed closely in fourth place, also making its debut in the rankings. Cosmic Cookies Infused Flower (3.5g) dropped to fifth place, showing a slight decline from its third-place position in December 2025.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.