Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

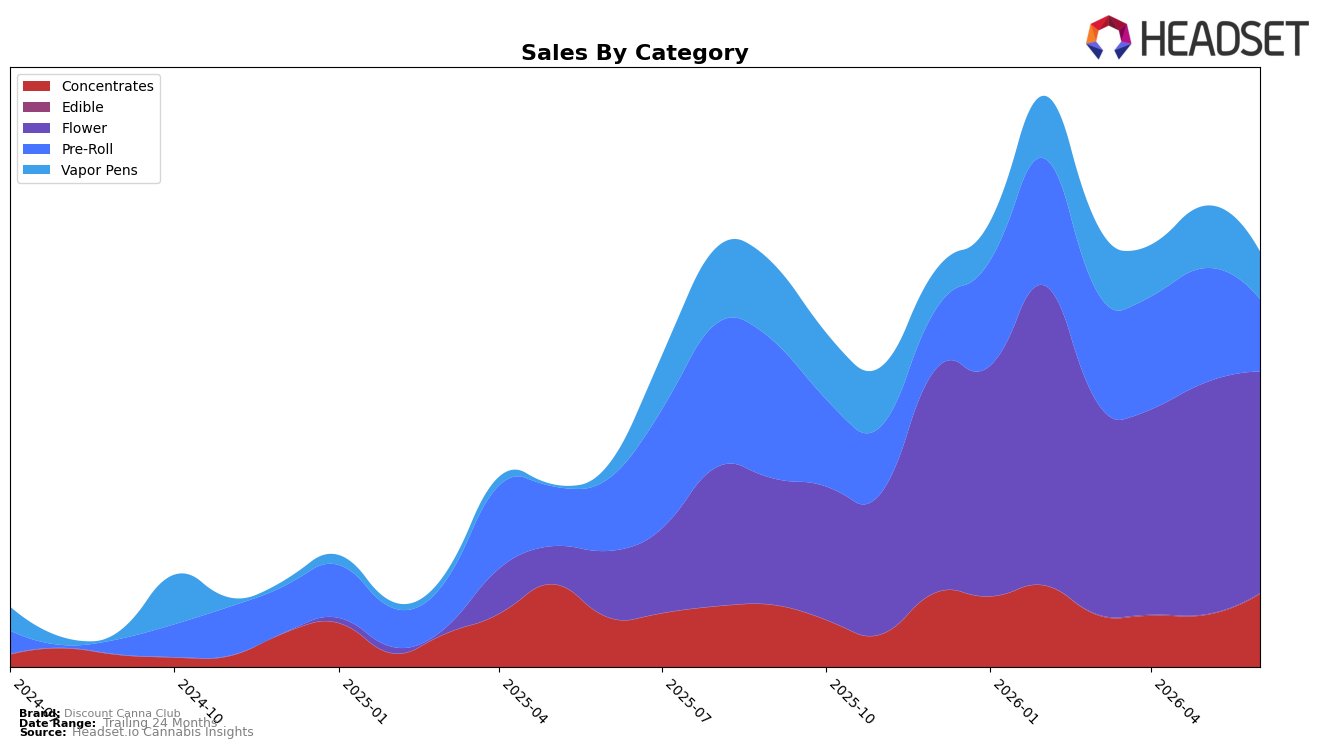

Discount Canna Club’s mix in June 2026 was led by Flower at 53.44% share with 235.02% year-over-year growth but a 4.30% month-over-month decline, while Vapor Pens held 11.44% share with 245.57% year-over-year growth and a 23.71% month-over-month drop; Pre-Roll sat at 17.42% share with 0.44% year-over-year change and a 36.95% month-over-month decline. In contrast, Concentrates reached 17.53% share with 47.86% year-over-year growth and a 41.02% month-over-month increase, and Edible, though only 0.17% share, rose 41.19% month-over-month; together, these moves imply the brand is leaning into inhalables with volatile month-over-month swings while selectively expanding higher-margin formats. Average price fell 5.31% year-over-year to $21.57 as Flower’s average price of $27.10 coexisted with a heavier mix of lower-priced Pre-Roll at $10.52, implying price laddering that supports unit velocity alongside premiumizing niches.

The category shifts suggest Discount Canna Club is prioritizing scale in Flower and Vapor Pens to drive traffic while using Concentrates’ 41.02% month-over-month rise and 17.53% share to buffer margin, implying a barbell strategy where growth relies on a high-share base and a faster-growing specialty. With June 2026 rank at 70 in Flower in Massachusetts and Pre-Roll down 36.95% month-over-month versus Concentrates up 41.02% month-over-month, the mix signals a pivot toward depth in categories where differentiation can improve rank trajectory. The combination of 106.33% brand sales year-over-year growth and a 23.71% month-over-month decline in Vapor Pens concentration suggests demand is broadening across inhalables rather than concentrating in a single format, positioning the brand to trade share between adjacent categories as price elasticity shifts.

Competitive Landscape

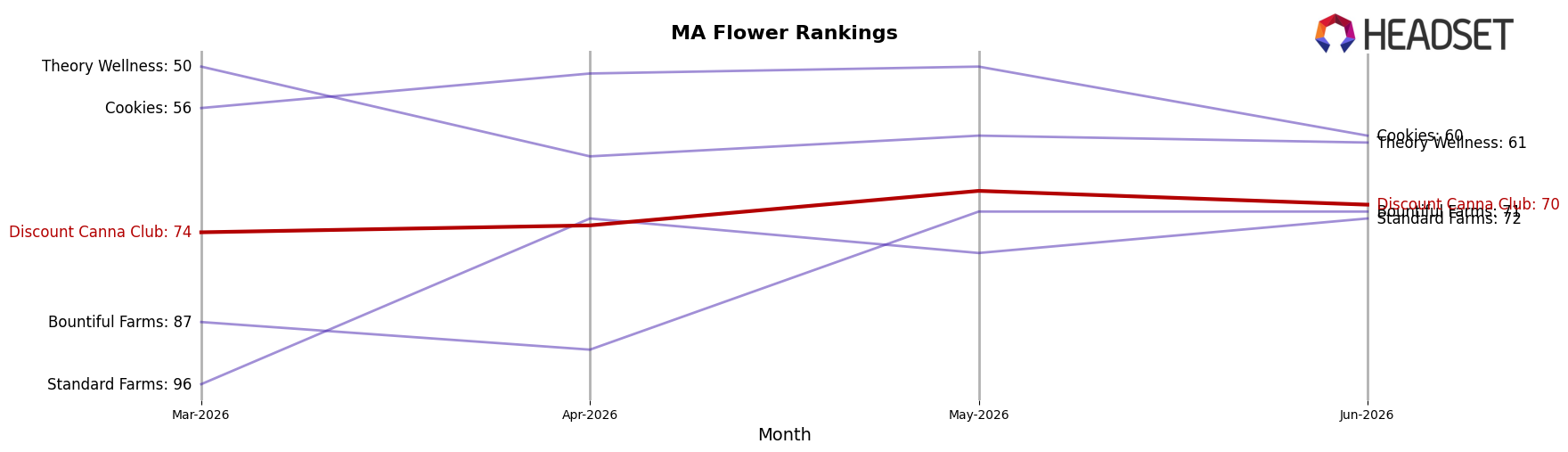

Discount Canna Club sits at rank #70 in MA Flower for June 2026, improving 57 positions year over year from #127 while slipping 4 spots since March 2026 from #74; the brand’s peak was #59 in February 2026, placing it 11 ranks above today’s position and indicating recent giveback after a longer YoY climb. Meanwhile, Farmer's Cut rose to #1 from #3 as sales grew 32.4% year over year, and Simply Herb fell to #2 from #1 with a 1.6% YoY sales decline, signaling that Discount Canna Club’s mid-pack gains are occurring while leadership is consolidating at the top. The pattern implies Discount Canna Club’s rank trajectory is improving on a 12‑month view but remains volatile quarter to quarter, suggesting that sustained share capture will require stabilizing momentum as top-tier competitors widen separation.

Notable Products

Northern Lights Diamond Infused Pre-Roll 2-Pack (1g) marks the steepest movement in June 2026 with a -35.9% month-over-month drop while sitting at rank 6, and Gaslight OG Diamond Infused Pre-Roll 2-Pack (1g) follows with a -20.3% decline at rank 4. In contrast, Acapulco Gold Diamond Infused Pre-Roll 2-Pack (1g) rose +34.9% MoM to rank 2, but the combined pattern of two double-digit declines versus one double-digit gain implies volatility concentrated within infused pre-rolls. Four of the top ten are Pre-Roll SKUs, including two infused formats and two standard pre-rolls, indicating category dependence even as Flower anchors the chart with Bananaconda (3.5g) at rank 1 and Cherrylicious (3.5g) inching up +2.2% at rank 9. The mix points to a pivot where Flower stability balances a churn-prone infused pre-roll lineup, suggesting assortment discipline will matter more than chasing short-term spikes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.