Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

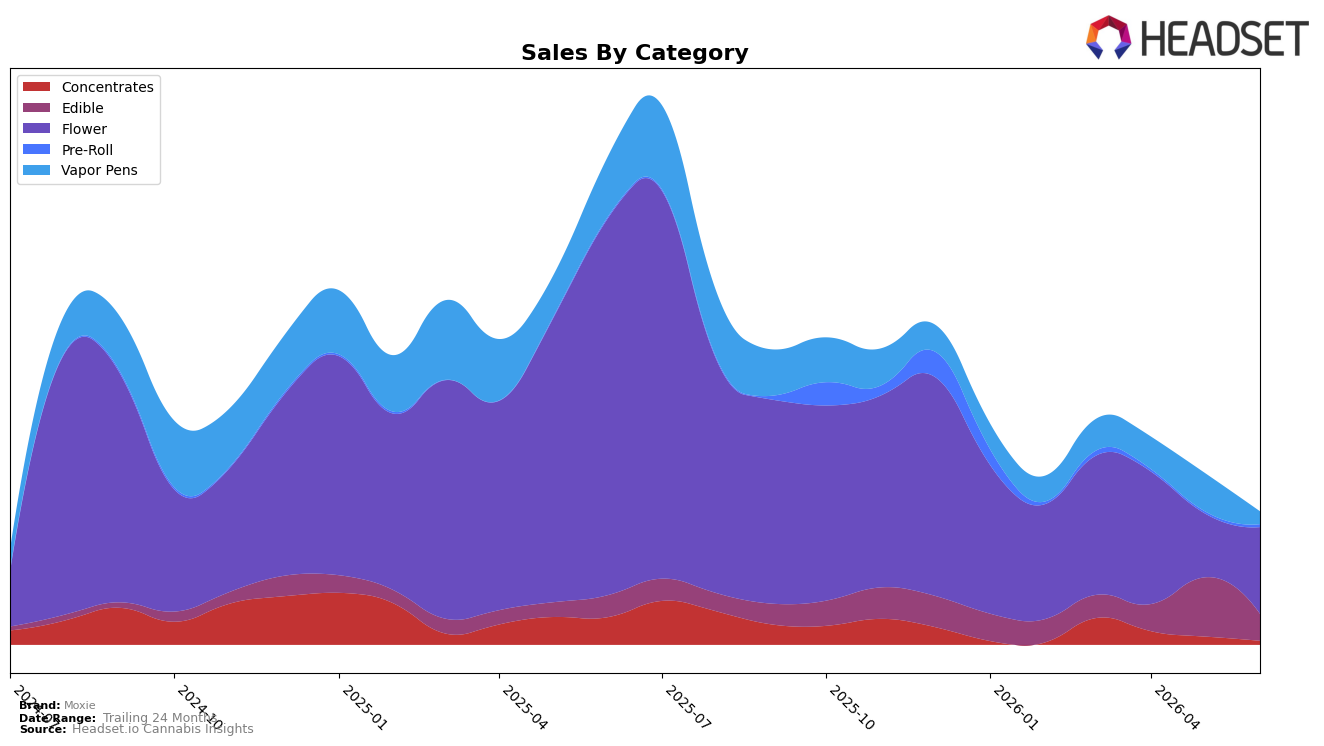

In June 2026, Moxie concentrated 65.58% of sales in Flower, where sales fell 77.08% year over year but rose 35.67% month over month, while Edible held 20.17% share with a 22.57% YoY increase and a 54.86% MoM decline. Vapor Pens slipped to 9.49% share with YoY down 79.24% and MoM down 67.12%, and Concentrates at 2.82% saw YoY down 86.47% and MoM down 53.29%; only Pre-Roll, at 1.95% share, grew on both horizons with 112.76% YoY and 45.98% MoM. With overall average price down 34.90% YoY and Flower’s average price at $43.28, the mix now leans on lower-priced Edible and Pre-Roll for volume, implying a defensive tilt toward accessible formats while legacy inhalables contract. The combined effect is a category barbell: Flower rebounds sequentially but remains sharply lower YoY, while Edible and Pre-Roll offset volatility, indicating Moxie is trading depth in inhalables for breadth across value-driven segments.

These shifts reposition Moxie toward mainstream, price-sensitive occasions: a 35.67% MoM lift in Flower alongside a 54.86% MoM pullback in Edible suggests near-term reliance on core Flower replenishment even as the brand tests lower-ticket formats. With Vapor Pens and Concentrates down 67.12% and 53.29% MoM respectively, and down 79.24% and 86.47% YoY, the brand’s historical potency-driven halo is unlikely to anchor share, pushing emphasis onto format accessibility and basket-entry roles signaled by Edible’s 22.57% YoY growth and Pre-Roll’s 112.76% YoY surge. Holding rank 41 in Flower in Ohio while Flower still represents 65.58% of mix indicates a crowded mid-pack stance; the pattern implies Moxie must treat Flower as a traffic driver and use Edible/Pre-Roll as margin stabilizers while selectively pruning underperforming inhalables.

Competitive Landscape

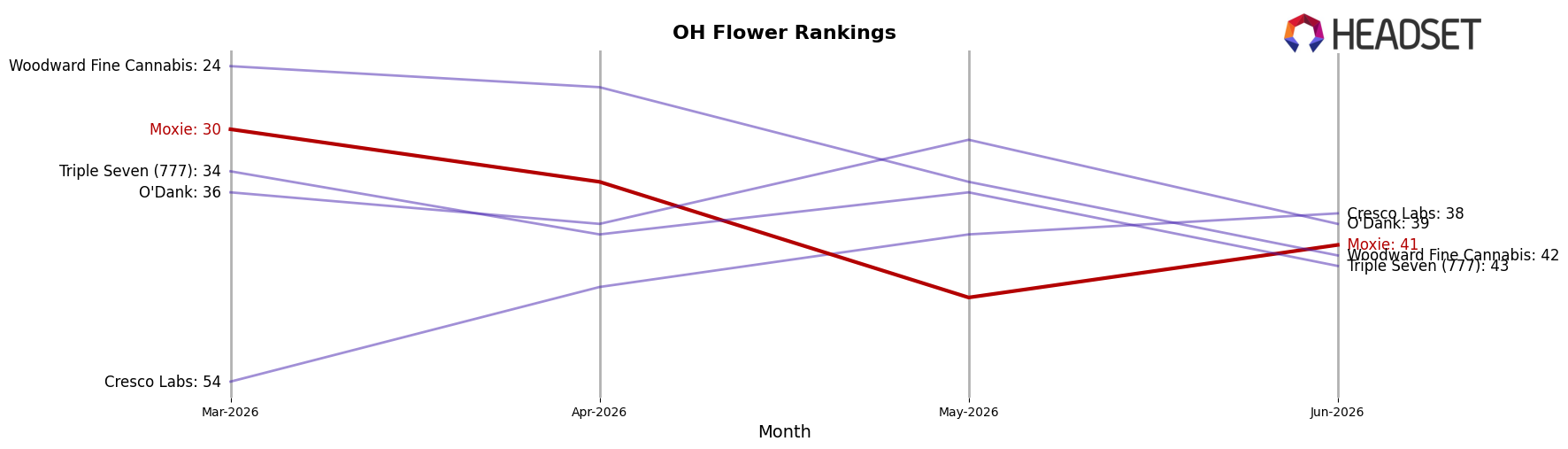

Moxie sits at rank #41 in OH Flower in June 2026, down 15 positions year over year and falling 11 places since March 2026 from #30, after previously peaking at #15 in July 2025; by contrast, Klutch Cannabis climbed 20 spots to #1 with 304.8% year-over-year sales growth while Riviera Creek edged up 1 position to #2 despite a 22.7% sales decline, signaling that relative rank is being driven more by competitive velocity than absolute growth levels and implying Moxie’s downward trajectory is a share-loss pattern rather than a temporary sales dip.

Notable Products

Blueberry Blackberry Gummies 10-Pack (100mg) led the reversals with a -64.4% month-over-month drop while still holding rank 1, and Cherry Lemon Gummies 10-Pack (100mg) fell -60.0% at rank 8, signaling sharp elasticity at the top and bottom of the edible list. Citrus Gummies 10-Pack (100mg) slid -40.3% at rank 3 and Strawberry Banana Gummies 10-Pack (100mg) declined -35.2% at rank 4, and with five of the top ten coming from the Gummies family the concentration amplifies downside when flavor shifts cluster in one month. GG4 (2.83g) rose to rank 2 with $40,536 alongside Wingsuit (14.15g) at rank 9, and Wingsuit Trim (14.15g) landed at rank 5, indicating Flower is absorbing demand as Edibles retrench. The pattern implies Moxie is pivoting toward Flower-led volume while Edibles require flavor and promo resets to stabilize share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.