Ohio Just Cleared $1.1B. Here's What Should Be on Your Shelf by Summer.

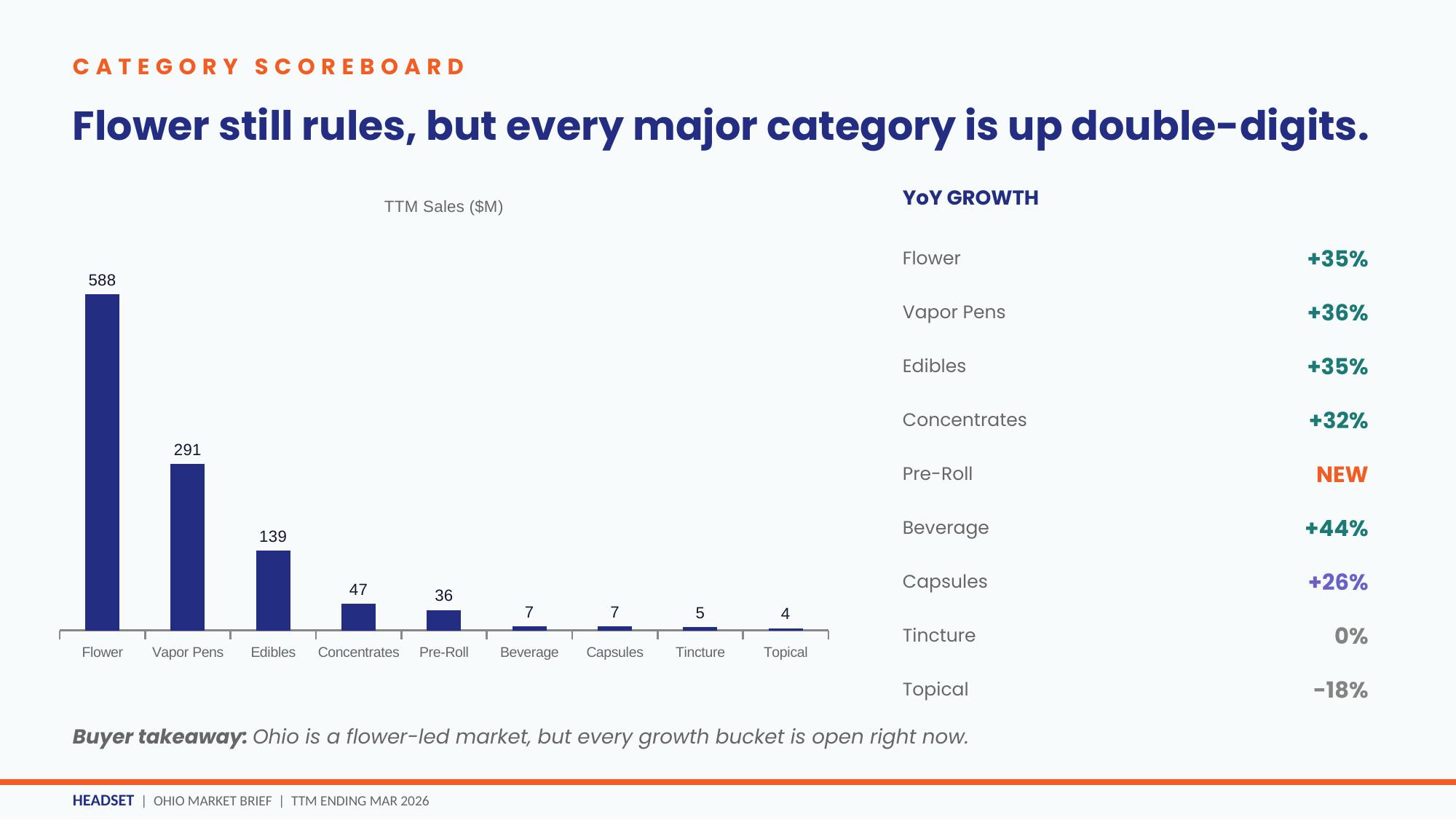

If you're buying for an Ohio retailer right now, the inventory plan you built on 2024 numbers is already behind. The state cleared $1.12 billion in retail sales over the trailing twelve months ending March 2026, up 35% year over year, with every major category posting double-digit growth. Ohio is no longer an emerging market. It's a top-tier US market with mature volume and a still-expanding shopper base.

This brief covers what's moving, what's margin-safe, and what your shelf should look like by summer. The data is from Headset's Ohio retail panel, trailing twelve months ending March 2026.

The category scoreboard

Flower still rules at $588M in TTM sales, up 35%. Vapor pens are second at $291M, up 36%. Edibles cleared $139M at 35% growth. Concentrates added $47M at 32% growth. Beverages, while small at $7M, grew the fastest of any established category at 44%.

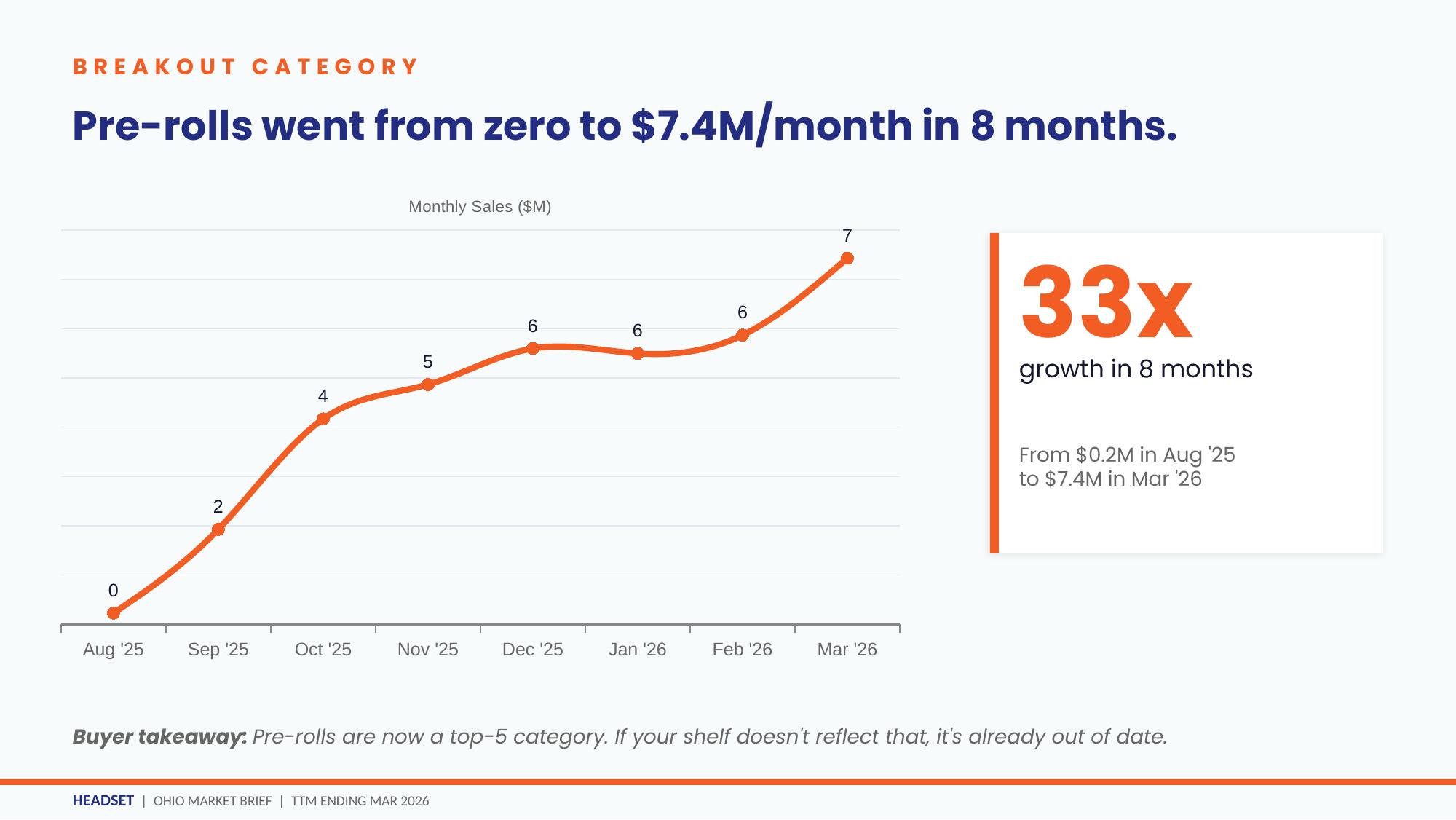

The headline number, though, is pre-roll. The category went from effectively zero to $7.4M per month in eight months. That's 33x growth from $0.2M in August 2025, putting pre-rolls in the top five categories before most retailers have adjusted their planograms.

Pre-roll is the story

Three things to know about how the pre-roll shelf is shaking out:

- The leaderboard is fragmented. The top three brands by 2026 YTD sales (Dogwalkers at $2.66M, Buckeye Relief at $2.65M, and (the) Essence at $2.61M) are within a hair of each other. No clear winner has emerged.

- Three distinct price tiers are in play. Premium ($30+) is RYTHM and Woodward Fine. Mid ($16 to $24) is Dogwalkers, Essence, Buckeye, and King City. Value (under $12) is Pure OH Wellness, Certified, Klutch, and The Solid. Value brands move volume. Premium brands carry margin. The buyers winning right now are building across all three tiers, not picking one.

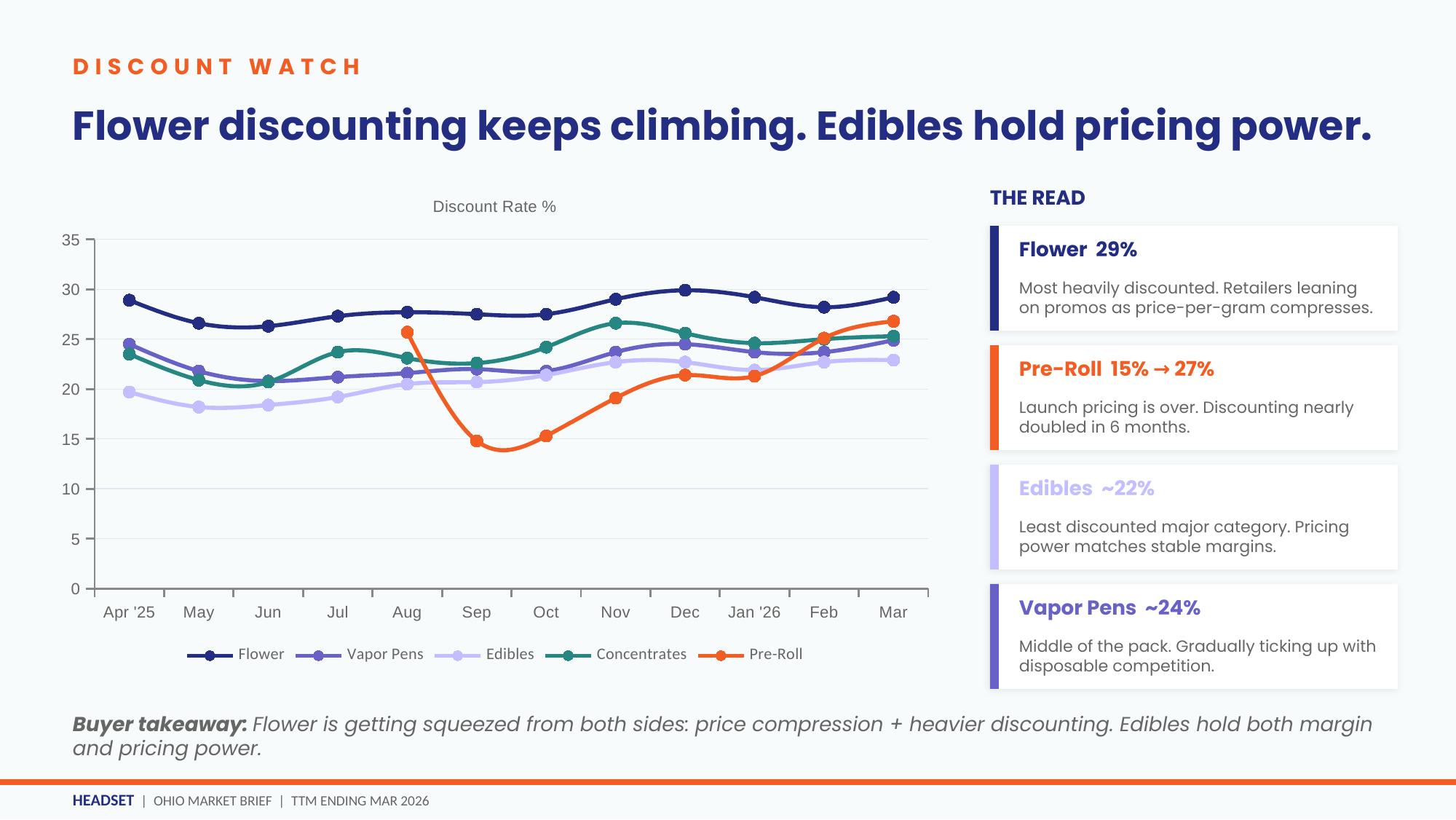

- Margin is normalizing. Pre-roll gross margin has come down from 49% to 44% as launch premiums fade and competition enters. Discounting on pre-rolls nearly doubled in six months, from 15% to 27%. Plan around the new reality, not the launch-era one.

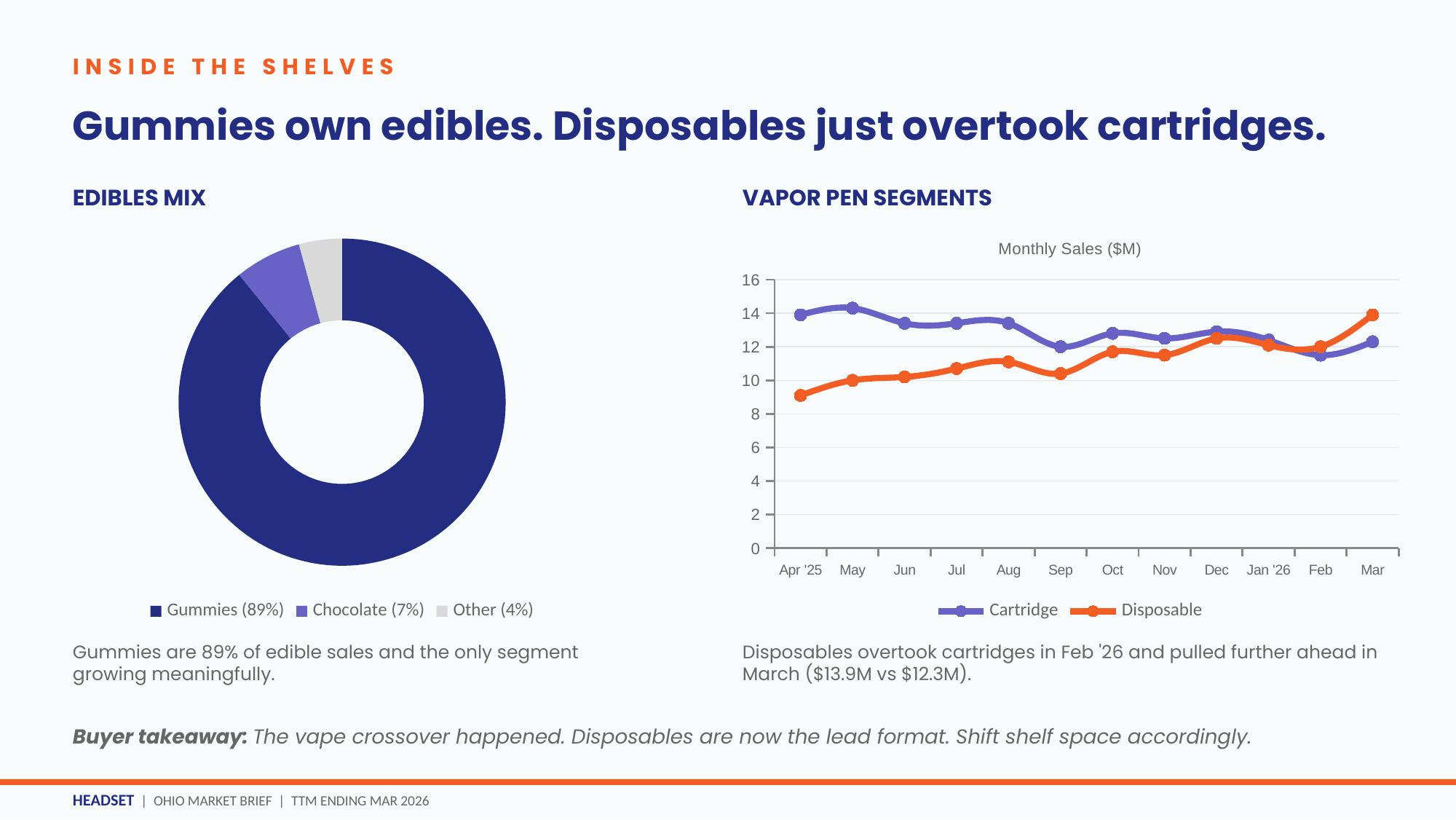

The vape crossover happened

For the first time, disposables overtook cartridges in Ohio. February 2026 was the crossover month. By March, disposables hit $13.9M vs $12.3M for cartridges, and the gap is widening. Vape pen gross margin has also recovered hard, from 39% to 45%, with disposables doing the work.

If your vape shelf is still cartridge-weighted, it's a backward-looking shelf. Shift the facings.

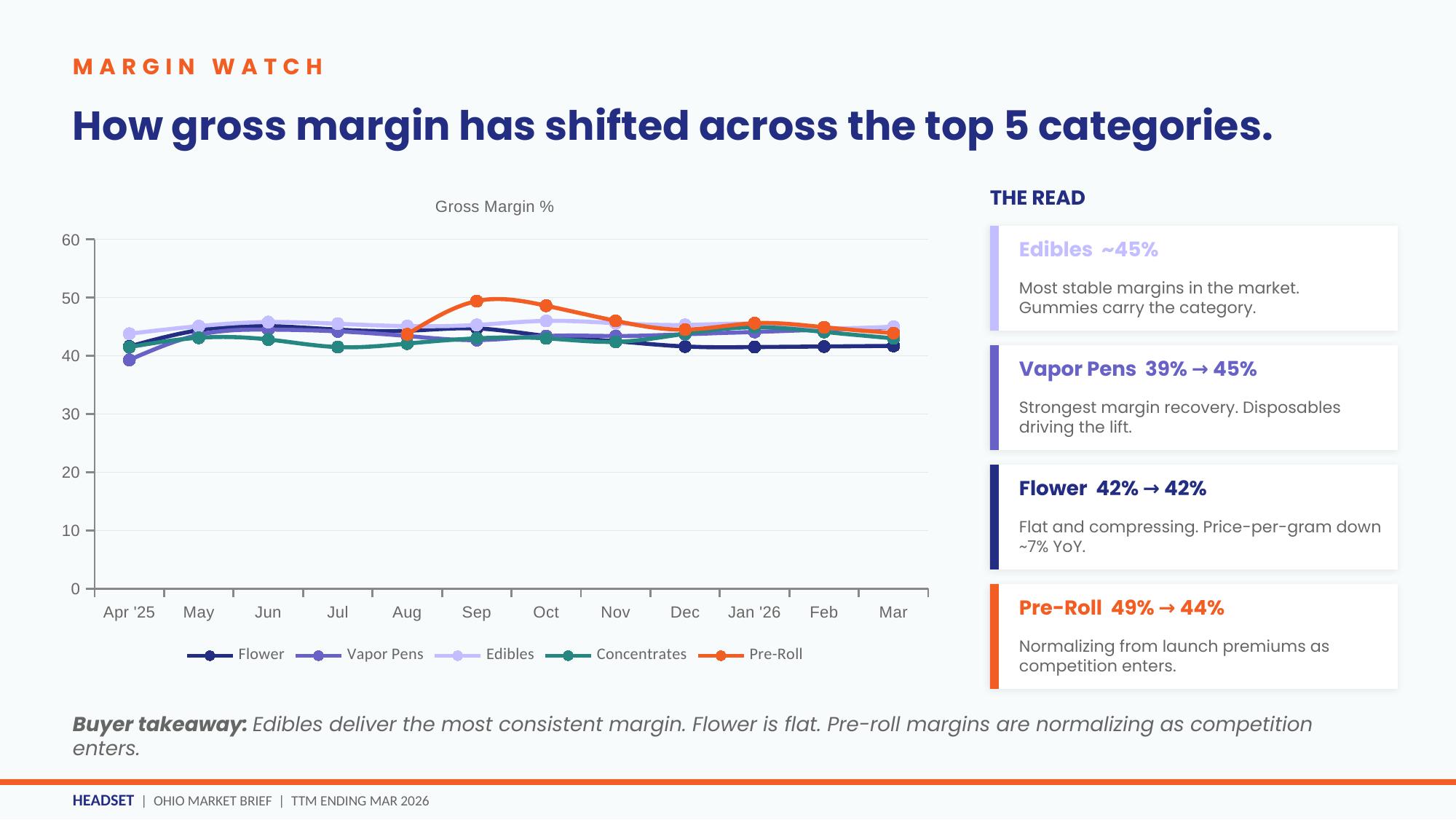

Where the margin is

Edibles deliver the most stable margin in the market at roughly 45%, and they hold pricing power: edibles are the least-discounted major category at 22%. Gummies do almost all the work, accounting for 89% of edible sales. Chocolate is 7%. Everything else combined is 4%.

Flower margin, by contrast, is flat at 42% and getting squeezed. Price-per-gram is down ~7% year over year, and discounting is at 29%, the highest of any major category. Don't discount edibles like you discount flower. The data says you don't have to.

Who's buying

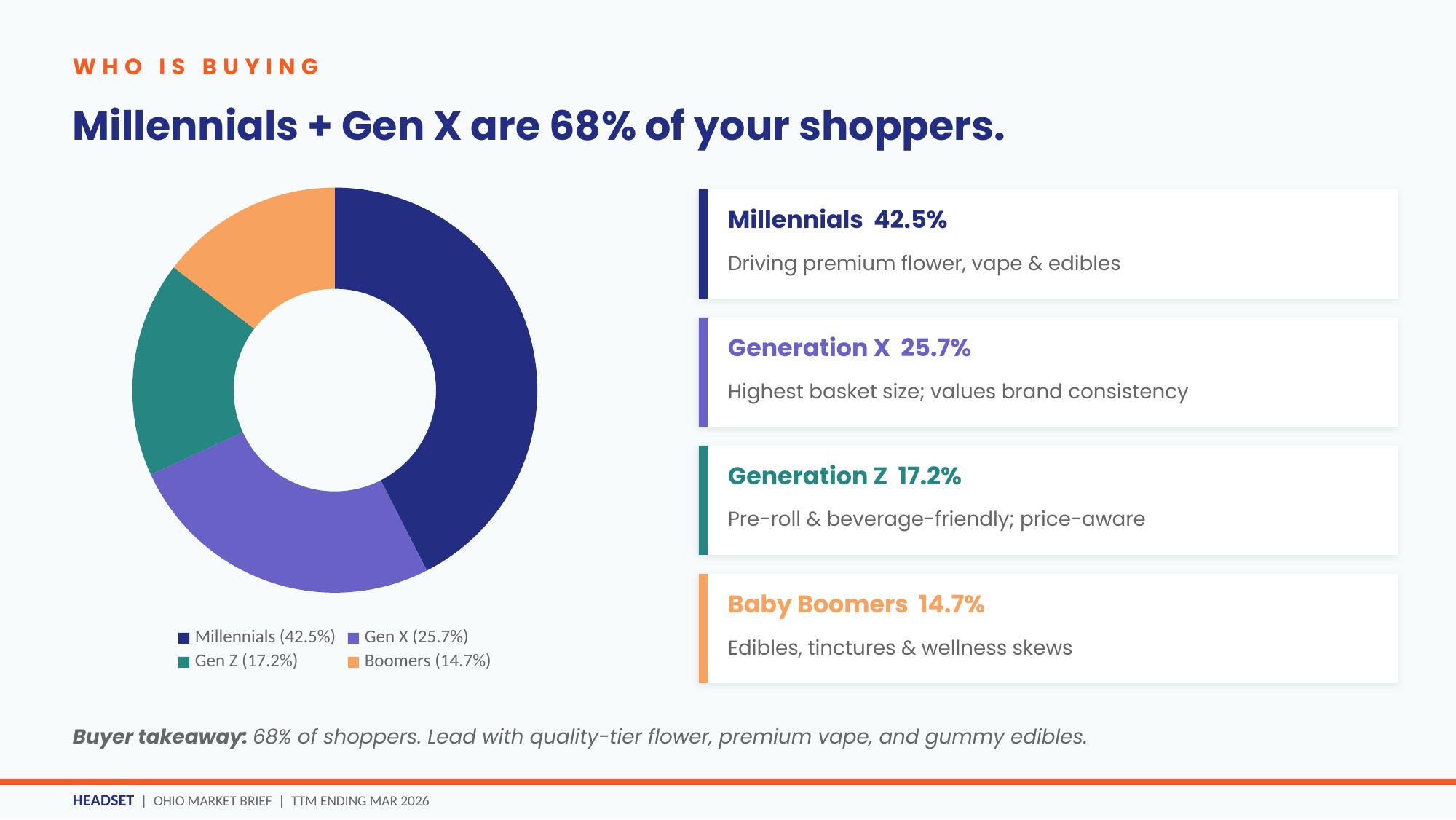

Millennials and Gen X are 68% of Ohio shoppers: 42.5% Millennials, 25.7% Gen X. Gen X carries the highest basket size and values brand consistency. Millennials drive premium flower, vape, and edibles. Gen Z (17.2%) skews toward pre-roll and beverage and is the most price-aware. Boomers (14.7%) lean wellness: edibles, tinctures, topicals.

Average basket size in Q1 2026 was $67.97 across two items, with a 26% average discount rate. Edibles are the universal attachment: tincture, beverage, and topical buyers attach edibles 40%+ of the time. Flower (96% solo), vape (94%), and pre-roll (91%) are trip drivers. Tinctures, topicals, and beverages are always add-ons, never the reason for the trip. Merchandise the wellness categories near edibles to lift baskets.

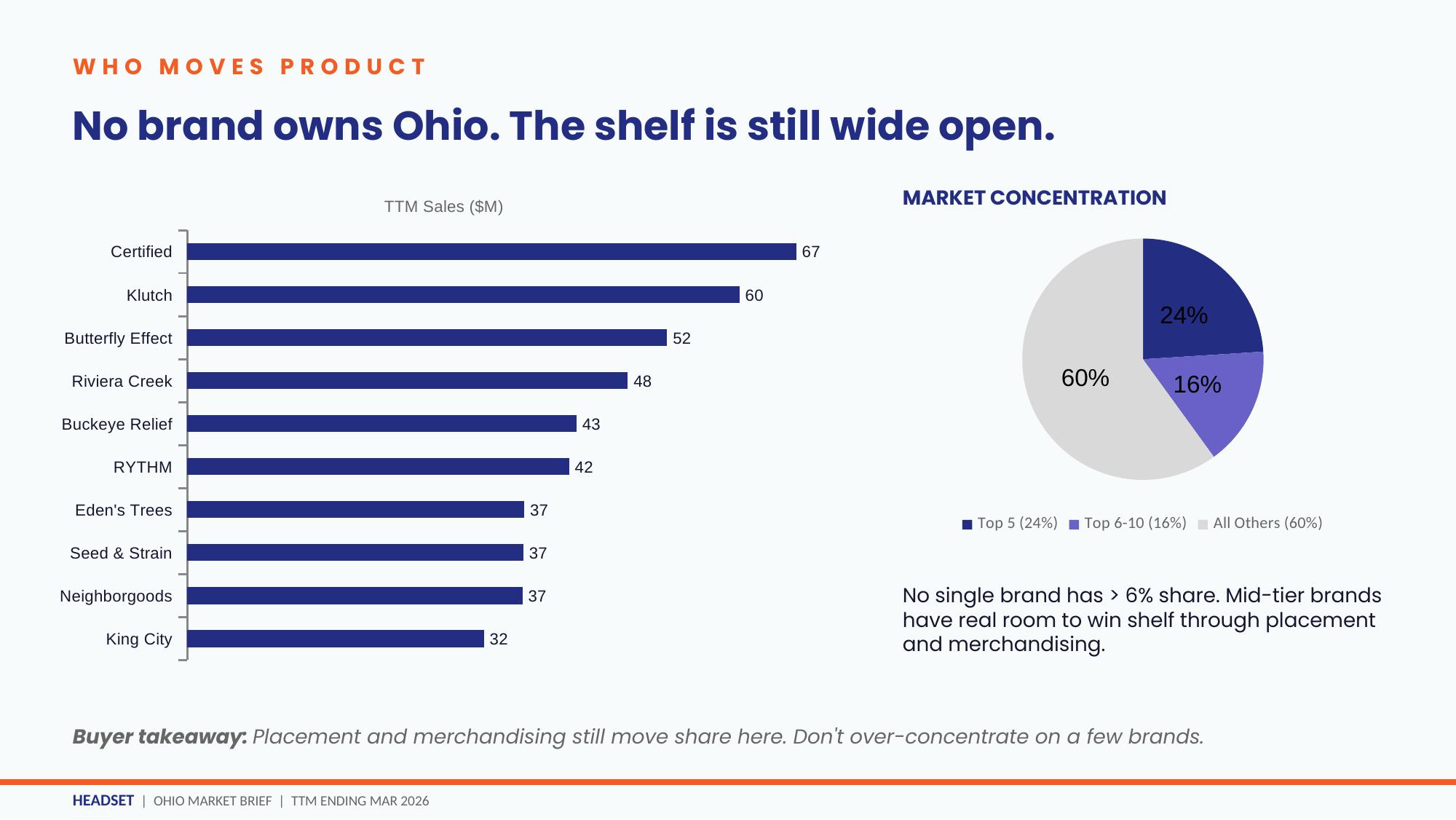

The shelf is still wide open

No single brand owns more than 6% of Ohio share. The top five combined are 24%. The next five are 16%. Everyone else is 60%. Placement and merchandising still move share in this market in a way they don't in mature ones. If you're a buyer, that's leverage. Don't over-concentrate on the top five.

Five moves to make on Monday

- Stock pre-roll, deeper than feels comfortable. From zero to a top-five category in eight months. Breadth and depth are still light at most retailers.

- Shift your vape shelf toward disposables. The crossover is here, not coming. Disposables passed cartridges in February.

- Protect edible margin. ~45% gross margin, consistent all year. Don't promo what doesn't need it.

- Diversify your brand mix. Top five is only 24% share. Mid-tier and emerging brands move on placement, not pull.

- Train budtenders to cross-sell edibles with wellness categories. A prompted suggestion at the register is where the basket lift happens.

The bottom line

Ohio's window for shelf advantage is still open, but it's narrower than it was six months ago. Flower anchors the trip. Vape is reformatting. Pre-roll is the breakout. Edibles are the margin engine. The buyers who are winning right now are reading the data weekly and adjusting in cycles measured in weeks, not quarters.

Source: Headset retail panel. Trailing twelve months ending March 2026.