Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

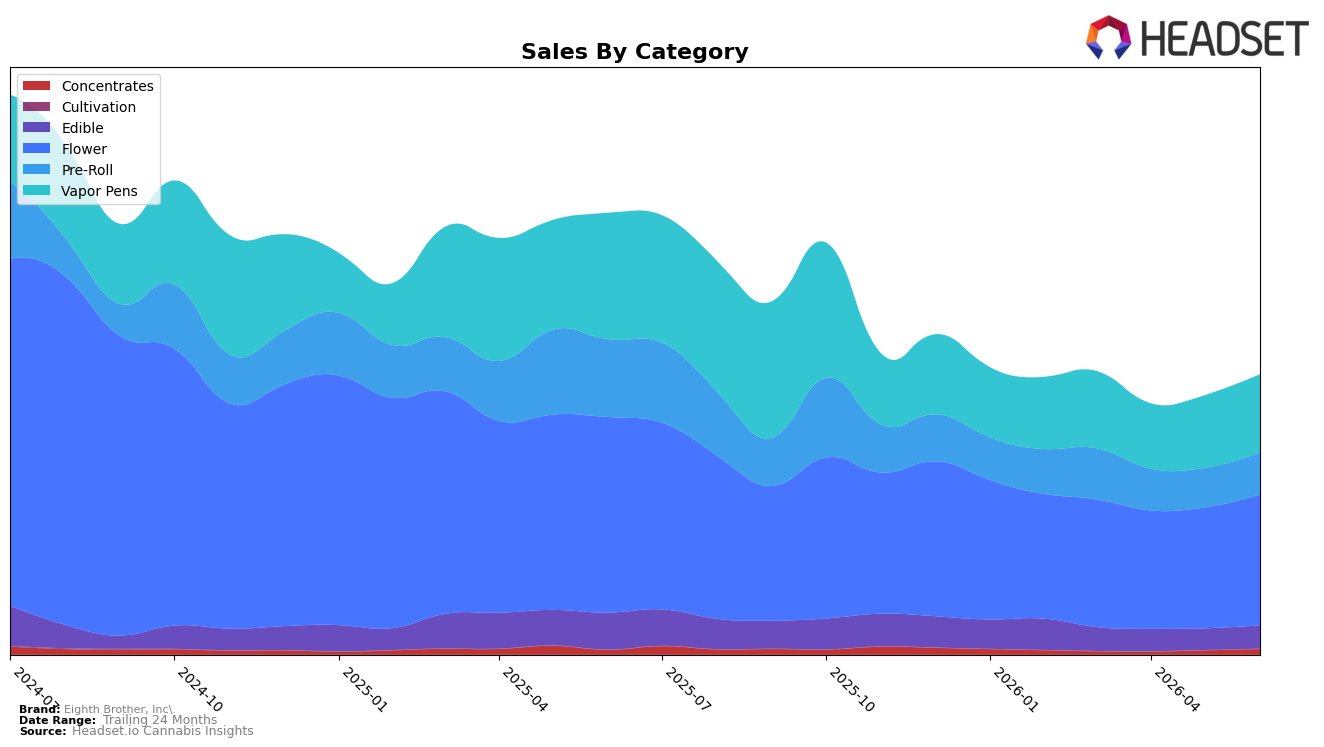

In June 2026, Eighth Brother, Inc. concentrated 46.83% of sales in Flower with year-over-year decline of 33.19% but month-over-month growth of 8.26%, while Vapor Pens held 27.93% share with a 38.29% year-over-year drop and a 7.63% month-over-month lift. Pre-Roll accounted for 14.99% share with year-over-year decline of 46.17% and month-over-month growth of 6.33%, and Edible represented 8.28% share with a 36.90% year-over-year decline and a 7.79% month-over-month increase. Concentrates is the outlier at only 1.97% share yet posted a 17.44% year-over-year increase and a 33.27% month-over-month jump; paired with an overall brand sales decline of 36.71% year-over-year and a 7.16% year-over-year rise in average price, the pattern implies mix recovery is being driven tactically by smaller segments while core categories rely on short-cycle month-over-month gains.

The shift suggests Eighth Brother, Inc. is leaning into near-term velocity rather than structural share expansion, as Flower and Vapor Pens combine for 74.76% share but both carry year-over-year declines above 33% while posting single-digit month-over-month gains between 7.63% and 8.26%. With Concentrates growing 17.44% year-over-year on a 1.97% share base and surging 33.27% month-over-month, the brand’s positioning tilts toward opportunistic niches for incremental lift rather than defending scale categories, a stance further evidenced by a rank of 28 in California Flower and an average price increase of 7.16% year-over-year that risks dampening volume in price-sensitive formats.

Competitive Landscape

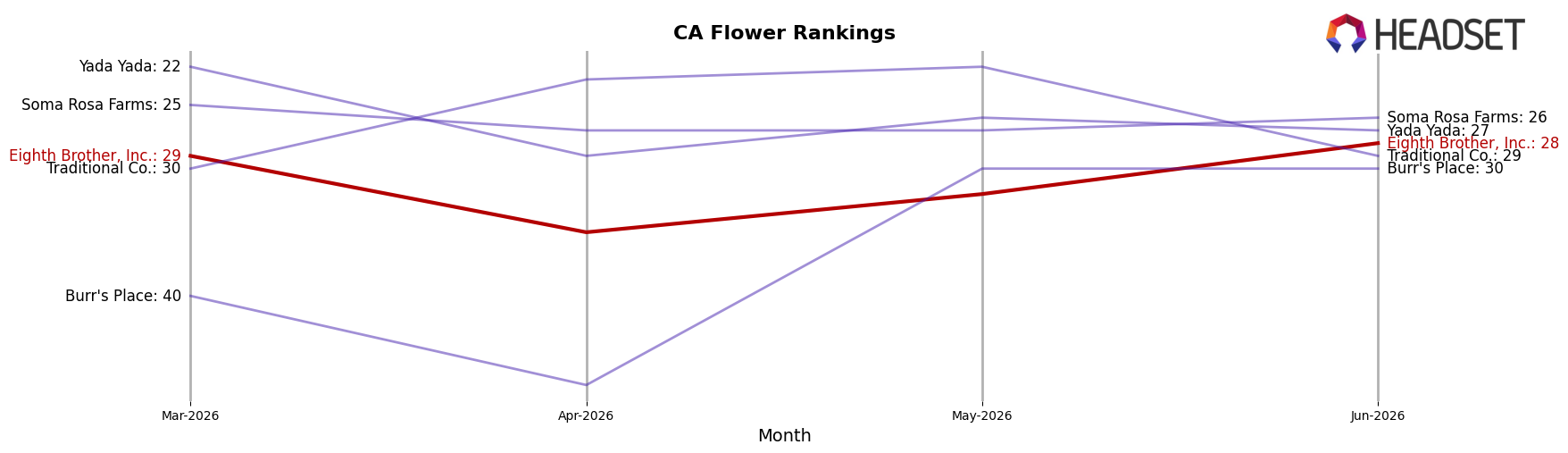

Eighth Brother, Inc. sits at rank #28 in CA Flower in June 2026, down 7 positions year over year from #21, while nudging up 1 position versus three months ago from #29, indicating a downward YoY trend amid only marginal recent stabilization. In contrast, STIIIZY advanced from #2 to #1 with 62.54% YoY sales growth, and CAM climbed from #3 to #2 with 56.23% YoY growth, whereas CannaBiotix (CBX) slipped from #1 to #3 despite a 2.38% YoY increase, showing that top-tier gains are concentrated among brands with materially higher growth rates. Given Eighth Brother, Inc.’s slide from a peak of #9 in July 2024 to #28 now and the 7-position YoY decline against competitors posting 56–63% YoY increases, the trajectory implies share erosion that will persist unless the brand re-enters the top-20 through mix or distribution changes.

Notable Products

Blue Dream Distillate Disposable (1g) fell 14.6% month over month to rank 1, while the runner-up held rank 2 with Green Crack Distillate Disposable (1g) rising 31.3%, creating a widening volatility gap at the very top. Cherry Pie Distillate Disposable (1g) advanced 34.3% at rank 5, and Blue Dream Pre-Roll (1g) slipped 1.7% at rank 3, indicating demand is rotating within overlapping strain names across formats. With four of the top ten in Pre-Roll and four in Vapor Pens, the mix concentrates in inhalables, and the contrasting -14.6% vs +31.3% swings imply Eighth Brother, Inc. is tilting toward flavor-driven pen SKUs rather than legacy Blue Dream leadership even as one pen still anchors the top rank.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.