Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Realeaf Botanicals concentrated 92.71% of sales in Vapor Pens, where year-over-year growth reached 98.13% despite a month-over-month decline of 6.38%, while the brand’s overall sales rose 82.42% YoY alongside a 24.97% YoY drop in average price. Edible held 2.53% share with 61.70% YoY growth but a steep 69.24% MoM contraction, and Pre-Roll at 1.76% share fell 56.90% YoY and 67.08% MoM; Flower, though only 1.52% share, slid 41.29% MoM with no YoY comp, and Concentrates and Topical contracted 33.34% and 50.49% YoY, respectively, with MoM declines of 33.34% and 37.48%. With a Vapor Pens rank of 15 in Illinois and the highest category-average price at $36.42 versus a brand-wide average of $31.91, the mix indicates volume-led Vapor Pen expansion is carrying growth while peripheral categories are being deprioritized, implying intentional focus rather than broad-based category scaling.

The combination of a 98.13% YoY surge in Vapor Pens and a 24.97% YoY reduction in average price suggests a value-tilt is unlocking unit velocity, helping secure a rank of 15 in Illinois while cushioning category volatility from 6.38% MoM declines. Concurrent 67.08% MoM and 69.24% MoM pullbacks in Pre-Roll and Edible, respectively, alongside a 41.29% MoM slide in Flower, indicate resource concentration and shelf rationalization toward Vapor Pens, which at 92.71% share effectively defines brand identity. The pattern implies Realeaf Botanicals is trading margin for share in Vapor Pens to solidify a defensible position in June 2026, accepting near-term volume cyclicality and narrower category breadth to reinforce a single-category leadership narrative.

Competitive Landscape

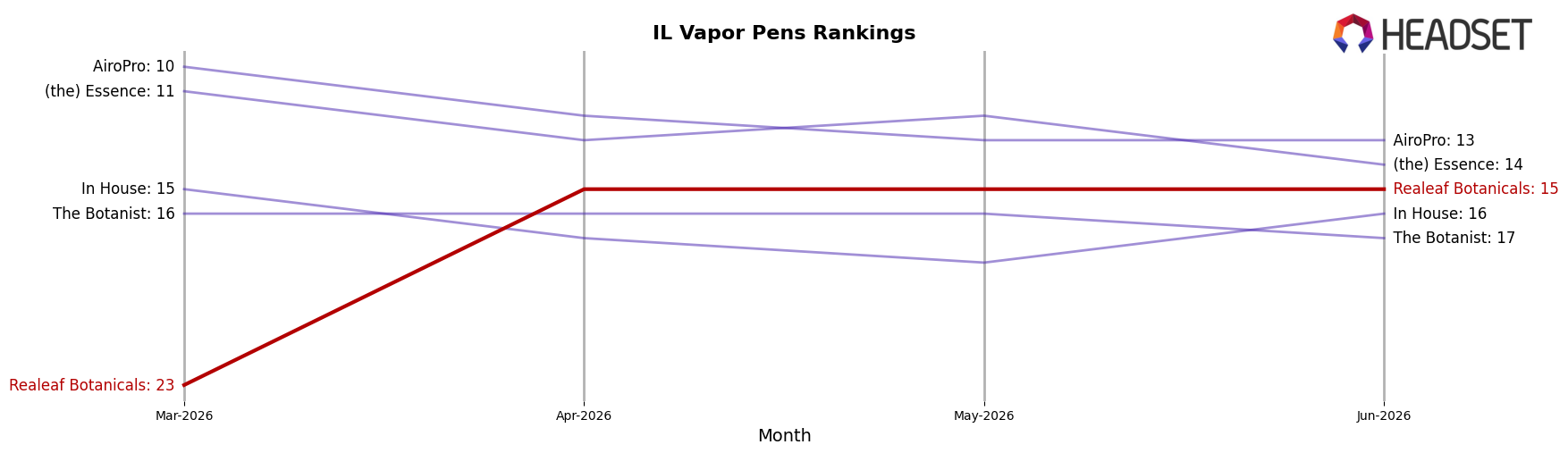

Realeaf Botanicals sits at rank #15 in IL Vapor Pens in June 2026, improving 10 positions year over year from #25 and rising 8 positions since March 2026 from #23, marking a peak rank of #15 in June 2026. In contrast, &Shine held steady at #1 year over year while posting a -12.7% sales change, and Select remained at #2 with a -6.8% sales change, indicating Realeaf Botanicals’ upward rank movement is occurring while top incumbents are flat in rank and negative in sales. This trajectory implies Realeaf Botanicals is gaining relative share position against higher-ranked brands despite category headwinds, with the jump from #25 to #15 suggesting momentum that could continue if incumbents’ negative sales trends persist.

Notable Products

Skyy - Blood Moon Distillate Cartridge (1g) posted the steepest decline in June 2026 at -59.9% MoM while falling to rank 9, and Skyy - Blueberry Dreams Distillate Cartridge (1g) also contracted -28.7% MoM at rank 7; by contrast, the category leader Skyy - Strawberry Fields Distillate Cartridge (1g) rose 39.6% MoM and held rank 1 with $46,919. With Vapor Pens occupying seven of the top ten SKUs, Skyy - Purple Urkle Distillate Cartridge (1g) slid -21.5% MoM to rank 3 as the Strawberry Fields line extended share at the top. The mix implies a portfolio leaning harder into a single flagship while legacy pen variants lose velocity, signaling near-term concentration risk and a need to refresh depth in the Vapor Pens lineup.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.